25.01.2022

15 minutes of reading

Biofuels in the road transport sector

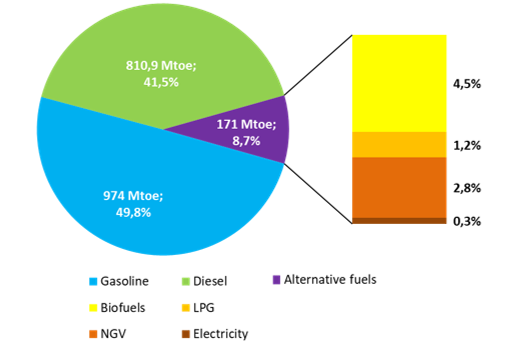

In 2020, global energy consumption in the road transport sector amounted to just over 1.95 Gtoe. For the first time since the 1970s, as a result of the global health crisis, the sector recorded a fall, which amounted to more than 11% compared to 2019. Nevertheless, in 2020, the share of alternative fuels to oil-based gasoline and diesel increased, to represent 8.7% of fuels consumed, i.e., 171 Mtoe. Among these alternatives (biofuels, LPG1, NGV2, electricity), biofuels represented 87.7 Mtoe, i.e., an alternative fuel market share of 52% (Fig.1). Their consumption increased by 11% between 2018 and 2019, and then fell by 7% between 2019 and 2020.

Source: IFPEN, from Enerdata and FO Licht

Since 2011, throughout the world, the volume of biofuels consumed in the transport sector had been increasing constantly until 2019. While the growth rates of ethanol and FAME (Fatty Acid Methyl Ester) biodiesel slowed in the 2015-2016 period, consumption subsequently began to rise again with the emergence of the HVO (Hydrotreated Vegetable Oil) market in 2017, and then for all products in 2018 and 2019. The fall in consumption observed in 2020 affected all products (Fig. 2).

Source: IFPEN, from FO Licht’s

On a continental level, the biofuel incorporation rate in road fuels varies depending on the region, but Latin America continues to boast the highest rate at 12% (energy) thanks to its ethanol market: ethanol alone has an incorporation rate in gasoline of more than 15%. North America and Europe follow, with respective rates of 6.5% and 5.6% (energy) respectively. In Asia, the rate only amounts to 2.2%, but it is nevertheless the zone where market growth is the highest.

In Europe, between 2011 and 2016, total biofuel consumption in the road transport sector oscillated between 13 and 15 Mtoe, marking the slowdown in market growth across the community, due in particular to a number of uncertainties concerning regulatory changes. The European Union then once again observed annual growth of more than 10% in 2017 and 2018, followed by 3.6% in 2019, to reach a total consumption of close to 18 Mtoe. This return to growth was primarily linked to the increase in the consumption of biodiesel, for which some sectors were supported by attractive regulations based on a double counting system for achieving objectives set out in the European Renewable Energies Directive (RED).

In 2020, the effects of the health crisis on total biofuel consumption varied widely from one continent to another. Throughout continental Europe, the crisis triggered a fall of less than 5% and in the European Union itself overall consumption remained more or less stable. In North and South America, the decrease amounted to 10%, while the Asia-Pacific region maintained positive growth of +1.7%, albeit well below the growth rate observed in previous years (+43% between 2018 and 2019).

In 2019, the renewable energy penetration rate for the European transport sector was 8.9% (energy)3, a rate that had been growing constantly with a view to achieving the regulatory objective of 10% specified for 20204. With the drop in demand for energy in the road and rail transport sectors observed in 2020, in the majority of Member States already close to the target rate, reaching the objective was facilitated (particularly for Austria, the Netherlands and Germany). Sweden and Finland had already exceeded the 10% objective several years previously.

Gasoline substitutes

Since the emergence of the biofuel market, ethanol has remained the primary substitute to gasoline fuels used around the world. The United States continues to be the biggest producer, followed by Brazil. The two countries alone account for 84% of the global market. With far lower volumes, Canada, China, India and Thailand complete the world’s top six producers. France is 8th in the global rankings and 1st in Europe.

.PNG)

Source: IFPEN, from FO Licht’s

In 2020 a decrease in production was observed in all producer countries but the fall was particularly marked in the USA, which was responsible for 65% of the drop. Brazil was responsible for close to 22% of the decrease observed.

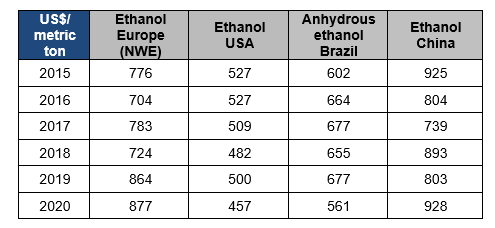

Despite a highly competitive market price associated with high stock levels (Table 1), American bioethanol fuel exports were badly affected by the health crisis (particularly those destined for Brazil). Nevertheless, exports to Canada held up well, exports to China resumed and exports of medical ethanol (for hand gel in particular) compensated for ethanol fuel losses. In 2020, 40% of the ethanol exported from the USA was destined for the medical market. The ethanol incorporation rate remained stable at around 10% of gasoline demand in 2020, i.e., an ethanol consumption of 47 billion liters, a fall of more than 13% compared to 2019.

Source: IFPEN, from Argus

In Brazil, the fall in demand and the price of ethanol encouraged producers to maximize sugar production and minimize ethanol production in flexible sugarcane distilleries, thereby enabling them to increase profitability. As for the use of corn for ethanol production, it increased by 80%, thereby minimizing the decline in the local market. In addition, the fall in the price of crude oil in 2020 ($42 per barrel on average throughout the year compared to $69 in 2019) made E1005 ethanol fuel less competitive in Brazil, reducing its distribution at the pump by 17% in the first half of 2020. In several Asian countries, this fall in competitiveness also delayed planned increases - heavily subsidized - in incorporation rates (E20 in Thailand and E10 in China, in particular). China also faced a significant reduction in local cereal supplies, driving up the price of corn and reducing the profitability of corn-based ethanol. Nevertheless, despite being delayed at State level, the roll-out of E10 has continued throughout the various provinces of China, with, at the end of 2020, eight provinces boasting full coverage and six others where availability was increasing. The number of Chinese ethanol production units is currently expanding. Resources are diversifying towards manioc and rice, and a project to build a synthetic ethanol production unit based on the gasification of lignocellulosic biomass was launched in the fall of 2020.

In the European Union, the reduction in ethanol production was below 10%. While Germany remains 1st in the rankings of European ethanol fuel consumers, France retains its position as the leading producer, despite a 20% fall between 2019 and 2020. France was the country where the impacts were greatest (along with Belgium), due to the sharp fall in demand, both locally and in countries to which we export, as well as a poor beetroot harvest and a significant rise in cereal prices at the end of the period. In other Member States, the introduction of E10 (in the Netherlands, Spain and Hungary), its continued territorial expansion (in Romania), as well the expansion of E85 (in France) supported the national use of bioethanol. With falling oil prices and stable European ethanol prices, the Swedish market for fuels with a high ethanol content - unsubsidized - nevertheless fell by 50%. In 2020 around fifteen European bioethanol fuel production units dedicated a percentage of their capacity to the production of medical ethanol. Examples include Germany, the Netherlands, Spain and Austria, who were able to compensate for some of the decrease in the use of their production capacity. Hungary even managed to increase its local capacities.

Diesel substitutes

Two main biofuels are currently incorporated into the road diesel fuel pool: FAME6 and HVO7. They use biomass resources containing fatty acids, such as oil crops (rapeseed, palm, soybean, etc.) or used cooking oils or animal fats. Unlike FAME, the incorporation of which is limited to a maximum of 10% vol. in diesel distributed at the pump in the European Union, there is no limit to the amount of HVO that can be incorporated in the conventional diesel mix. The youngest industry but one that is enjoying strong growth, HVO represents 8% of biodiesels consumed globally (Fig. 2).

While global biodiesel consumption fell slightly in 2020, the market was less affected by the health crisis than ethanol. This was because the reduction in demand for diesel was smaller than that for gasoline, the impact of health measures (lockdown, teleworking, etc.) on freight transport being far less significant than it was on the use of private vehicles. In addition, in the European Union, the leading producer and long-standing consumer of biodiesel, regulatory objectives governing the incorporation of biofuels and the reduction of fuel emissions encouraged the use of biodiesels, particularly those produced using recycled oils, due to superior environmental performances. HVO biodiesel also enabled Member States that had already reached the 7% incorporation limit (energy and volume) to increase their level of fossil diesel substitution with HVOs produced from recycled FOGs (fat, oil and greases), in particular.

The growth in the HVO market thus made it possible to largely compensate for the fall in FAME consumption resulting directly from the decline in the demand for diesel.

%20production%20movements%20by%20zone%20(in%20billions%20of%20liters).PNG)

Source: IFPEN, from FO Licht’s

In the EU, FAME production fell by 7% while that of HVO increased by almost 20%, particularly in France and Italy, where new plants that had come on stream in 2019 operated all year for the first time. Today, the leading European HVO producers are the Netherlands, France, Italy, Spain and Finland, with almost 95% of the local market. Production capacity is expected to rise in 2021, driven in particular by an expansion in capacity in Sweden.

In the USA, biodiesel consumption continued to rise, with 8.5 Mtoe in 2020 and a market made up of 65% FAME and 35% HVO. The market has remained dynamic in the country as a result of the federal government’s incorporation mandates (RFS28) and carbon intensity reduction requirements in California (LCFS9). In addition, a four-fold increase in HVO production capacities is expected in the short term, particularly via the conversion of fossil fuel refinery units. California and several Canadian States (Oregon and British Columbia) are particularly encouraging the development of the recycled oil-based biodiesel market.

The biodiesel market also continued to grow in Brazil, with a consumption of 5 Mtoe in 2020, thanks primarily to a bumper soybean harvest and an increase in the incorporation requirement to 12% vol. While soybean oil represents 75% of the biodiesel produced in Brazil, the share of FOGs (primarily animal fats) is now almost 8%.

In Indonesia, Asia’s leading producer, the increase in national incorporation requirements from 20% to 30% vol. at the start of 2020 made it possible to compensate for the 12.5% fall in the demand for diesel caused by the health crisis. In 2020, FAME consumption thus exceeded 7 Mtoe. Moreover, the launch of local HVO production may make it easier to reach the 40% incorporation mandate announced for the coming months.

Source: IFPEN, from Argus

Source: IFPEN, from Argus

* Class I : HVO from food crops, enabling a reduction in greenhouse gases of 65% min.

**Class II : HVO from recycled vegetable oils (UCO, POME), enabling a reduction in greenhouse gases of 85% min.

***Class III : HVO from category 3 animal fats, enabling a reduction in greenhouse gases of 80% min.

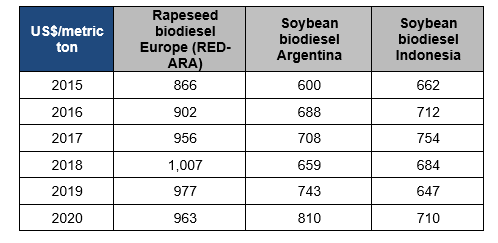

In 2020, as had been the case for several years, FOGs were, behind rapeseed oil, the 2nd most widely used raw material in the EU for biodiesel production, with a share of close to 23% for used cooking oils (UCO) and 6% for animal fats. The increase in their usage is due to the benefit of double counting for meeting the 2020 regulatory objectives stipulated in the RED Directive. Nevertheless, the collection of UCOs was greatly hampered by the closure of restaurants. Imports rose by 20% compared to 2019, primarily from Malaysia, China, the USA, Russia and Indonesia. In 2020, crude palm oil still accounted for 18% of European biodiesel oil supplies, a level that increases to almost 30% for all crude oils and palm oil derivatives (including UCO, PFAD10 in particular). In the short term, their use is set to be affected by the gradual elimination of biofuels derived from high ILUC11-risk crops. European delegated act 2019/807 limits the use of these resources to the 2019 level until 2023 and thereafter gradually eliminates them by 2030. In its current version, only palm oils are concerned. A revised version of this act, due in 2021, may include other types of oils, such as soybean oil.

In addition to being able to meet the demand for road diesel substitutes, the HVO process may also make it possible to meet a demand for kerosene substitutes in the aviation sector via the coproduction of a fuel known as HEFA-SPK, already approved by the ASTM12 for maximum incorporation of 50% vol. with fossil kerosene. While this option appears to be of interest to a number of industrial players, its development, in Europe and North America, is set to be hampered by availability limits affecting oils and fats meeting sustainability requirements set by the regulatory authorities in both zones.

Within the framework of the publication in July 2021 of its collection of “Fit for 55” policy measures aimed at achieving carbon neutrality in 2050 and cutting greenhouse gas emissions by 55% by 2030, the European Commission revises the renewable energy consumption objectives for the transport sector set out in its REDII13 Directive. The maximum levels of biofuels derived from biomass resources of food origin (max. 7% LHV of the 2030 target) and waste oils (UCO-type) and animal fats (max 1.7% of the 2030 target) are maintained. Other renewable fuels are then supported by minimum incorporation levels such as advanced biofuels (min. 2.2% LHV) and e-fuels (min. 2.6% LHV). Among these options, several technologies, such as Fischer-Tropsch synthetic fuels, which mobilize potentially more abundant lignocellulosic biomass resources, will have to take up the strain in order to meet community objectives and the growing demand for renewable fuels for the road diesel pools and kerosene for the aviation sector.

Spotlight on biofuels in the aviation sector

With the growing awareness of the existing environmental impacts of international air travel (which accounts for 13% of CO2 emissions in the transport sector) and given the sector’s growth outlook (pre COVID-19), Member States of the International Civil Aviation Organization (ICAO) adopted a greenhouse gas stabilization objective from 2021. In order to achieve this objective, the use of alternative and sustainable fuels (SAF14) is seen as the principal lever for reducing emissions along with CORSIA15.

There are currently nine ASTM-approved (bio)kerosenes, including some that are produced using processes that are already mature or close to industrial maturity, such as HEFA-SPK16, coproduct of HVO biodiesel units, FT-SPK17, coproduct of the BtL and e-fuel processes for the production of Fischer-Tropsch synthetic biodiesel, and ATJ-SPK18, derived from the conversion of ethanol or isobutanol into synthetic kerosene. These (bio)kerosenes are currently approved for incorporation in traditional kerosene, with a maximum limit of 50% vol. in the blend.

Among the European Commission’s “Fit for 55” package of proposals, those concerning the ReFuelEU Aviation initiative are aimed at introducing SAF incorporation obligations for kerosene suppliers to European airports (Table 4). From 2030, these incorporation levels would be made compulsory at all airports throughout the EU (with exemptions for small airports). These requirements would only apply to biofuels produced from UCO and animal fats (Annex IX.B of the REDII Directive), advanced biofuels (Annex IX.A of the REDII Directive) as well as e-fuels.

%20in%20the%20aviation%20fuel%20mix.PNG)

Source: ReFuelEU Aviation initiative

The various proposals contained in the “Fit for 55” package will now be debated over a period of several months at the European Parliament and the Council of Ministers representing Member States.

In France, a roadmap has already been adopted (at the start of 2020) setting out the country's ambition and national strategy for the development of sustainable aviation biofuels with incorporation rates identical to those of the EU for 2025 and 2030. In order to make this roadmap operational, the French ministries for the ecological and inclusive transition, the economy and agriculture immediately launched a call for expressions of interest concerning the production of sustainable aviation biofuels aimed at identifying projects and French players with the potential to become established in this field. More recently, last July, ADEME launched a call for projects with an envelope of €200 million to support R&D projects, with a view to accelerating the bringing to market of innovative and sustainable solutions, from the industrial research phases through to engineering prior to the investment decision.

In the USA, the Biden administration plans to cut national aviation emissions by 20% by 2030 and is proposing an SAF tax credit, the ultimate aim being to replace all aviation fuels by sustainable alternatives by 2050.

In mid-November 2021, according to the ICAO19, there were 21 government measures around the world, either adopted or being developed, supporting the roll-out of SAFs. In addition, during the course of the year, there was a significant increase in the number of SAF supply contracts, concerning the distribution of a total of around fifteen million metric tons of SAF. To date, 43 airports are estimated to be in a position to distribute SAF on a continuous basis, and 22 on a batch basis.

Concrete and restrictive measures will nevertheless have to be widely introduced in order to ensure the long-terms distribution of SAFs within a fair market context.

Biomethane for NGV powertrains

An as yet minority renewable fuel, its consumption is nevertheless increasing in some zones where natural gas has historically figured among road fuels. Currently primarily produced by the anaerobic digestion of organic waste (methanization), or via the recovery of landfill gas, biogas is a renewable fuel principally used for heat and electricity production. Only a fraction (less than 10%) is purified to obtain biomethane suitable for injection into the natural gas network or used as a fuel in dedicated vehicle engines.

In the USA, NGV fleets made up of heavy trucks, buses and waste collection vehicles, have grown significantly in recent years. In 2020, NGV consumption was nearly 3 Mtoe and around 55% of this gas was renewable, i.e., 1.7 Mtoe. So biomethane fuel enjoyed growth of close to 25% compared to 2019. In the USA, most of this renewable gas comes from the recovery of landfill gas but biogas derived from the anaerobic digestion of agricultural waste grew in importance in 2020, increasing from 3% to 11% of the biogas produced nationally.

Biomethane fuel consumption in the European Union amounted to 0.32 Mtoe in 2020, i.e., 2% of total biofuel consumption and an increase of 30% compared to 2019. Primarily obtained via the fermentation of organic waste, biomethane fuel is considered in European regulations as an advanced biofuel, thereby contributing to the 0.5% and 2.2% objectives set for 2025 and 2030 respectively in the latest REDII revision. While Sweden is the leading European producer of bioNGV, the highest growth was seen in Italy (+41.2 ktoe), Germany (+19.2 ktoe) and the Netherlands (+15.7 ktoe).

Focus on France

In 2020, France incorporated a total of 4 million m3 (or 2.9 Mtoe) of biofuels in fossil fuels, i.e., a fall of 15% compared to 2019, directly related to the health crisis. Nevertheless, the global incorporation rate was 9.7% vol. not taking into account double counting.

Since 2017, SP95-E1020 containing up to 10% by volume of ethanol has been the most consumed fuel by French gasoline vehicle owners, with a market share of around 50% in 2020. Super ethanol E85 (gasoline containing up to 85% ethanol by volume), dedicated to Flex-fuel vehicles and gasoline vehicles fitted with conversion boxes, continued its growth, with a market share of 3.6% (+ 4% compared to 2019), despite a 14% decrease in overall gasoline consumption due to the health crisis. The number of service-stations distributing E85 continued to increase (+585 stations) and while the adapted vehicle fleet (standard flex-fuel or vehicles fitted with conversion boxes) appears to be stable, flex-fuel vehicle ranges have developed, the main manufacturers being Ford and Jaguar Land Rover. Also in France, E85 is subject to a lower TICPE21 meaning it is more attractively priced (0.65 €/l on average in 2020), and the price of the fuel has been significantly less affected by the energy price increases observed this year (+20% over the first 10 months of 2021 for E95-E10, compared to + 4% for E85). A clear advantage that suggests a continued increase in market share for this fuel in 2021.

%20et%20en%20%25%20volumique%20pour%20le%20SP95-E10%20(en%20jaune).PNG)

Sources: SNPAA 2020 from CPDP (French Professional Oil Committee)

Among fossil gasoline substitutes, ethanol makes up by far the greatest share (71% of the mix) and saw a growth in consumption in 2020. ETBE (25% of the mix) and HVHTE22 (a synthetic gasoline fuel making up 4% of the mix) experienced falls in consumption of 29% and 48% respectively. While until recently HVHTEs were imported and produced from palm oil, in 2020, for the first time, most of them (60%) were produced locally from animal fats and rapeseed. This is the result of the French parliament’s decision, in 2018, to exclude products derived from palm oil from the list of biofuels, with the law coming into force on 1 January 2020. The measure had a significant impact on the mix of resources mobilized by the French HVO and FAME sectors.

In terms of fossil diesel substitution options, FAME and in particular VOME23 continue to make up the majority (> 80% of the mix), followed by HVHTG24 (12%). Rapeseed and soybean are the principal resources mobilized for VOME. The disappearance of palm oil thus globally corresponds to the decline in the VOME market observed in 2020. The exclusion of palm oil had a significant impact on the HVHTG sector, with a fall in consumption of 36% in 2020 and a resource mix primarily made up of UCOs, animal fats and rapeseed.

Taking all of the various categories into account, it should be noted that the consumption of biofuels, which benefit from double counting for the purposes of achieving the objectives set out in the European REDII Directive, increased by 13% in 2020. The majority of this consumption concerned FAME and HVO derived from UCOs (70%), followed by ethanol from wine residues (24%). The latter is currently the primary contributor to the advanced biofuel objectives set for 2023 in France’s current long-term energy plan (PPE). In order to reach these objectives, other sectors, particularly those using lignocellulosic resources, will undoubtedly emerge in the French and European biofuel mix.

Expected opportunities for advanced biofuels

In the European regulations, advanced biofuels correspond to biofuels derived from resources listed in annex IX-A of the REDII Directive25, primarily made up of biomass from organic waste, agricultural and forestry residues, organic residues from the agrifood sector and other non-food biomass of the lignocellulosic or algae type. UCOs and animal fats, which are included in annex IX-B and benefit from a maximum incorporation threshold, are excluded. In its current version, the REDII Directive imposes the deployment in each Member State of a minimum incorporation rate of 0.2%, in 2022, 1% in 2025 and 3.5% in 2030, with the possibility of using double counting (thus meeting the 2030 objective with a real incorporation rate of 1.75%, for example). In the European Commission's latest proposed revision, a minimum incorporation rate of 0.2% would be required in 2022, followed by 0.5% in 2025 and 2.2% in 2030 without double counting. Depending on the evolution of energy consumption in the European transport sector during this period, the objective would imply the deployment of between 8 and 10 Mtoe of advanced biofuels, while current consumption amounts to a little under 1.3 Mtoe.

In France, the PPE (long-term energy plan) requires the deployment of 3.8% of advanced biofuels in the gasoline pool and 2.8% in the diesel pool by 2028. Since ethanol derived from wine alcohol contributes to achieving less than 1% of the objective for the gasoline pool and is currently close to its maximum level, it is necessary to consider the development of other options, such as lignocellulosic ethanol and synthetic diesel fuels, kerosene and gasoline derived from lignocellulosic biomass. Within the framework of the French Energy-Climate Strategy (SFEC) currently being rolled out, the French Energy Climate Planning Bill (LPEC) is due to come into effect by July 2023. New versions of the country’s National Low-Carbon Strategy (SNBC3), the National Climate Change Adaptation Plan (PNACC3) and the Long-Term Energy Plan (PPE 2024-2033) will then be adopted, probably incorporating revised objectives for advanced biofuels.

On the industrial side, the European Union already has advanced biofuel production capacities in existing FAME, HVO and ethanol units, but sugar and oil resources set out in annexes IX-A (tall oil, algal oils, wine alcohol, etc.) are available in very limited quantities for technologies of this type. New, second-generation ethanol units mobilizing lignocellulosic biomass are currently being developed to supplement capacity. There are six projects in the EU (see 2019 biofuel dashboard), including the Clariant lignocellulosic ethanol unit in Romania, commissioned at the end of 2021. Concerning Fischer-Tropsch or BtL technology for the production of synthetic biofuels, the UK (4 units) and the USA (4 units) are ahead of the field in terms of commercial unit projects.

There are also an increasing number of trials focusing on alternative fuels for sea and river transport vessels. Biodiesels, bio-LNG, ammonia, biomethanol and hydrogen are the main liquid fuels under consideration. Alongside the European initiative for the aviation sector, the Commission has proposed the RefuelEU Maritime initiative. The proposal is based on objectives for the reduction of greenhouse gas emissions resulting from operating vessels, taking average emissions recorded in 2020 as a starting point. These reduction levels will be determined during a future stage of the legislative procedure for different categories of vessel.

In terms of investments, in the short term, new production capacities are likely to concern the ethanol and biodiesel sectors, with a tripling of HVO production capacities planned by 2025. The USA leads the field currently in terms of active zones, but there are also several projects in Asia, Brazil and the EU. Concerning ethanol, the main active zones are Brazil and China, who currently represent half of all global investments. However, several projects have been delayed, particularly in Thailand and Brazil, due to the fall in the demand for fuel caused by the health crisis. Investments in advanced biofuel production processes are also being launched, with six projects in India and as many again in Eastern Europe. Similarly, investments are accelerating in the field of biomethane fuel, particularly in Europe and North America, while Brazil, India and China are also encouraging its use in the transport sector. Some oil companies (Total, BP, Shell and Chevron, in particular) are actively involved in developing the sector.

Daphné Lorne - daphne.lorne@ifpen.fr

[2] NGV: Natural Gas for Vehicles

[3] Incorporation rate taking into account multiple counts

[4] Directive 2009/28/CE relating to the promotion of the use of energy produced from renewable sources

[5] E100: gasoline vehicle fuel made up of 100% vol. ethanol

[6] FAME: Fatty Acid Methyl Ester

[7] HVO: Hydrotraited Vegetable Oil

[8] RFS2: Renewable Fuel Standard, July 2010 version

[9] LCFS: Low Carbon Fuel Standard

[10] PFAD: Palm Fatty Acid Distillate

[11] ILUC (Indirect Land Use Change) risk: greenhouse gas emission risk associated with indirect land use changes

[12] ASTM International: American Society for Testing and Materials International

[13] https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52021PC0557

[14] SAF: Sustainable Aviation Fuels

[15] CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation): https://www.icao.int/environmental-protection/pages/climate-change.aspx

[16] HEFA-SPK: Hydroprocessed Esters and Fatty Acids – Synthetic Paraffinic Kerosene

[17] FT-SPK: Fischer-Tropsch – Synthetic Paraffinic Kerosene

[18] ATJ-SPK: Alcohol-to-jet - Synthetic Paraffinic Kerosene

[19] Source: https://www.icao.int/environmental-protection/pages/SAF.aspx

[20] SP95-E10: Lead-free 95 gasoline containing up to 10% by volume bioethanol

[21] TICPE: A French domestic consumption tax on energy products

[22] HVHTE: Huiles végétales hydrogénées de type essence (synthetic gasoline hydrogenated from vegetable oils)

[23] VOME: Vegetable Oil Methyl Ester

[24] HVHTG: Huiles végétales hydrogénées de type gazole (synthetic diesel from hydrogenated vegetable oils)

[25] https://www.etipbioenergy.eu/everyone/advanced-boifuels

You may also be interested in