01.09.2017

30 minutes of reading

Biogas, produced from all kinds of organic matter, is used to produce electricity and heat. Biomethane, which is biogas stripped of its CO2 component, can be injected into the natural gas network or upgraded to biofuel for use in the transport sector. In Europe, biogas represented 8% of renewable fuel production in 2015, equivalent to 4% of European natural gas consumption.

Biogas production methods and use

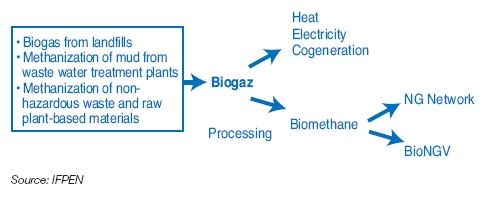

The notion of biogas refers to all gas products resulting from a biological or physico-chemical conversion of biomass/biowaste. Biogas can be burned for use as heating and/or electricity, or refined to extract methane and meet regulatory requirements (CO2 content, etc.). Biomethane can then be injected into natural gas networks or used as fuel (bioNGV)1.

Biogas is produced by recovering it in non-hazardous waste storage facilities (ISDND or “landfills”) or through methanization (Ref. 1; Fig. 1). This allows recycling of non-hazardous biowaste (from agriculture, industry, household waste, etc.), plant-based materials and mud from waste water treatment plants (WWTP)2.

Other biomethane production methods are being tested or are in the demonstration phase, such as gasification of biomass from lignocellulosic resources, and Power to Gas, which uses electrolysis of water to produce hydrogen.

In these two options, biomethane is produced by CO2 methanation through reaction with hydrogen. Methanization of microalgae is another solution proposed for the long-term.

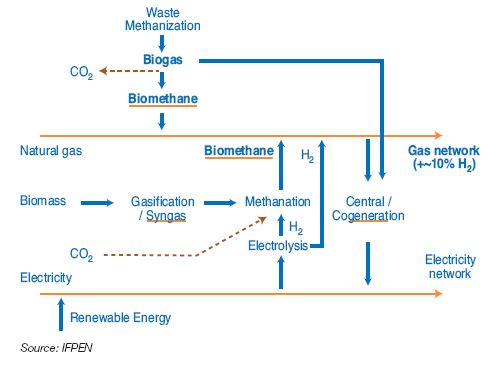

Figure 2 offers some idea of an integrated energy diagram that involves the gas and electricity networks. Mature production methods (methanization) and those being considered (methanation) are represented in this diagram.

gas/electricity/hydrogen diagram

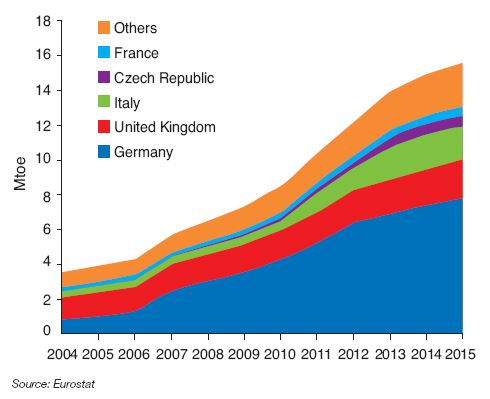

Germany produces one-half of European biogas

Germany is the leading biogas producer in Europe with a total of 7.8 Mtoe in 2015, representing one-half of European production (Fig. 3). The United Kingdom and Italy both produce approximately 2 Mtoe. Together, these three countries make up 80% of the European total. France ranks 5th among European countries, with 0.5 Mtoe.

For all 28 countries in the European Union, biogas production, 50% of which comes from energy crops, reached 15.6 Mtoe in 2015. This biogas is mainly used for electricity (62%) along with heating (27%). The balance (11%) is converted to biomethane to be injected into traditional gas networks, or used by the transport sector (Ref. 2).

In 2015, biogas fuel represented only 0.13 Mtoe in Europe, compared with 14 Mtoe for biofuels. Growth in European biogas production has slowed since 2014.

From an average of 13% per year since 2010, the average annual growth rate fell to 7% in 2014, then to 4% in 2015. Specifically, changes in German and Italian policy explain this turnabout. In both cases it favors the use of by-products and agricultural waste rather than the use of energy crops (Ref. 3).

In France, methanization has developed more recently, and has intentionally favored the use of biowaste, especially manure. To reconcile the development of biogas plants with respect for land use issues, a 2016 decree caps the use of energy crops at biogas plants at 15%.

These provisions fall within the scope of non-binding European Union recommendations on biomass sustainability criteria (for energy facilities of at least 1 MW). They are intended to prohibit the use of biomass from converted land, forests and areas with high levels of biodiversity (Ref. 4).

A minimum two-fold increase in European production envisioned by 2030

A study conducted on behalf of the European Commission (Ref. 2) estimated potential biogas production from waste at between 30 and 40 Mtoe by 2030, around 3% of European energy consumption and approximately 10% of gas consumption within that timeframe.

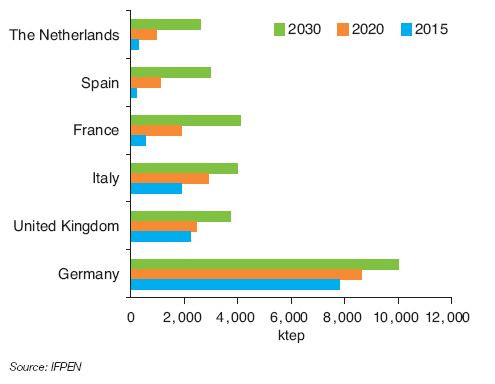

For France, the potential is estimated at 4 Mtoe in 2030, a volume equal to that produced by the United Kingdom and Italy (Fig. 4). A 2013 study by ADEME (Ref. 5) assessed the exploitable potential through methanization at 4.3 Mtoe (56 TWh) in 2030, i.e. a volume similar to that established in the European study. Some analyses predict a potential in excess of 8 Mtoe (100 TWh) by 2040 (Ref. 6).

However, production costs for renewable energies produced through methanization is still high compared to market rates. A study by Irena (Ref. 7) mentions costs of biogas production and processing of €30 to 150/MWh, highly dependent on inputs (energy crops, manure or waste) and installed capacities. By way of comparison, European gas prices have fluctuated between €15 and 30/MWh since 2014.

Assistance is therefore essential to support the industry. The European report emphasizes the importance of an effective and stable policy for deployment and investment in the biogas sector. Therefore, European regulations for the period following 2020 will be critical to achieving the identified volumes.

A proactive policy for France

In France, the 2015 energy transition act for green growth aimed to increase the share of renewable energies in gross final energy consumption to 32% in 2030, compared with 14% in 2014. More specifically, renewable energies should represent 10% of gas consumption within this same timeframe.

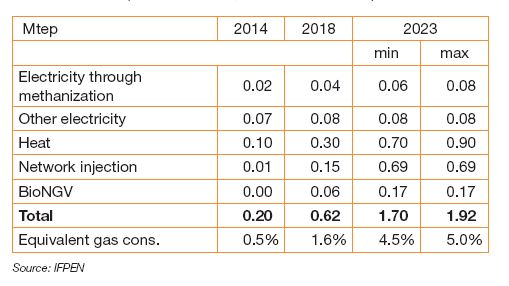

The multi-annual energy program (PPE) will establish concrete growth objectives for various renewable electricity production industries by 2023 (Ref. 8 and 9). Regarding biogas, objectives are defined based on usage, specifically electricity production, heating or bioNGV, as well as biomethane injection. The objectives proposed in October 2016 are very ambitious and require the shortterm completion of a large number of projects.

In addition, to produce electricity through methanization, the PPE provides for installed capacity of 137 MW in 2018 and 240 to 300 MW in 2023, compared with 110 MW in 2016. For other processes (ISDND and WWTP: 280 MW in 2016), there are plans to equip existing sites with electricity production methods when it is economically justified and neither biogas injection into the network nor heating production is possible. Currently, the total installed power of these various industries is equal to 390 MW, which remains modest compared with 1,700 MW for the overall bioenergy industry, and 10,300 MW for onshore wind energy.

The plan is to support development of bioNGV, to reach 0.7 TWh consumed in 2018 and 2 TWh in 2023, on the assumption that bioNGV would represent 20% of NGV consumption by that date. Finally, biomethane injection into the gas network could reach 0.7 Mtoe (8 TWh) in 2023 compared with 0.02 Mtoe (0.2 TWh) in 2016, numbers to be compared with natural gas consumption of 38 Mtoe in 2016.

With regard to other biomethane production methods (excluding PPE), various studies estimated the technical potential in France by 2040 between 14 and 24 Mtoe (160 to 280 TWh) for gas from gasification, and between 1 and 3 Mtoe (15 to 40 TWh) for “power to gas” (Ref. 10).

Nevertheless, technical and economic constraints must be addressed if there is hope to achieve this level of recovery.

(base 2016 PPE, IFPEN calculations)

Power to gas

Electrolysis of water enables production of hydrogen through an electrolyzer. Hydrogen can be recovered directly or converted to biomethane through methanation.

Over the long term, these two methods are intended to recover surplus from the electricity market available in an intermittent renewable energy system and store it in gaseous form. Hydrogen could be integrated into a broader energy system to address demand for mobility using fuel cell electric vehicles.

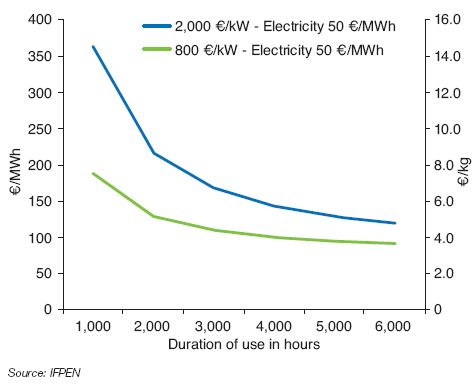

Nevertheless, its production cost when using electrolysis remains relatively high, between €100 and 200 MWh for an electricity price of €50/MWh and a production time in excess of 2,000 hours per year (Fig. 5).

duration of use of electrolyzer

Biogas allows for reduction of greenhouse gas emissions

The biogas industry fits within the objectives of the energy transition, allowing reduction of greenhouse gas emissions and the development of a circular economy due to recovery of digestates from methanization in agriculture.

An ADEME-GRDF study shows that growth in the biomethane industry, as a substitute for natural gas, helps to reduce greenhouse gas emissions by 188 grams of CO2 equivalents for every kWh produced, injected or consumed. This would represent at least 750,000 tons of CO2 equivalents per year in France, for an amount of biomethane assessed at 0.3 Mtoe (4 TWh) within this timeframe (Ref. 11).

In the case of a regional methanization project with reinjection into the network, an LCA analysis performed by IFPEN gave similar results (Ref. 12). Thus, biowaste methanization offers very significant environmental benefits.

However, work remains to be done to specifically assess environmental impacts based on the type of inputs.

A European study (Ref. 2) also emphasized the advantages with regard to greenhouse gas emissions. It highlights the benefits, regardless of the use of the biogas. Nonetheless, the impact is greatest when used in transport (bioNGV) as a replacement for diesel, with an 80% reduction in greenhouse gas emissions.

For new electrical facilities exceeding 1 MW, European Union recommendations specify that bioenergy sources emit 50% less greenhouse gases during their life cycle (cultivation, conversion, transport, etc.) compared with fossil fuels in 2017, then 60% less in 2018, compared with an earlier 35% threshold (Ref. 4).

Financial support is needed for biogas development

In the absence of price competitiveness in the current market, development of biogas and biomethane requires public support in a variety of forms. Feed-in tariffs are the most common measure, currently used by countries such as the United Kingdom, Italy and Germany. Sweden has implemented a tax exemption on energy and CO2 for biomethane used in transport.

In France, the terms of sale for electricity produced by facilities primarily using biogas through methanization were amended at the end of 2016 (Ref. 13). The base rate is €175/MWh for electrical output below 80 kW, and €155/MWh between 80 and 500 kW, to be compared with a market price for electricity of €40 MWh in 2016. This base rate will decline by 0.5% every quarter starting on January 1, 2018. Above 500 kW, a call for tenders has been proposed for new facilities.

For biomethane injected into the gas network, there has been a support system in place since 2011 (Ref. 1). The guaranteed purchase price over 15 years varies between €45 and 95/MWh for non-hazardous waste storage facilities, and between €64 and 95/MWh for other facilities (excluding premiums of €1 to 39/MWh based on inputs).

As with electricity, these rates are significantly above current market prices for natural gas in Europe, which are around €15/MWh in 2016, i.e. approximately one-half of the historically high 2013 price.

The existence of waste funds and heating funds should also be highlighted. The first type of fund finances digestate processing equipment and methanization projects with recovery of biogas produced through cogeneration. The heating

funds finance methanization projects with direct recovery of heat (and associated heat networks) as well as projects to inject biomethane into gas networks (Ref. 1).

Biogas, a legitimate energy source for the energy transition

In Europe, the potential for biogas is estimated at 30/40 Mtoe, equivalent to 10% of gas consumption by 2030. In France, objectives by industry as defined by the PPE in 2016 may achieve nearly 2 Mtoe in 2023 (0.5 Mtoe in 2015), a volume equal to nearly 5% of the country’s gas consumption.

Such volumes will not disrupt the energy environment, but contribute to the gradual deployment of renewable energies.

Biogas offers numerous benefits that fit perfectly within the energy transition and the circular economy. It enables production of storable renewable energy that can be substituted for fossil fuels. In addition, methanization offers a solution to the intermittent nature of solar and wind energy, and provides an option for waste treatment. Finally, digestate, a residue from methanization, can be used as a fertilizer that can replace mineral and chemical fertilizers.

Biogas presents a number of challenges, specifically higher costs that require significant financial support from the government. Beyond the impact of scale effects, research is being conducted in Europe to try to reduce them, specifically optimizing returns from digesters and purification technologies (Ref. 14).

Guy Maisonnier – guy.maisonnier@ifpen.fr

Julien Grandjean – julien.grandjean@ifpen.fr

With the support of Anne Bouter, Pierre Collet, Thierry Gauthier

Final draft submitted in September 2017

(1) Natural Gas Vehicle

(2) French Ministry definition for the three biogas processes: methanization of non-hazardous waste and raw plant-based materials; methanization of mud from waste water treatment plants (WWTP); biogas from non-hazardous waste storage facilities (ISDND)

APPENDIX

IFPEN and biogas

Biogas processing

IFPEN mainly operates within the processing component of the biogas chain. This phase is essential to achieving gas quality that is consistent with its injection into the natural gas network, or its use as fuel (bioNGV).

Biogas purification, which eliminates undesirable components, generally involves three stages:

- dehydration to eliminate water;

- desulphurization to remove highly corrosive H2S;

- decarbonation, or upgrading, to eliminate carbon dioxide (must comply with maximum content of 2.5 to 6% in Europe).

Decarbonation, which is the main step in purification, can be achieved through various technologies, of which the most widely used are PSA (pressure swing adsorption), membrane technology, physical absorption via washing with water or an organic solvent, chemical absorption through amine scrubbing.

IFPEN developed an amine scrubbing procedure using a new molecule, capable of reducing energy consummation in the purification stage.

Implemented by Arol Energy as part of an exclusive partnership, the AE-Amine process displays extensive thermal integration between the purification stage and methanization digesters, and offers a significant reduction in heating needs during the upgrading phase compared with traditional amine technology.

This innovation improves biomethane productivity achieved with amine technology, reaching a level comparable to ther technologies, while retaining the benefit of lower energy consumption by a factor of 3 to 4. This lower production cost improves operating results by 15 to 20% for medium to large facilities starting from 300 Nm3/h of biogas.

The AE-Amine technology also provides higher-purity biomethane and CO2 production, more than 99.5% CH4 and 99.9% CO2 respectively. Residual CO2 content in biomethane can be adjusted for injection into the network or production of bioLNG.

As part of the Biomet project supported by ADEME and the future investment program, AE-Amine is currently being tested at the Terragr’eau facility in Évian (France). This purification unit, which represents the first demonstration of amine technology in France, can process up to 250 Nm3/h of biogas, which has been injected into the network since March 2017.

REFERENCES

(1) MTES Biogaz

(2) Optimal uses of biogas from waste stream – European Commission - Dec. 2016

(3) Biogas barometer 2014 – EurObserv’ER

(4) Biomass – European Commission

(5) Estimation des gisements potentiels de substrats utilisables en méthanisation – Ademe – 2013

(6) NégaWatt scenario 2017 – 2050 - Negawatt

(7) Biogas for Road Vehicles | Technology Brief – 2017 ; Irena

(8) Decree no. 2016-1442 of October 27, 2016 relating to multiannual energy programming.

(9) PPE Volet offre – MTES 2016

(10) Production de biométhane : de nouveaux procédés en développement – GRDF

(11) Évaluation des impacts GES de l’injection du biométhane dans les réseaux de gaz naturel” – GRDF

(12) Étude d’impact environnementale basée sur la méthodologie ACV d’un projet de méthanisation territorial – IFPEN, A. Bouter, T. Gauthier

(13) Conditions de rémunération de l’électricité... – Légifrance – Order dated December 14, 2016

(14) IEA Bioenergy 2014

Other sources

(15) Club Biogaz – ATEE

(16) Publications et tableaux de bord – MTES

(17) Biométhane – Cegibat

(18) Baromètres EurObserv’ER

(19) Energy from biogas – IEA

(20) Biogas Potential in the United States – NREL