01.06.2018

30 minutes of reading

In 2017, spending on oil and gas exploration fell by 10%, while investments in E&P recovered slightly (+ 4%). Despite more than 200 discoveries, volumes discovered in 2017 fell 13% over one year, representing only around 11 billion barrels of oil equivalent (boe) in gas and liquids. Major discoveries are becoming increasingly rare. The most significant in 2017 is a gas deposit off the coast of Senegal (2.7 Gboe). However, new regions continue to emerge. Following major gas discoveries in the eastern Mediterranean and East Africa, offshore Mauritania and Guyana are coming into fruition. Overall, offshore holds a dominant position, with the largest discoveries and 75% of new volume for the year. Gas represented approximately 50% of volumes discovered.

Global spending on exploration

IFPEN estimates that 2017 worldwide spending on exploration was $41 billion, a 10% drop over one year. Since peaking at $100 billion in 2014, spending fell sharply by 35% in 2015 and 33% in 2016, thus tracking the decline in oil prices (Fig. 1).

The modest 4% increase in worldwide upstream investments (exploration and production) during 2017 (IFPEN report on “investments in petroleum equipment and services in 2017”) only moderately benefitted spending on exploration, since most global E&P investments concerned the development of non-conventional crudes in the United States.

This decline in exploration, expressed in dollars, must be weighted against E&P costs that have fallen between 30 to 50% since 2015, depending on sector.

between 2007 and 2017

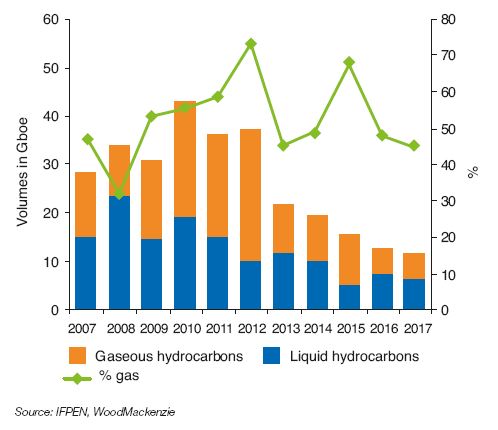

Volumes of oil and gas discovered

Spending on exploration rose by nearly 60% between 2010 and 2014. However, volumes discovered steadily declined, falling from nearly 40 Gboe in 2010 to less than 20 Gboe four years later (Fig 2).

Between 2015 and 2017, the upstream spending and investment cycle has reversed, triggering a 60% decline in spending on exploration. In 2017, discovered volumes are estimated at around 11 Gboe, a 13% decline over one year and representing just half of 2013 levels.

The number of discoveries is not at issue, however, with more than 200 made in 2015, 2016 and 2017. This downward trend is mainly attributable to a reduced number of massive discoveries, the extent of the Brazilian pre-salt layer (from 2006) and the Rovuma basin in Mozambique and Tanzania (from 2010). During 2016 and 2017, the share of discovered gas volume ranged from 45% to 48%, nearly half of the total (oil and gas) volumes discovered.

In today’s dollars, and by barrel equivalent discovered, there has been a decline in exploration costs from $5.5/boe to $3.5/boe between 2015 and 2017. Costs in E&P services fell by around 50% over the same period. Over the past three years, it is estimated that the discovery of one barrel of oil equivalent requires 15% greater effort during exploration. Areas being explored are in deeper waters and are more complex from a geological point of view.

In 2017, with worldwide oil production of 98 Mb/day, i.e. 36 Gboe/year, oil discoveries (6 billion barrels) have not come close to making up for annual production. Given the depletion of existing fields (3.5% per year), the oil sector must replace 3 Mb/day each year (1.1 Gb/year), equivalent to North Sea production, while also meeting increased demand (0.54 Mb/day), i.e. 0.2 Gboe/year according to BP Energy Outlook. In sum, taking stock of 2017, there is a shortfall or 36 + 1.1 + 0.2 – 6, i.e. 31.3 Gboe to be drawn from the 1,700 Gboe of proven oil reserves.

However, this short-term trend must be considered in light of the fact that global proven oil reserves rose by 23% over 10 years (BP Statistical Review), increasing the proven reserves to production ratio to 52 years. The reassessment of reserves, thanks to a better understanding of reservoirs, has permitted the discovery of satellite fields and reconsideration of volumes. Other reassessments may be political and/or include heavy crude or non-conventional oil reserves. On the other hand, EOR (enhanced oil recovery) by gas injection (CO2 and HC) and thermal methods have contributed 3 Mb/day to global production.

The main discoveries of 2017 by region

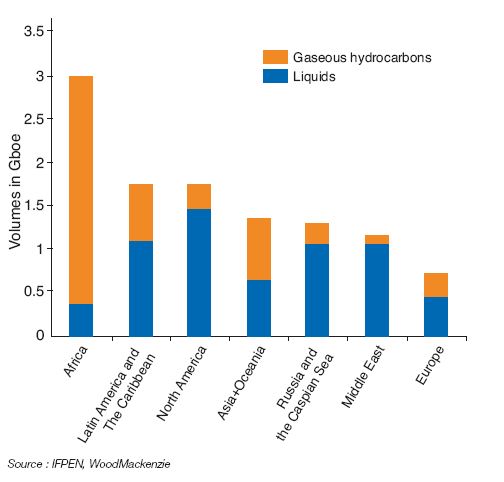

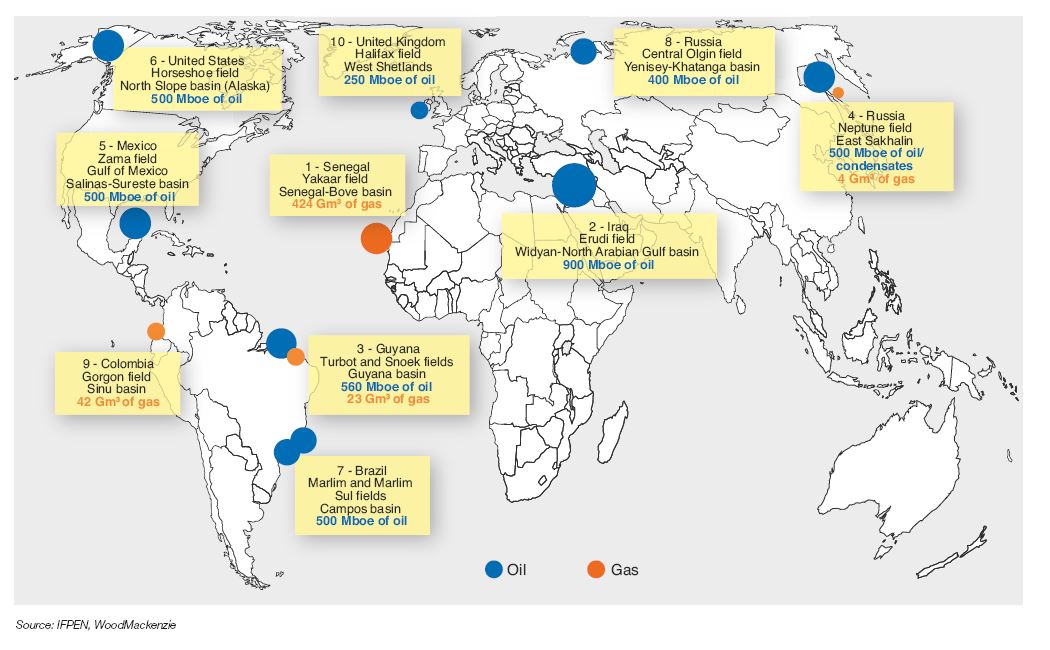

In 2017, Africa was in the forefront (Fig. 3) of worldwide discovery with 27% of volumes, despite posting a 9% decline over one year. The massive Yakaar gas discovery (Tab. 1) in Senegal (424 Gm3 of gas, i.e. nearly 2.7 Gboe) by Kosmos BP confirms the scale of the petroleum system off the coast of Senegal and Mauritania. After the Marsouin gas discovery (42 Gm3) in 2015, followed by Tortue (212 Gm3) in 2016, this new deposit, located 40 km west of the earlier Teranga discovery (141 Gm3) in 2016, could justify the creation of a second LNG hub.

Other discoveries in Africa were comparatively minor. The largest in this region was made back in 2015 with the Zohr discovery (3.9 Gboe) in Egypt by ENI. There was also a significant decline in exploration in the Gulf of Guinea and East Africa.

With regard to oil and gas discoveries, South America was roughly equal to North America as the second most prolific region, with 16% of volume. South America doubled the volume of its discoveries when compared with 2016. In Guyana, ExxonMobil made two additional oil discoveries in the Stabroek block during 2017 with the Turbot-1 well (350 Mboe) drilled 50 km from the Liza project and the Snoek-1 well (350 Mboe). The Liza field was discovered in 2015 due to a study of the West Africa and South America conjugate margins. Discoveries followed in 2016 with Payara (500 Mboe) and Liza Deep (200 Mboe). The entire Stabroek block may hold between 2.5 and 2.75 Gboe. Exploitation of this oil could be a game-changer in this small nation, which is one of the poorest in South America. Exploration is very active in neighbouring Suriname.

In Brazil, Petrobras continues exploration of the pre-salt layer in the Campos basin, and discovered 300 Mboe in the Marlim field and 200 Mboe in Marlim Sul (Poraque Alto well). This mature basin has the benefit of infrastructure needed to develop the reserves.

In Columbia, Anadarko uncovered 42 Gm3 of gas reserves, following the Gorgon-1 exploration wells in its southwest territorial waters in the Caribbean Sea. In 2015, Anadarko had already discovered 28.3 Gm3 of dry gas while drilling the Kronos-1 well in the same basin (Sinu). They were the largest discoveries in this country since Cuisiana and Cupiagua in 1989, and should enable the country to alleviate its declining oil reserves.

North America is ranked third in terms of discoveries (1.7 Gboe), with 16% of volumes. During 2016, Alaska had already made two significant discoveries with Tulimaniq (1.8 Gboe) and Willow (300 Mboe). In 2017, the North Slope basin continues to yield large volumes with the Horseshoe discovery (500 Mboe). In Mexico, volumes have been discovered offshore in the Zama oil field (500 Mboe) and onshore in the Ixachi gas field (38 Gm3).

With 12% of annual discoveries in 2017, Russia increased its volume of oil and gas discoveries by 50%. Gazpromneft found a large oil deposit (537 Mboe) in the Neptune field in the Sea of Okhotsk, in the East Sakhalin basin, as well as Rosneft, in the Laptev Sea within the Yenisey–Khatanga basin (400 Mboe). Other discoveries outside the Russian Federation were smaller and concerned onshore gas fields in Turkmenistan (Uzynada Deep and Osman).

Volumes discovered in Asia increased by 70% compared with 2016. 1.3 Gboe was discovered, i.e. 12% of the worldwide total. This includes 250 Mboe of shales (Dinhye and Yuxi-Zu) discovered in China, approximately one-third of the country’s discoveries. Other discoveries, numbering 45, were mainly found in China (500 Mboe), as well as Myanmar (160 Mboe), Indonesia (116 Mboe), India (100 Mboe) and Pakistan (86 Mboe).

With 1.1 Gboe, the Middle East represented 10% of volumes discovered, down 50% compared with 2016. However in 2017, 150 km west of Basra in Iraq, Lukoil made a significant onshore oil discovery (Tab. 1) in the Eridu field (900 Mboe). Other discoveries were smaller and were primarily made in Oman (205 Mboe) with the discovery of 14 Gm3 of gas in Mabrouk NW and, in Iran, with the discovery of 50 Mboe of oil in Araya. Only one-half of the amount of oil and gas was discovered in this region compared with 2016, and four times less than in 2015. Given the modest price of oil in 2017, the Middle East, with the world’s largest oil reserves, does not give priority to investments in exploration in order to expand its reserves. This is especially true since this region also has non-conventional resources that can be developed at a future date. In early April 2018, the small island nation of Bahrain, with declining production, announced the discovery of massive shale oil resources that may enter production within five years. An initial well will be drilled this summer for evaluation.

Europe ranks last with only 7% of discovered volumes in 2017, a 20% decline compared with 2016. Nevertheless, the discovery of the Halifax oil field in the Western Shetlands in the United Kingdom (250 Mboe) is one of the ten largest discoveries of 2017. In Norway, the Barents Sea contains several oil and gas discoveries, including Filicudi (70 Mboe), Korpfjell (60 Mboe) and Kayak (40 Mboe). In Cyprus, Total made a deepwater discovery of 90 Mboe of gas in Onisiforos.

Fig. 4 – Les dix premières découvertes de 2017 en pétrole et gaz

Significance of offshore in volumes discovered

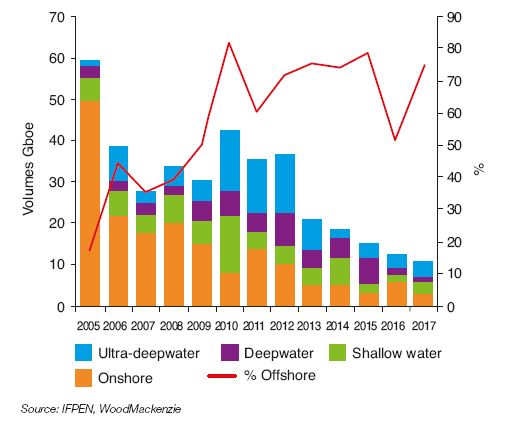

Since 2010, most discoveries (75%) have been made offshore (Fig. 5). During 2017, 14 fields were discovered in extra-deep offshore waters, in more than 1,500 metres of water. Extra-deep offshore waters represent 4 Gboe, i.e. 36% of volumes discovered. These include three of the ten largest discoveries in 2017, including two in more than 2,000 metres of water: Gorgon in Colombia and Yakkaar in Senegal, and in 1,500 to 2,000 metres of water: Snoek and Turbot in Guyana.

Deep offshore waters offer the possibility of discovering additional new regions to be developed. This mainly benefits the majors, given the cost of drilling and project development, as well as major independent companies which assume the risk of exploration.

Certain major national companies such as Petrobras and Statoil, which have significant maritime resources, have developed the technology needed for production in very deep water under difficult conditions (HP, HT).

Volumes discovered by operator

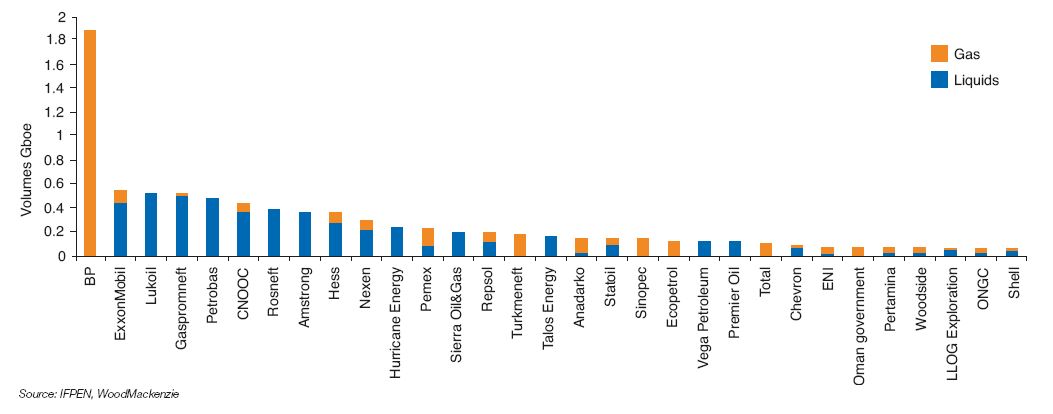

BP made the largest discoveries during 2017, with nearly 2 Gboe of gas (Fig. 6) distributed among Senegal (Yakaar), Trinidad and Tobago (Savannah and Macadamia) and Egypt (Quatameya). ExxonMobil was ranked second with three discoveries in Guyana (Snoek, Turbot and Ranger) and two in Africa: Nigeria (Erha Northeast Deep) and Equatorial Guinea (Avestruz), primarily oil in deep and ultra-deep offshore waters. Volumes discovered by Lukoil came almost exclusively from the Eridu field, a major onshore discovery in Iraq. Likewise, Gasprom’s fourth place position mainly results from the Neptune oil and gas field discovered at Sakhalin. Petrobras owes its success to two offshore oil discoveries in the Campos basin (Marlim and Marlim Sul). CNOOC found a total of 0.45 Gboe with 15 mid-size oil discoveries, mainly in Chinese offshore regions. Rosneft was responsible for the Olginskoye offshore oil discovery. Armstrong owes its position to one discovery, Horseshoe in Alaska. Hess holds a 30% interest in the Guyana discoveries made with ExxonMobil, along with Nexen which holds a 25% interest. Hurricane Energy was responsible for the Halifax oil discovery in the Shetlands.

In 2017, the discoveries requiring the largest investments were made by national companies: Pemex, Statoil, Petrobras, CNOOC. With more than $800 million in expenditures, Pemex’s efforts yielded few results, with only the Ixachi onshore discovery (Zama was discovered offshore by Talos Energy). Putting this into perspective, deep offshore drilling may cost between $100 and $200 million, compared with ten times less onshore.

Factors limiting exploration

To increase its reserves and production, an operator may also opt to merge or acquire another operator. By acquiring Maerk Oil for $7.5 billion, Total increased its reserves by 1 Gboe and its production by 160,000 boe/day.

Contrary to the launch of production of conventional hydrocarbons, the development of shale oil and gas in the United States was achieved without the use of major seismic exploration surveys. The operator learns to understand its reservoir and estimate its reserves at each drilling.

Major national companies have substantial reserves compared with their annual production. In the Middle East, they are not required to spend billions on exploration while their R/P ratio is high, and there is a need for OPEC countries to lower production.

Conclusion

Spending on exploration has fallen by 60% over three years. It is directly linked to declining investment by oil and gas operators, which have suffered from a 50% drop in oil prices since 2014.

The merger or purchase of an operator by another is one strategy for acquiring and supplementing a reserve portfolio while limiting exploration and the risk of failure. On the other hand, the rise in shale oil and gas production has occurred without the need for an intensive exploration campaign. Major Middle East national companies hold vast reserves and currently have no immediate need to replenish them.

Overall, with more than 200 discoveries, the volumes discovered in 2017 fell 13% over one year and represent around 11 Gboe in gas and liquids. Major discoveries are becoming increasingly rare. The most significant discovery of 2017 was a gas deposit off the coast of Senegal (2.7 Gboe). However, new regions are constantly emerging. Following major gas discoveries in the eastern Mediterranean and East Africa, offshore Mauritania and Guyana continues to develop.

For the past two years, gas has made up nearly 50% of volumes discovered. Offshore holds a dominant position in exploration, with 75% of volumes discovered. The largest discoveries have been made offshore.

During 2018, there have already been significant discoveries such as Ballymore made by Total, in 2,000 metres of water in the eastern Gulf of Mexico, and in Bahrain where massive shale oil resources will be drilled for assessment.

Sylvain Serbutoviez – Sylvain.Serbutoviez@ifpen.fr

Final draft submitted in June 2018