01.02.2018

30 minutes of reading

The decline in CO2 emissions from road vehicles is essential to the sustainable reduction of greenhouse gas emissions. At the global level, the transport sector represents a 23% of total greenhouse gas emissions. In France, this sector plays a comparatively greater role; in 20141 it was responsible for 28.5% of greenhouse gas emissions, making it the largest emitter, far ahead of the agriculture (17%) and residential/tertiary (16%) sectors. To reduce greenhouse gas emissions in the transport sector, solutions depend on the development of new engine technologies, biofuels, new fuels and zero-carbon alternative energies. In addition to lowering greenhouse gas emissions, these solutions provide additional benefits, such as improving local air quality (especially in the case of electric vehicles) and reducing oil imports.

Historically close ties between transport and oil

An energy transition needed for transport

The Paris Climate Accord, signed in December 2015, aims to move society toward a low-carbon economy for the end of the century. France has set the additional goal of carbon neutrality by 2050. Every sector must contribute to reaching this ambitious goal. Like the electricity production sector, which increasingly integrates renewable energies, the transport sector has committed to an energy revolution. However, due to the low turnover rate of the automobile fleet, this could occur at a slow pace. However, even though the transport sector is not the sole emitter of particulates in the atmosphere, the fact that certain cities are starting to ban older diesel vehicles – as Stuttgart did after Dieselgate – could single-handedly hasten transformation of the fleet.

To achieve this, the European Union’s goals for reducing greenhouse gas emissions and treatment of local pollution must combine improvements in combustion engine efficiency with the development of alternative energies and engines such as hybridization, biofuels, electric engines or fuel cells. At the same time, exhaust after-treatment systems should also continue to expand.

Constructing medium or long-term scenarios, and anticipating technological breakthroughs, radical changes in public policy and changes in user behavior remain difficult. Despite everything, alternatives based on existing technologies currently allow direct reductions in greenhouse gas emissions in the transport sector. This memo sets forth these alternatives, though it does not address vehicle natural gas (VNG). Given its potential to reduce greenhouse gas emissions (especially in its bio VNG form) and particulates, VNG will be the subject of a future Panorama memorandum.

Biofuels: significant growth, slowed by an uncertain regulatory framework

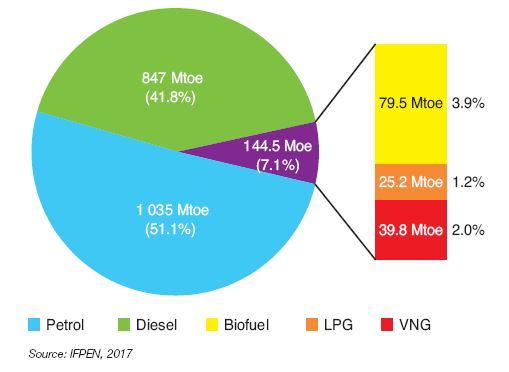

Worldwide energy consumption in the road transport sector rose by nearly 2 billion toe. During 2015, alternatives to gasoline and diesel continued to expand, representing 7.1% of fuels consumed. Among these alternatives (biofuels, liquified petroleum gas (LPG), vehicle natural gas (VNG)), biofuels represented 79 Mtoe (Fig. 2). Their consumption rose by nearly 14% between 2014 and 2015, while demand for road fuels only grew by 3.1%.

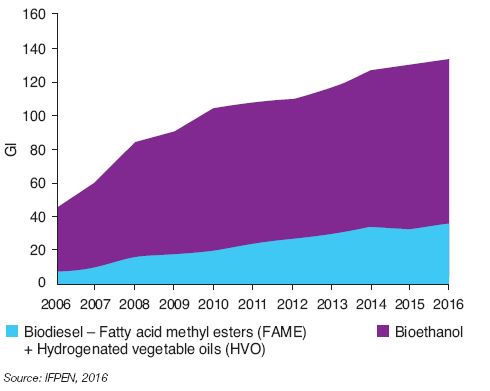

Worldwide consumption of biofuels in the transport sector has grown sharply since they debuted in the early 2000s (Fig. 3). However, blend rates in the fossil fuel pool has grown at a more moderate rate since 2011, given ongoing regulatory uncertainties, especially in Europe.

Latin America posted the highest overall biofuel blend rate of more than 10% (in energy). North America and Northern Europe followed, posting rates of approximately 6% and 4% respectively (in energy). While Asia has only substituted around 1% of its road fuel consumption, it is nevertheless a region where the most dynamic pro-biofuel investments and public policies are found. At present, only Finland, Sweden and Austria have achieved the consumption objectives set forth in the Renewable Energy Directive proposed by the European Commission, which set a 10% target for energy from renewable sources in transport by 2020. In France, the biofuel blend rate was 8.5% in 2015.

Following three years of decline, global investment in biofuels began to rise in 2017, revived by several key factors:

- significant growth in Asian countries for supply security;

- ongoing growth in supply of biomass from South America;

- the transition to new-generation biofuels in Europe, whose resources do not compete with food-related uses;

- the United States tendency to increase its ethanol exports (24 Mb exported in 20162).

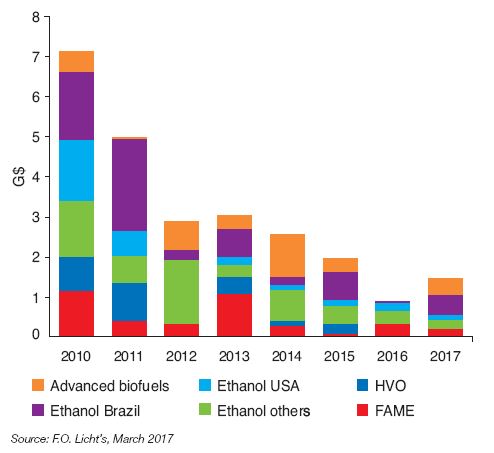

Thus, we expect global biofuel demand to rise sharply in the coming years, driven by North America and Asia. This is illustrated by the amount of investments trending upward in 2017 (Fig. 4). According to its goals set forth in its Renewable Energy Directive (REDII) to prepare for conventional and advanced biofuels, Europe may also contribute to rising global demand for biofuels.

Production capacity for conventional biodiesel made from hydrogenated vegetable oil (HVO) is growing. Examples include the upgrade to the Diamond Green Diesel unit in Louisiana, increased capacity of the ENI unit in Porto Marghera and the imminent opening of the Total unit at La Mède refinery in France.

In the short term, advanced biofuels made from ligno-cellulosic biomass could also emerge quickly. The first commercial ligno-cellulosic biomass ethanol units were launched in 2013, with projects in the United States, Brazil and Europe. More recently, the Indian and Chinese markets began to drive the growth of this technology (more than 12 projects announced in India during 2018.

Today there are more than ten commercial ligno-cellulosic ethanol units worldwide, including five in the United States, two in Brazil and in China, and one in Europe and in Canada. The ligno-cellulosic ethanol supply is rapidly being deployed for industrial use. France is well-positioned in the market, with technology developed as part of the Futurol™ project. Driven by Axens, this technology became commercially available in 2017.

Ligno-cellulosic processes for biodiesel and biokerosene production (primarily the BTL3 process) should emerge by 2020. The French BioTfueL® project demonstrating the BTL process is in its test phase, and several industrial projects have been announced in Scandinavia, Canada and China.

Among the prospects for development of biofuel processes, those which concern the aeronautics sector are among the most promising, given the lack of alternatives to the use of fossil-based kerosene, other than that offered by biofuels. Reliance on low-emission fuel alternatives thus seems unavoidable if global greenhouse gas emission targets are to be achieved in this sector. At present, several products have already been certified for blending at 10% to 50% into fossil-based kerosene (particularly biokerosenes made from hydrogenated fatty acids or created using the BTL process).

In both the road and air sector, the emergence of new processes requires support from public authorities through financial incentives. A clearer vision of future regulatory constraints on biofuel blending is also needed, especially in Europe.

Because liquid fuels used in road transport have strong prospects for future growth in developing countries, demand for biofuels should logically rise. This finding differs for Organisation for Economic Cooperation and Development (OECD) member countries, particularly for the main consuming countries where growth of supply will depend on regulations to promote increased blending of very low greenhouse gas emitting fuels. Clear and stable policies to promote new investment are needed.

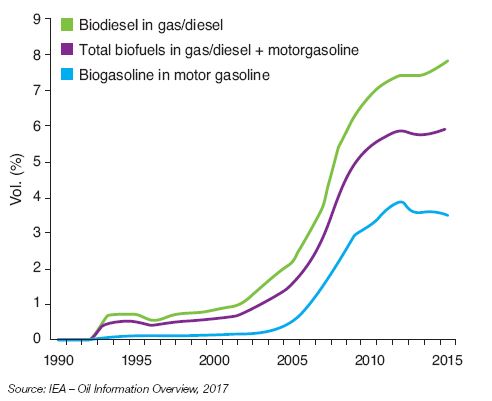

At present in Europe, so long as the proposed REDII directive is not balanced, these conditions are not yet met. Figure 5 highlights the consequences of shifting policies, especially in Europe after 2010.

Strong environmental pressures weigh on the air and maritime transport sectors, given the outlook for rising energy demand. Greenhouse gas reduction goals in aviation could trigger higher global demand for biofuel, which could reach 3 Mb/day in 2040 according to the International Energy Agency.

Regarding advanced biofuels, and especially for developing technologies, lower equipment and operating costs are still anticipated in the short to medium term. This will make the new biofuel processes competitive and, all the easier, oil prices will remain steady and substantial CO2 taxation will be implemented. Against this background, the place for these new biofuel processes in the energy market will be facilitated in the future, so long as uncertainties are eliminated regarding future regulations (post-2020) and related tax policies that promote blending in the various transport sectors.

While the use of biofuels is beneficial with regard to CO2 emissions, current blending rates (less than or equal to 10% vol.) are still not enough to significantly reduce local pollution issues (particulates, NOx, etc.). Technical advancements in combustion engines (improvements in combustion, reduction of polluting emissions at the source) must be pursued, along with post-treatment systems (improved conversion of pollutants into inert compounds, especially at low temperature).

Electricity in transport: evolution or revolution?

Electric vehicles (EV) are seen as an alternative to combustion vehicles that can reduce both the climate impact (so long as electricity production generates little carbon) and the local environmental impact of transport, especially in urban areas.

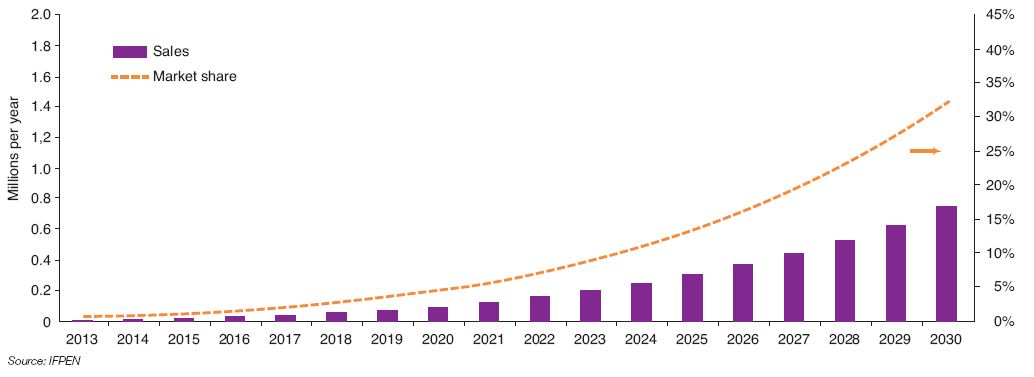

The light electric vehicle market, including EVs and rechargeable hybrids (PHEV) has grown significantly since the first models became publicly available. In 2011, only 50,000 electric vehicles had been sold worldwide; this figure rose twenty-fold within six years to reach 1,230,000 sales in 2017. Market share in 2017 reached 1.3% (Fig. 6). Looking at the current global automobile fleet, it is estimated that 3.1 million electric vehicles were in circulation at the end of 2017 (approximately 0.33% of the fleet).

and share of total sales

In most cases, autonomy of electric vehicles on the market is sufficient to handle day-to-day travel. Looking at the three most widely sold models in Europe during 20164, autonomy (in the certification cycle) averaged 250 km, whereas a typical vehicle does not travel more than 50 km per day. However, autonomy continues to be seen as a barrier to the consumer’s decision to purchase, along with a relatively high sales price (less purchase rebates).

Technological progress is real, targeting improvements in batteries and vehicle weight reduction. The price of batteries has fallen fourfold since 2008, reaching approximately $230/kWh in 2017 according to the U.S. Department of Energy (DOE). At the same time, significant progress on the energy density of batteries has been achieved: currently equivalent to 170 Wh/kg, it should significantly increase (and ultimately reach 300 Wh/kg) due to the emergence of new battery technologies, such as the use of Lithium-air batteries. This parameter is crucial for the move toward lighter, more compact batteries. In addition, recharging infrastructure is expanding in many countries. France should have 45,000 recharging stations (slow) by 2020, compared with 16,000 currently. The growing use of battery vehicles will also demand a greater number of rapid recharging stations to partly relieve wait times — there are only 53 superchargers for 390 Tesla recharging stations in France as of May 20175. At present, in the best case scenario (temperature, supercharger capacity, battery condition), recharging will take between 15 and 30 minutes. The model of swapping an empty battery for a charged battery has proved its limitations.

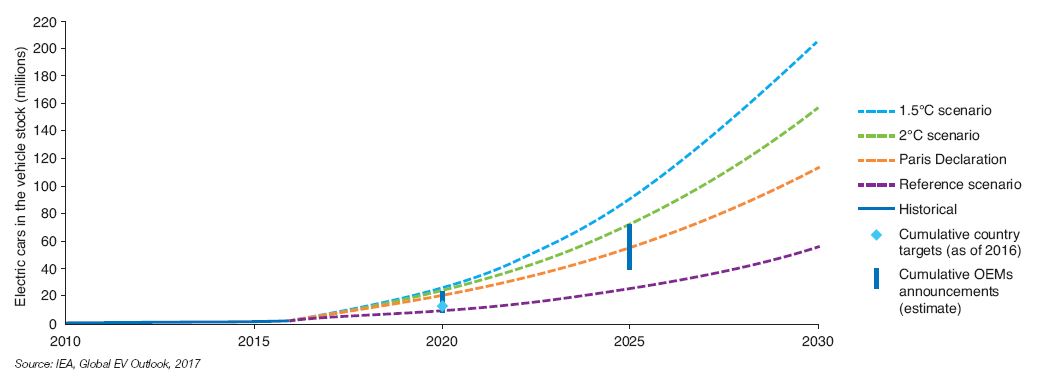

A drastic reduction in sales price, which is currently too high, the need to establish incentive-based public policies to increase market share and greater autonomy are the three key challenges to surmount so that EVs become a sustainable and substantial alternative to combustion vehicles in the global automobile fleet. Although significant technological progress has been noted, improved growth in EV sales has not yet been achieved in the short term. The various deployment scenarios (Fig. 7) show that the number of electric vehicles will only become significant (i.e. > 50 million, 5% of the current fleet) in 20256. It is estimated that by 2040, with moderate growth predicted for EVs, an equivalent of 5 Mb/day of oil will be replaced by electric consumption.

The market is more mature in France. In its most optimistic scenario, an IFPEN analysis based on modelling of the French automobile fleet in 2030 predicts a market share slightly above 30% in 2030, i.e. 750,000 models (EV or PHEV) sold (Fig. 8).

Power-to-gas sector

Hydrogen: an option for the future

Hydrogen produced from renewable electricity (through electrolysis of water) could represent a future carbon-free fuel. Even if electrolysis currently constitutes just 1% of worldwide hydrogen production (particularly when higher purity levels are needed), this process could develop and support the growth of the hydrogen vehicle fleet.

These vehicles operate with a fuel cell that powers an electric motor. As with battery vehicles, they offer the benefit of zero greenhouse gas emissions from their exhaust, apart from water. Contrary to battery electric vehicles, 100% hydrogen vehicles can be quickly recharged (between 3 and 5 minutes), simply through pressure equalization between the recharging station and the vehicle, and offers autonomy (500 to 600 kilometres) close to that achieved by combustion vehicles. Of course, the price of hydrogen remains too high for the driver – it is approximately €10/kg at the pump (an energy equivalence of €3/l of diesel). The price of vehicles, due to the additional costs of the fuel cell, is still too high, with the Toyota Mirai priced at €65,750 as one example. But both aspects – the price of hydrogen and the vehicle price – should fall as electromobility becomes more widespread:

- The production cost of hydrogen by electrolysis between €4 and 6/kg (source: IFPEN) could decline with improvements in electrolyzer performance, which would automatically lower the price at the pump.

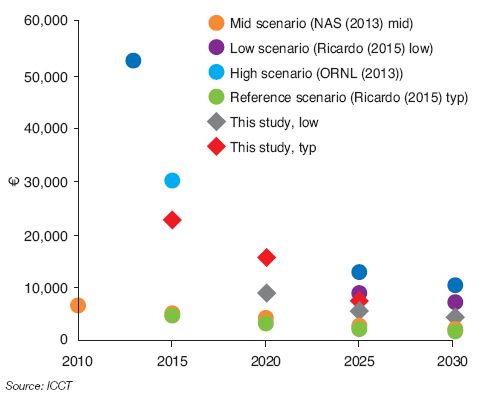

- The very low current production of hydrogen vehicles (3,000 Mirai in 2017) does not yet enable costs to fall through economies of scale. Nevertheless, a significant drop in sale prices can be expected with technology advances and deployment of the system. For example, Toyota announced plans to halve the price of the Mirai by 2025. According to a report by the International Council on Clean Transportation (ICCT)7, the cost of a hydrogen vehicle could fall by 70% between 2015 and 2030 and sales volume could reach 100,000 vehicles by 2030. The additional cost compared with a combustion vehicle would then be equivalent to a PHEV (Fig. 9).

The proliferation of hydrogen recharging stations will also be key to this technology’s success. At present, in France there are only 19 recharging stations (half of which are private), with a goal of reaching 25 stations by 2020. More are undoubtedly needed to boost hydrogen vehicle sales. In addition, regulatory questions about the location of such stations could slow their development. The Mobilité Hydrogène France8 consortium is working on the deployment plan for this system and answers questions from the various players (public authorities, urban areas, etc.).

Despite real potential for reducing local pollution and greenhouse gas emissions (in the case of a very low-carbon hydrogen), hydrogen vehicles are currently just an option over the long term. For example, Toyota (the leading car manufacturer in this technology) sets measured sales objectives of around 30,000 hydrogen vehicles by 2020. In addition, like the carbon content of electricity consumed by EVs, the climate impact of hydrogen vehicles will only be effective if hydrogen production is carbon free, mainly by using electricity of renewable origin (Power-to-Gas process).

Countries wishing to promote EVs as well as hydrogen vehicles will ultimately aim for a massive increase in the share of renewable energy used in their electricity production.

From the various scenarios for development of the automobile fleet, one may envision, on average, that PAC H2 vehicles could represent 3% of the automobile fleet by 2040 (i.e. 50 million vehicles). This would replace 0.5 Mb/day in oil consumption.

E-fuels: the new El Dorado?

Synthetic fuels from electricity of renewable origin, known as e-fuels, have emerged as an alternative to petroleum fuels. They include methane, petrol and synthetic diesel.

Their advantage is the ease of transport and storage, especially for liquid fuels in ambient conditions. In the near future, e-fuels could also address two fundamental criteria: environmental impact and supply security.

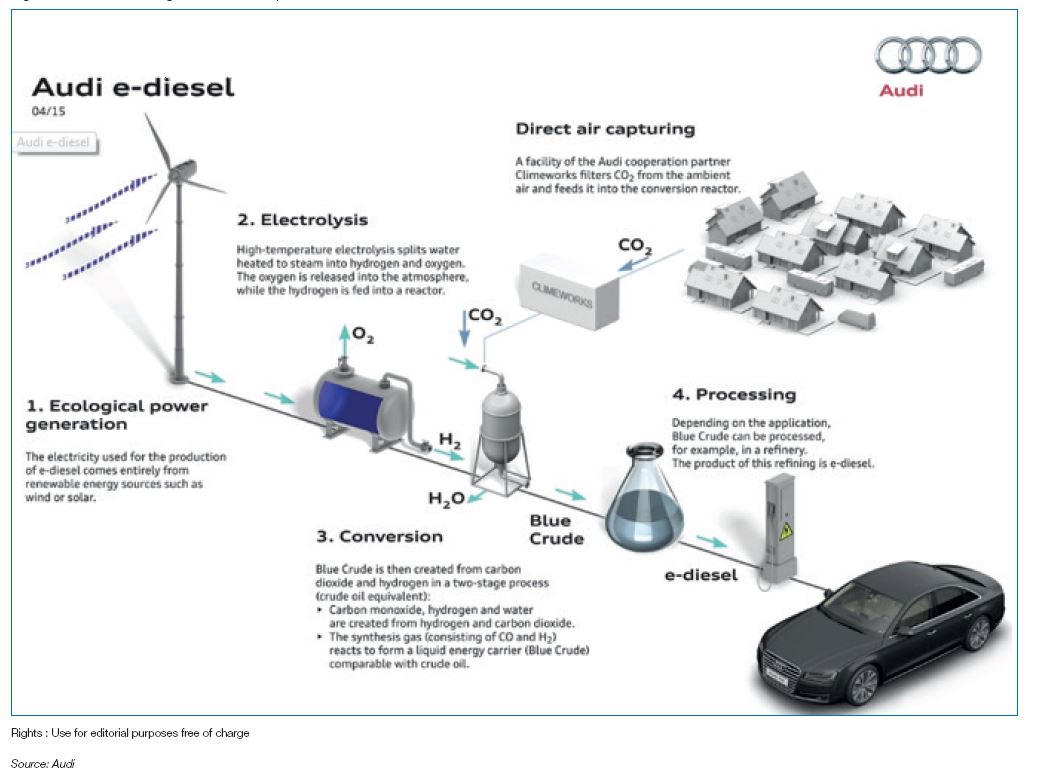

This solution involves redirecting hydrogen to a conversion unit where, mixed with CO2 (especially when captured in industrial units), it will be converted to synthetic methane (Power-to-Methane process) then, if necessary, into synthetic liquid fuel (Power-to-Liquid, see Fig. 9). This last fuel can be directly added to a pool of equivalent petroleum fuel (petrol or diesel) with no need to modify existing engines or the distribution network.

The key points of this solution remain the production of renewable electricity, and the cost of electrolysis, methanation, liquid synthesis and CO2 capture. According to a study by the equipment supplier Bosch9, the cost of a synthetic fuel (petrol or diesel) for direct use in the automobile fleet could optimistically fall between €2 and 2.50/l. To enable large-scale production, the development of electrolysis and CO2 capture technology must advance further, and the externalities associated with such production remain to be quantified. Pilot facilities are already operating in Germany, where medium scale production may be achieved in 10 to 15 years.

However, it is advisable to temper the optimism of various equipment suppliers and manufacturers that wish to make e-fuels the showcase of their R&D. The main barrier to development of e-fuels is likely the cost, especially of CO2 capture, which is more difficult to recover in low concentrations and more costly in units of limited size. Production of “green” hydrogen through electrolysis is also costly, and raises questions about its intermittent nature and competition with resale prices of electricity on the grid.

It is very difficult to identify a growth scenario for e-fuels, given the technology’s lack of maturity. However, for illustrative purposes, a 10% blend rate for these synthetic fuels in the fossil fuel pool in 2040 would lead to a 2 Mb/day drop in oil consumption.

Finally, like biofuels, the use of e-fuels may be beneficial in terms of CO2 emissions, but does not address local pollution issues (particulates, NOx, etc.). To achieve this, technical advancements in combustion engines (improvements in combustion, reduction of polluting emissions at the source) must again be pursued, as with post-treatment systems (improved conversion of pollutants into inert compounds, especially at low temperature).

Conclusion

In response to growing environmental concerns, the transport sector, particularly light-duty vehicles, is undergoing a profound transformation. It is driven by technological progress, groundbreaking innovations, which drive the emergence of new fuel solutions and engines.

To satisfy the Paris Climate Accord and to limit urban pollution from transport, actions taken must be in keeping with two directions:

- at this time, commit the transport sector to low-carbon technological solutions and,

- at the same time, continue improving efficiency and after-treatment of vehicles.

In the short term, improving efficiency of combustion engines and after-treatment of exhaust gas are key ways to lower CO2 emissions and improve air quality. The use of mild hybridization (small electric motor coupled with a traditional combustion engine) or blending of conventional biofuels may offer rapid and meaningful gains in an automobile fleet that is primarily made up of internal combustion vehicles. Efforts toward improving efficiency of spark ignition engines (petrol and VNG) is also a promising avenue for improvement in the medium term. At the same time, alternative solutions based on advanced biofuels, hydrogen and electric vehicles can be launched.

The combination of all these technologies will, in the various segments being considered (road, air, maritime and river) promote carbon reduction in the transport sector. Significant investment in R&D is needed to lower the costs of these emerging technologies and to accelerate the deployment of dedicated infrastructure (especially electric recharging stations and hydrogen stations).

Transformation of this sector will require sustained effort over time. An optimistic scenario for the worldwide growth of alternative solutions shows that, by 2040, it is possible to save around 10 Mb/day, i.e. around 20% of current oil consumption in the sector. Even though this is far from negligible, the transport sector as a whole will remain highly dependent on oil in 2040. This 10 Mb/day in savings will reduce the release of CO2 of fossil origin into the atmosphere by at least 4.3 Mt each day.

Cyprien Ternel – cyprien.ternel@ifpen.fr

Daphné Lorne – daphne.lorne@ifpen.fr

Final draft submitted in February 2018

(1) Study I4CE “Climate figures”, 2017

(2) US Energy Information Administration, Petroleum Status Report, 2017

(3) BTL for Biomass to Liquid. There is a set of processes to synthesize liquid fuel from biomass through thermochemical means

(4) Renault Zoé (21,750 models sold), Nissan Leaf (18,800) and BMW i3 (15,000)

(5) As of May 2017, there were 5,000 superchargers and 9,000 Tesla recharging stations worldwide. These figures are expected to double by 2018

(6) Mercedes wants EVs to constitute 25% of its sales by 2025

(7) Electric vehicles: Literature review of technology costs and carbon missions, ICCT - 2016

(8) Consortium brought together by the Association française pour l’hydrogène et les piles à combustible (AFHYPAC)

(9) Roadmap to a de-fossilized powertrain, Technical Congress 2017