30.07.2019

15 minutes of reading

In 2018, spending on oil and gas exploration rose by 20%, while investments in Exploration & Production (E&P) continued to recover (+ 7%). Estimates for discovered resources give volumes of 9 giga-barrels of oil equivalent (Gboe) in 2018 as against 10 Gboe in 2017. In total, 140 discoveries were made globally in 2018, and gas resources accounted for about 40% of the volumes found. Offshore discoveries predominated, with 70% of the new volumes found over the year. Only four discoveries were of unconventional hydrocarbons. They accounted for 7% of the resources discovered in 2018.

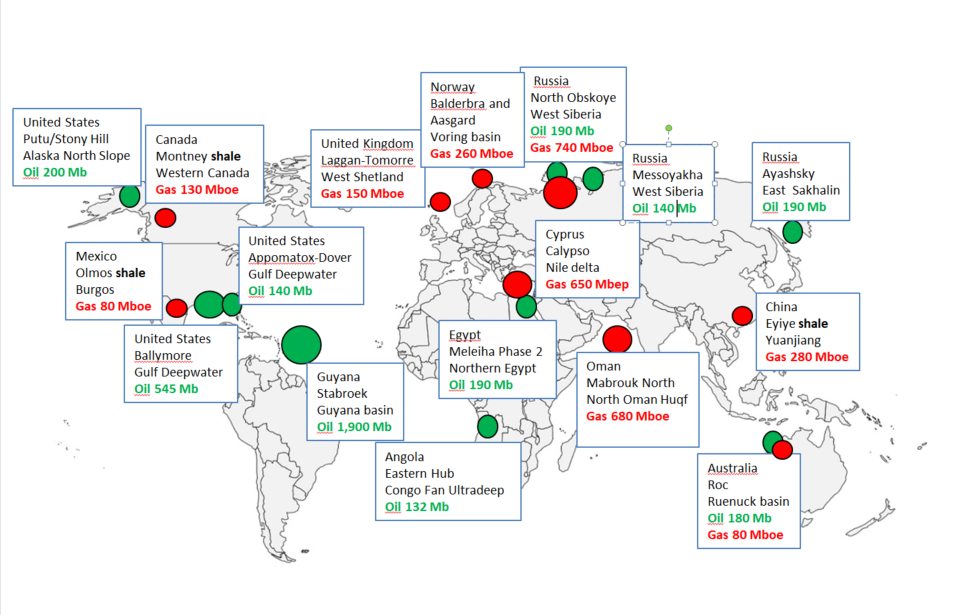

In 2018, the largest oil discoveries were made off the coast of Guyana on the Stabroek block by ExxonMobil, totaling nearly 2 Gb. Over a period of four years, this new oil province has notched up over ten discoveries and about 5 Gb of liquids. The Gulf of Mexico remains prolific, with two oil discoveries, Ballymore and Dover on Appomattox. As regards natural gas, Novatek made the largest discovery of 2018 with the North Obskoye field in the Kara Sea, a giant field estimated at 930 mega-barrels of oil equivalent (Mboe). The gas discoveries off Cyprus with the Calypso field and in Oman with Mabrouk North East represent about 650 Mboe.

2019 is looking set to grow compared with 2018, in particular with discoveries continuing of gas off Cyprus and of oil off Guyana. Globally, a slight recovery in exploration and a rise in discovered volumes appear to be under way.

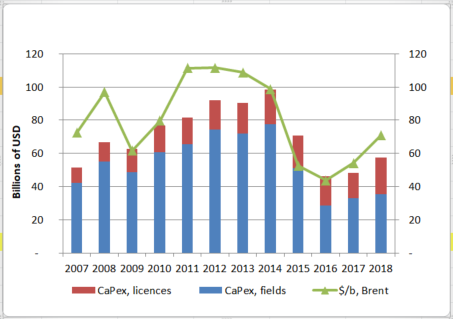

In 2018, global spending on exploration, estimated at $57 billion, was significantly up, by 20%, on the previous year. After peaking at $100 billion in 2014, exploration spending fell sharply by 30% in 2015 and by 35% in 2016, thereby tracking the decline in oil prices (Fig. 1).

The slight increase (4%) in global upstream (exploration and production) investments observed in 2017, with the upturn in oil prices, checked this fall, and was followed by a return to significant growth (20%) in exploration spending in 2018.

The share of the spending that was devoted to investment (capital expenditure, CapEx) in exploring fields is estimated to be 60%, the remainder corresponding to purchases of licenses ($ 22 billion). Over a period of ten years, the financial operations for purchasing licenses has doubled to the detriment of field exploration operations.

Source : IFPEN and Rystad Energy

Volumes of oil and gas discovered

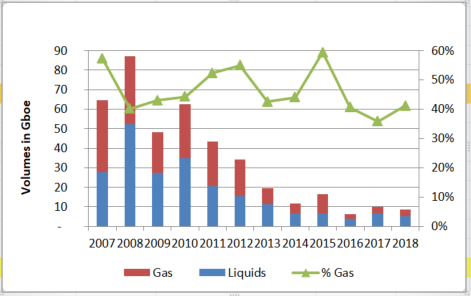

In spite of the upturn in oil prices in 2010, and of the upsurge in exploration spending that lasted until 2014, the volumes discovered declined unceasingly, falling from 62 Gboe in 2010 to 12 Gboe in 2014 (Fig. 2).

With the fall in oil prices in 2015 and the fall in exploration spending, discovered volumes hit a low in 2016 with only 6 Gboe of oil and gas discovered worldwide.

Source : IFPEN and Rystad Energy

Since the low point of 2016, recovery has been slow, despite the upsurge in exploration spending in 2018. In 2018, 140 discoveries were identified, and the initial assessments of the resources give an oil and gas total of nearly 9 Gboe, which breaks down into 5.2 Gb for the liquids and 3.6 Gboe for the gas. However, it can be estimated that the mean unitary size of the discoveries is on the up again because, in 2017, nearly 200 discoveries were made, for a total volume of 10 Gboe.

Of the 140 discoveries, only four were of unconventional hydrocarbons, including two shale gas discoveries in China (Eyiye in the Yuanjiang Basin, and Zhu in the Sichuan Basin) and one in Mexico (Olmos in the Burgos Basin). In total, the unconventional hydrocarbon resources discovered in 2018 are estimated at 600 Mboe, i.e. 7% of all of the resources discovered in 2018.

The share in volume of the gas discoveries has, for the last three years, ranged from 30% to 40%. Ten years ago, the range of that share was more like 60% to 80%. Given the price of natural gas, it is financially more advantageous to produce liquids.

The main discoveries of 2018 by region

In 2018, South America was top region as regards discoveries, with 24% of the global volumes discovered, i.e. 2.1 Gboe, mainly thanks to the major oil discoveries made in Guyana. Three regions then almost tied in terms of discovered volumes, North America thanks to the Gulf of Mexico and Alaska, Europe thanks to Cyprus, and Russia, with each region accounting for about 15% of the global discovered volumes, i.e. 1.3 Gboe.

Then, in 5th and 6th place, came Asia (11%) and the Middle East (9%), with a little less than 1 Gboe. Africa and Australia scored respectively 5% and 3% of the volumes discovered in 2018, but, nonetheless, they had a few major discoveries ranking in the ten largest, for both oil and gas.

Source : IFPEN and Rystad Energy

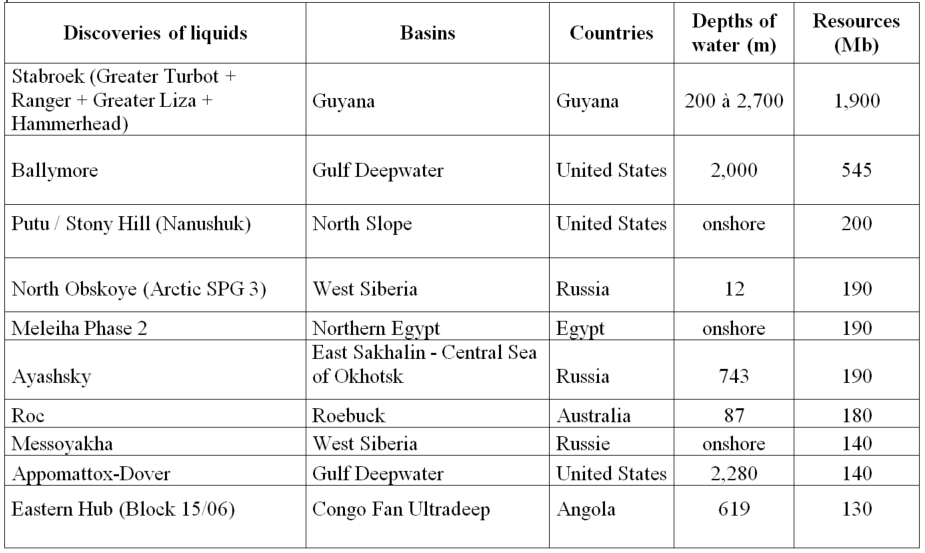

In South America, the series of major offshore oil discoveries on Guyana's Stabroek block continued in 2018. This confirms the existence of a major oil province off the coast of Guyana. With the discovery of Pluma in December 2018, ExxonMobil raised the estimated resources of the Stabroek block to 5 Gboe. It was the 10th discovery on that block in four years. It is recalled that the first nine were Liza, Liza Deep, Payara, Snoek, Turbot, Ranger, Pacora, Longtail, and Hammerhead. By 2025, ExxonMobil foresees an output of 750,000 barrels per day and at least five Floating Production, Storage and Offloading (FPSO) vessels. ExxonMobil, the operator, holds 45% of the interests, alongside Hess (30%) and CNOOC Nexen (25%).

In 2018, Brazil had only one major discovery, of oil and gas combined (130 Mboe), made by Equinor offshore in the Carcara Norte field, in the subsalt layer of the Santos basin. However, Brazil is about to return to a high level of exploration activity, since all four blocks in the 5th round of bidding for subsalt deepwater exploration and production in the Santos and Campos basins have been successfully awarded. According to Brazil's National Petroleum Agency (ANP), drilling through thick salt domes is not without its technical difficulties, but the success rate is high and the resources are substantial, which has aroused the interest of the operators.

Colombia has recorded about ten small discoveries onshore in the Llanos and Magdalena Basins, totaling 80 Mb of oil and 10 Mboe of gas.

In North America, the United States has had three major oil discoveries, including two in the Gulf of Mexico, at Ballymore (545 Mb) at a depth of 2,000 m under water, and at Appomattox (140 Mb) under 2,300 m of water. The United States has also had an onshore discovery in Alaska in the Putu/Stony field (200 Mb).

Chevron is the operator of Ballymore with a 60% shareholding, and with its partner Total holding 40%. At the end of 2017, Total E&P United States signed an exploration agreement with Chevron in the deepwater offshore area of the Gulf of Mexico. That agreement covered 16 blocks in two plays of the Gulf of Mexico: the Wilcox play in the central part, close to the Anchor discovery, and the Norphlet play in the eastern part, close to the Appomattox discovery. The main Appomattox field was discovered in 2010 (579 Mboe), and then it was supplemented with the discovery of Vicksburg (98 Mboe) in 2013, and then Dover (183 Mboe) in 2018. Dover is the 6th Shell discovery in the region. All of the fields will be tied back to the main field.

Onshore, Conoco Philips discovered the oil field of Putu/Stony in Alaska, (200 Mb) in the Nanushuk formation of the North Slope Basin.

Mexico is continuing to make shale gas discoveries, in particular with the Olmos field (80 Mboe) in the Burgos Basin that borders on the Eagle Ford Basin in the United States. That unconventional discovery is the result of the co-operation between Pemex and Lewis Energy, and production should begin in 2021. Among the discoveries of conventional hydrocarbons, two offshore shallow-water oil fields have been discovered in Mexico in the Sureste Basin, namely Mulach (80 Mb) and Ixtal-Manik (44 Mb).

In Canada, in the Western Canada Basin, a new gas resource estimated at 128 Mboe was discovered onshore in the Montney field. It mainly comprises tight gas, but the Montney formation is also known for its shale gas resources that have been producing gas since 2011. This deposit, straddling the border between Alberta and British Colombia, is very large and heterogeneous.

In Europe, the main discoveries were of gas, offshore, and located in the Eastern Mediterranean. The largest is Calypso off the coast of Cyprus (650 Mboe), a deepwater offshore find (2,074 m). ENI and Total are the operators, with a 50% shareholding each. In 2011, Cyprus discovered the gas field Aphrodite, not far from the Leviathan field off the coast of Israel. The multiple discoveries in the Eastern Mediterranean are re-sparking the tensions at the borders of the Exclusive Economic Zones (EEZs) of the various countries. Nevertheless, a new gas hub should develop given the substantial gas resources of the region and the development of the Zohr field in Egypt.

In Norway, the two largest discoveries are the gas fields of Baldera (136 Mboe) and Aasgard (113 Mboe), both of which are located in the Voring basin. Exploring this basin is renowned for being complex due to basalt flows that mask reflection seismic imaging. The chances of major discoveries for Norway probably lie more in the least explored areas of the Barents Sea.

The United Kingdom has discovered 147 Mboe of gas in the Laggan-Tormore field in the West Shetland Basin. That field is scheduled to be connected to a gas processing plant on the coast of the Shetland Islands, 140 kilometers away.

Source : IFPEN and Rystad Energy

In Russia, Novatek made the largest discovery of gas of 2018 with the North Obskoye field, located under a very shallow depth of water in the Kara Sea, 13 kilometers offshore. It is a giant gas and condensates field, estimated at 930 Mboe. In the same basin, Gazprom discovered, onshore, on the Gydan peninsula, the oil field of Messoyakha, whose resources are estimated at 140 Mb of liquids. Among the other oil fields discovered by Gazprom, we might mention Triton in the Okhotsk Sea (200 Mboe), and, onshore, Alexander Zhagrin (130 Mboe) in the West Siberian Basin (Kondinsky district).

In Asia, China has made ten discoveries, seven onshore and three offshore. Among the onshore discoveries, two are of shale gas resources, the largest one, made by Sinopec, relating to the Eyiye field (280 Mboe), and the second, Zhu, found by Petrochina being of much more modest size (20 Mboe). China is determined to achieve energy security and is seeking to develop its unconventional hydrocarbon resources. BP is now the only international company present in exploration and development of shale gas in China. The wells are costly, and they have to reach the lower Silurian at a depth of from 3,500 m to 4,500 m and the productivity of the wells is uncertain. Despite the substantial resources, developing unconventional hydrocarbons constitutes a genuine economic challenge.

Following China's lead, the Indian government has approved exploration and production of unconventional hydrocarbons under the existing oil and gas licenses.

Indonesia has made a series of small discoveries, mainly of gas and located offshore, around Java, for a total of 250 Mboe. The two largest are the Bontang gas field (75 Mboe) operated by Pertamina in the Kutei basin under a depth of water of 50 m, and the gas and condensates field of Ujung Pangkah (71 Mboe), operated by Saka Energi under less than 25 m of water in the Java Sea.

In the Middle East, the Sultanate of Oman is continuing to accumulate gas reserves. The onshore Mabrouk North field was the 2nd largest discovery of gas in the world in 2018, with 790 Mboe, including 110 Mb of liquids, the operator being Shell. By 2023, given the declining output from its mature oil fields, the Sultanate of Oman will be producing more gas than oil.

Bahrain has announced it has made the largest oil discovery in its history with the field of Khaleej Al Bahrain, provisionally estimated at 80 Mboe. That field apparently also includes major gas resources deep down.

In all, the Middle East has had three discoveries in 2018, the smallest being in Iraq, with the onshore discovery of the Salman oil field, which is estimated at 29 Mb.

In Africa, the discoveries are essentially of liquids: oils and condensates.

- Onshore, Egypt has discovered 189 Mb of oil in the Western Desert, constituting Phase 2 of Meleiha. This discovery of oil is one of the ten largest in 2018. The operator Agiba Petroleum is planning to start production in 2021. Among the smaller discoveries made in Egypt, we might mention the discovery of gas and condensates by the British company SDX Energy in the Ibn Yunus field, in the Nile Delta, and the one by the Italian operator ENI in Faramid South in the Western Desert. Agiba Petroleum also discovered oil in Gazalat South.

- In Angola, ENI made two light oil discoveries offshore, with the fields of Kalimba (70 Mb) and Afoxé (60 Mb), under 600 m and 800 m of water respectively. The 15/06 block, initially estimated as a gas-producing area, apparently contains liquid resources that are probably considerable, located in the ultra-deep sea fan located to seaward of the Congo River.

- In Niger, the independent British company Savannah Petroleum made a 4th discovery in the Agadem Rift Basin, with the Bushiya field (70 Mboe). With the discovery of Kafra, Sipex, a subsidiary of Sonatrach is considering the possibility of the existence of a new oil province on the border between Algeria and Niger.

- In Nigeria, Erin Energy discovered the Oyo field (28 Mboe) in the Niger Delta Basin.

Source : IFPEN and Rystad Energy

In Australia, the independent Australian company Santos discovered the Roc onshore oil field in the Roebuck Basin, and this discovery is estimated at 182 Mb of liquids and 83 Mboe of gas. Senex Energy and Santos have also made a series of small oil and gas discoveries in southern Australia, in the Eromanga basin. To cope with the ban on hydraulic fracking in the provinces of Victoria and Northern Territory, the Australian government has launched, in particular for the other provinces, a major gas exploration investment plan. The aim is to counter the rise of LNG in Qatar.

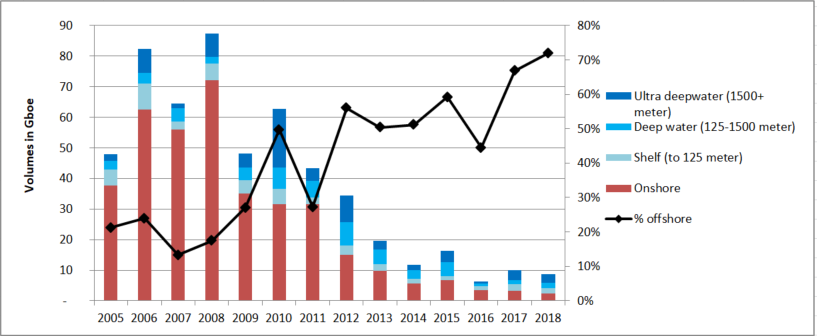

Significance of offshore in volumes discovered

Since 2010, more than half of the volumes discovered have been offshore. In 2018, 55 discoveries were made offshore, representing 70% of the volumes of liquids and gas discovered (Fig. 4). Ultra-deep offshore, with 13 fields discovered in 2018, represents 3 Gboe, i.e. 34% of the volumes discovered, or one half of the volumes offshore. The remainder of the offshore discoveries were found under from 125 m to 1,500 m of water; no discovery was made in 2018 at depths shallower than 125 m, since that maritime domain has already been explored.

Source : IFPEN and Rystad Energy

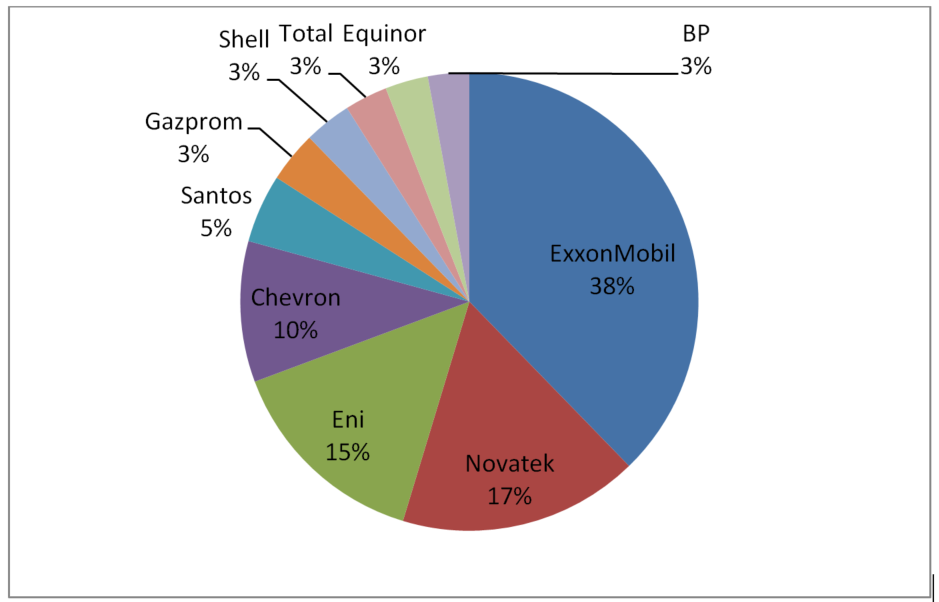

In 2018, the ultra-deepwater offshore discoveries were located in the Gulf of Mexico, Guyana, Brazil, Trinidad and Tobago, Malaysia, Gabon, and Cyprus. Three of the largest discoveries made in 2018 are ultra-deepwater offshore finds: Stabroek under 2,700 m of water off the coast of Guyana, Appomattox-Dover under 2,280 m of water in the Gulf of Mexico, and Calypso under 2,074 m of water off Cyprus. The leaders in the rankings of the offshore operators (Fig. 5) are ExxonMobil, Novatek, Eni and Chevron.

Deepwater offshore offers the possibility of discovering new provinces. Despite the major investments that need to be made (drilling and project-development costs), the scale of the discoveries and the productivity of the wells make it possible to generate substantial profits that mainly benefit the major companies and a few independent companies who take the exploration risks.

Certain major national companies like Petrobras and Statoil, who enjoy considerable maritime resources, have developed the technologies needed for production in very deep water under difficult conditions (HP/HT).

Source : IFPEN and Rystad Energy

Conclusion

The volume of discoveries, which had been stagnating at a little less than 10 Gboe for two years, appears to be increasing slightly with the upturn in exploration budgets. This trend has been confirmed by the volume of new discoveries in the first quarter of 2019, that volume being approximately 3 Gboe of liquids and gas. If it continues at this rate, 2019 could see 12 Gboe discovered over the whole year.

ExxonMobil is continuing its run of successes off Cyprus, with the gas field of Glaucus, which is the 3rd offshore discovery for Cyprus. Similarly, off the coast of Guyana, ExxonMobil has notched up an 11th successive discovery of oil on the Stabroek block, with the Tilapia field, and a 12th discovery of gas and condensates on Haimara. In South Africa, Total has discovered the gas and condensates field of Brulpadda, leading to the discovery of a new oil province that could, in the future, be found to contain new deposits.

The share of unconventional hydrocarbon discoveries remains small but should increase, in particular in India and China. Going from discovery to economically viable production remains, however, a challenge.

Very deepwater offshore exploration, at water depths beyond 1500 m, is playing a leading role. It has made it possible to discover giant fields and new oil and gas provinces such as Guyana and the Eastern Mediterranean.

Sylvain Serbutoviez – Sylvain.Serbutoviez@ifpen.fr

Draft submitted in July 2019