01.01.2018

30 minutes of reading

Sulfur oxides emissions from maritime traffic are constantly rising, unlike those generated by all land-based sources, which are subject to numerous regulations on both fuels and emission caps on equipment that uses them. Accordingly, the International Maritime Organization (IMO) adopted a resolution to reduce the sulfur content of marine fuels, but its implementation, set for 2020, could prove complicated.

The increasingly widespread use of very low-sulfur marine fuels

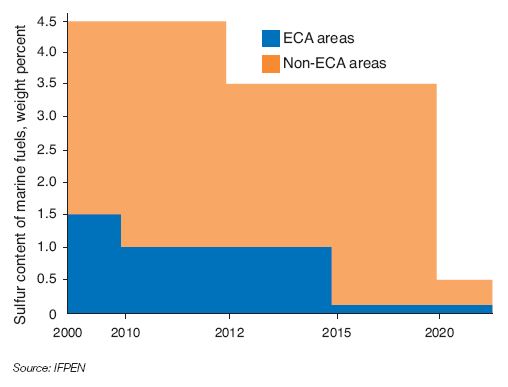

In 2016, maritime transport consumed 235 Mt of fuel, i.e. a little more than 5% of global oil demand. Burning of marine fuels (often referred to as marine bunkers) with high sulfur content leads to acid deposition and contributes to air pollution (sulfur oxides emission), which is harmful to human health and the environment. To reduce pollution caused by shipping, the IMO, a United Nations specialized agency that handles security and safety within the industry and prevents pollution by vessels, adopted a resolution to amend the international “Marine Pollution” convention of 1973 (known as “Marpol”). Ratified by 87 countries, it applies to all ships, including merchant ships which represent more than 80% (in volume) of global trade. A resolution was adopted in 2008 to amend its Appendix VI, which concerns atmospheric pollution and the sulfur content of marine fuels. As of January 1, 2015, this amendment prescribes the use of fuels with maximum sulfur content of 0.1 weight percent (instead of 1%) in emission control areas (referred to below as ECAs), (Fig. 1).

Outside of ECAs, the 2008 version of Appendix VI provided for a shift to sulfur content of marine fuels with a maximum at 0.5 weight percent by 2020 or by 2025 (versus 3.5%, that is to say an 85% reduction) based on the availability of adequate fuels. It was only in October 2016 that 2020 was established as the target year (Fig. 2). This decision ended a long period of uncertainty regarding the convention’s application date, which left the various economic players just four years to achieve compliance.

| One of the consequences of the 0.1% sulfur cap in ECAs The 2015 tightening of sulfur specifications for marine fuels within ECAs led to the appearance of new marine fuel grades, generally lighter than those previously used in these areas. Some of them combine the physico-chemical features of gas oil base stocks (referred to below as distillates) and residual base stocks combining viscosity and a higher flash point than gas oil (easier and more reliable handling), minimization of impurities and excellent lubricity. |

It is difficult to envision full compliance by 2020

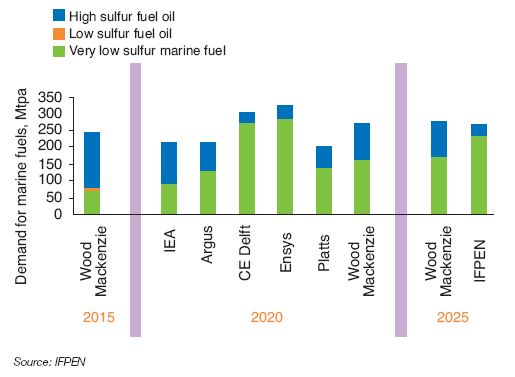

The simplest solution available to ship owners is clearly to use very low-sulfur (VLS) marine fuels. This choice, which does not involve any investment on their part contrary to other available possibilities, assumes a market in marine fuel with a 0.5% sulfur content supplied by refiners. However, it seems likely that as the 2020 deadline approaches, the refiners that supply this market (estimated between 100 and 300 Mt) will be temporarily unable to satisfy all demand solely through VLS residual base stocks. Some refineries’ configurations mean that they will be unable to produce sufficient quantities without investing in additional desulfurization or conversion of residues with high-sulfur content capacity. Because of the very low number of investment projects announced for these types of processes (expressed in $billions per unit) and their build times (2 to 5 years), there are likely to be shortages in residues that can be incorporated into VLS marine fuels by 2020. In other words, there are fears of a temporary supply/demand imbalance in marine fuels with 0.5% sulfur content (for an undetermined period) when future IMO requirements take effect, despite the inconsistency among the demand forecasts available in the literature (Fig. 3).

There are two possibilities to consider with regard to the likely shortfall in VLS residual base stocks:

- non-compliance of some marine fuels which is harmful to the environment (potentially massive since the most pessimistic entities are forecasting around 100 Mt of such out-of-specification fuels),

- additional use of distillates. Their large-scale incorporation (direct or mixed) into marine fuels with 0.5% sulfur content, like those used in ECAs, is nevertheless problematic since refiners only produce them if the sale of such fuels is profitable. However, production capacity for these distillates is currently insufficient to meet demand in the sector, and the 2020 deadline is too close for timely construction of the dditional capacity required. The supply/demand imbalance will mean higher prices for marine fuels, which will be profitable for refiners that have units dedicated to their production, but will damage the competitiveness of shipping. At the same time, the high sulfur fuel oil (HSFO) market could reach structural overcapacity, which would decisively disrupt global refining. There is no doubt it will continue to be used by stationary facilities with flue gas desulfurization systems and by ships equipped with scrubbers, but the risk of surpluses is real. On the other hand, such excess would benefit ship owners, which will choose scrubbing of HSFO due to low values in an overcapacity market.

What are alternative solutions to marine fuel with 0.5% sulfur content?

The main alternatives to using VLS marine fuels are the use of alternative fuels (liquefied natural gas, biomass and non-biomass synthetic fuels) and the installation of scrubbers. The relative share for all of these options, with distinct performances, currently remains uncertain.

The use of liquified natural gas (LNG) as a marine fuel has the advantage of zero sulfur oxides emissions along with an attractive price. Despite this, its market share will not be predominant over the short term, since substantial investment is needed (not only by ship owners, but also by certain port authorities) due to a lack of available infrastructure. The makeup of the maritime fleet demonstrates this: fewer than 200 ships (out of around 100,000) are currently powered by LNG. Even if this number on shipbuilders’ order books nearly doubles, some specialists believe that consumption of only 5 to 15 Mt of marine fuel with 0.5% sulfur content would be avoided in this way by 2020.

IMO regulations allow ship owners to continue burning HSFO if they invest in a scrubber1. Estimates vary regarding of the penetration rate for this technology, which is currently used in fewer than 1% of ships worldwide.

However, some players in the oil industry agree that installation of scrubbers would deduct around 35 Mt of marine fuel with 0.5% sulfur content by 2020. Regardless, with scrubber manufacturers’ limited capacity2, this solution only impacts a limited portion of the fleet. Contrary to scrubbing of flue gases at stationary facilities, which has been done for more than 30 years, on-board technologies are in the early stage of commercial use. The most widely used technology operates using wet method.

It involves washing flue gases with an alkaline aqueous solution. These processes can be open-loop (the solution is nothing but naturally basic sea water), closed-loop (a basic reagent such as sodium hydroxide or milk of lime is incorporated into soft water, which is pumped from a reservoir then recycled after cleaning) or a hybrid process.

Sulfur oxides captured during scrubbing end up as sulfate in flue gas neutralization sludge (which contain hydrocarbons, ashes and heavy metals). Like hazardous waste, this sludge must be stored on-board before being discharged at ports (provided the ports have reception facilities). Thus, controlling the proper application of this technology is key to avoiding any discharge of pollutants into the ecosystem. That said, the issue of compliance is also critical with respect to the specific sulfur content of VLS marine fuels. The implementation of regulatory measures to check compliance with provisions was thefocus of discussions at the most recent meeting of the IMO’s Marine Environment Protection Committee in July3.

One of the few certainties regarding the use of alternative solutions is the fact that they are largely used on new ships, given their dissuasive cost and the technical impossibility (dimensions) of renovating existing ships. They will be more favorable on larger vessels that travel long distances. Their profitability (from the ship owner’s viewpoint) will be proportional to the price differential between VLS marine fuel and HSFO and, to a lesser extent, to time spent in ECAs.

In summary, contingencies, clashing prerogatives between refiners and ship owners plus a degree of perplexity regarding possible legislative changes are factors that slow decision-making, less than three years before the future IMO requirements take effect.

What are solutions for producing marine fuel with 0.5% sulfur content in a refinery?

Global refining will probably be unable to meet demand for marine fuel with 0.5% sulfur content once the OMI provisions are implemented. Technical feasibility is not the reason for this shortage, since there are proven technologies that can be adapted for its production.

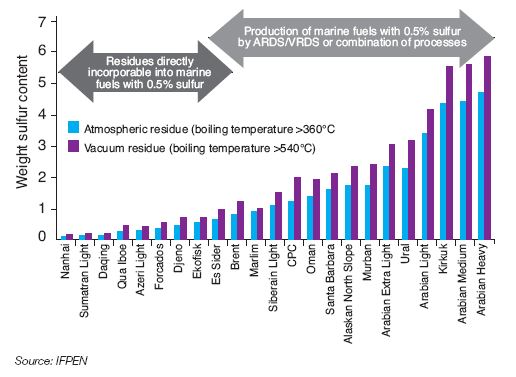

The residual base stocks most suitable for producing marine fuels with 0.5% sulfur content come from the first distillation of VLS oils (atmospheric and vacuum residues). Derived from the initial refining stage, their low production costs makes it economical to incorporate them into non-ECA marine fuels. Nevertheless, availability of VLS oils (generally light and with uneven geographic distribution) is such that refiners only possess them in limited quantities4. Consequently, not everyone can produce all marine fuels with these cuts. Those which intend to supply the marine fuel market and possess these prized VLS oils will likely adjust their supply so that their contribution carries more weight within the refinery crude diet. This practice, which assumes that these VLS oils are separately refined (segregation), will be followed to the extent possible, and so long as the price of these feedstocks (which will inevitably rise) does not hinder their acquisition (Fig. 4).

To address the high sulfur content of residual base stocks other than VLS ones, a proven solution is hydrotreatment or desulfurization in the presence of hydrogen. This solution also applies to atmospheric residue desulfurization (ARDS) and vacuum residue desulfurization (VRDS).

Effluents from these units have lower levels of sulfur compounds as well as nitrogen compounds, metals and asphaltenes. Accordingly, ARDS/VRDS allow direct production of marine fuel with 0.5% sulfur content as well as providing a feed of choice for fluidized-bed catalytic cracking units. Their other advantage is the moderate conversion of residual bases in lighter, more recoverable products (naphtha and diesel). It should be mentioned that the eliminated sulfur is completely recovered and collected in solid form through a chain of fully-controlled high-performance units for use as raw material in other industries (sulfuric acid, fertilizers, etc.).

Another solution involves the further conversion of these residual base stocks through various processes or linked processes. Available technologies generally fall into two categories: those with carbon discard such as delayed coking, and those which add hydrogen through a catalytic intermediary that improves the yields and quality of converted products. These conversion processes have the benefit of flexibility and secure production of marine fuel with 0.5% sulfur content (with coproduction of higher value-added distillates).

- Delayed coking enables the production of coke (20 to 30% by weight) and lighter cracked products such as naphthas, light gas oil and heavy gas oils from coking. The latter can be converted to marine fuel with 0.5% or 0.1% sulfur content after desulfurization.

- Solvent deasphalting enables separation of residual base stocks into deasphalted oil and an asphalt. The deasphalted oil, after desulfurization, meets specifications for 0.5% and even 0.1% sulfur content.

- Fluidized-bed residue hydrocracking achieves higher conversion of residual base stocks into lighter products such as naphthas, gas oils and vacuum distillates. Recent technological advances concerning this process mean that it can be specially designed for very high conversion. It can also be paired with solvent deasphalting or delayed coking to produce deasphalted oil or heavy coker gas oil from hydrocarbons not converted in residue hydrocracking. If the produced naphthas and gas oils can be post-processed then incorporated into fuel for light vehicles or road freight, vacuum distillates and deasphalted oil or heavy coker gas oil may be subsequently converted using suitable processes (distillate hydrocrackers) or be desulfurized for compliance with the 0.5% or 0.1% sulfur content specification.

There is no recommended solution by default. Each decision results from a comprehensive system analysis which considers refinery configuration, changes in product prices, the use of other petroleum bases to formulate VLS marine fuels and the level of investment in processes, post-treatment and utility generation (especially hydrogen production and sulfur recovery chain).

Optimal formulation of marine fuels with 0.5% sulfur content

The choice of the technical solution (scrubbing, use of alternative fuels or VLS marine fuels) raises the question of the production cost of these fuels in a refinery. To address this, IFPEN conducted a technical-economic study on the various refining products by 2025. Based on the results from a linear programming model specified to meet global demand for oil at a lower cost, this work helps to measure the impact of the IMO regulations on global refining.

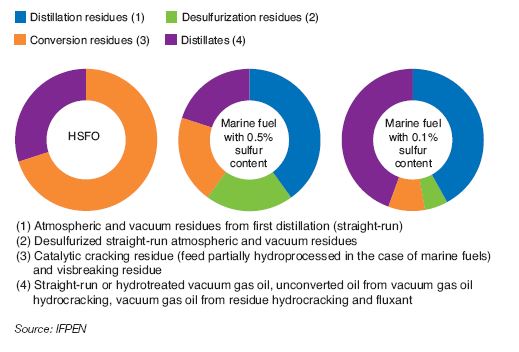

This exercise looks at the marginal values of oil products and the composition of marine fuels in a market having regained equilibrium following the transition period that could result from implementation of the IMO requirements. One of the results (Fig. 5) shows that marine fuels with 0.5% sulfur content (a grade that will make up three-quarters of demand for marine fuels in 2025) could be formulated mainly with residual base stocks. VLS distillation residues are their main components5. This presumes the normalization of VLS oils segregation, which will first be directed to refineries that produce marine fuels with 0.5% sulfur content. Competition for access to these VLS oils could weaken “rival refineries” that use these base stocks for other purposes (for example, feeding a catalytic cracker with non-pretreated residues). This competition leads to greater needs for investment in ARDS/VRDS within the refineries that lack them.

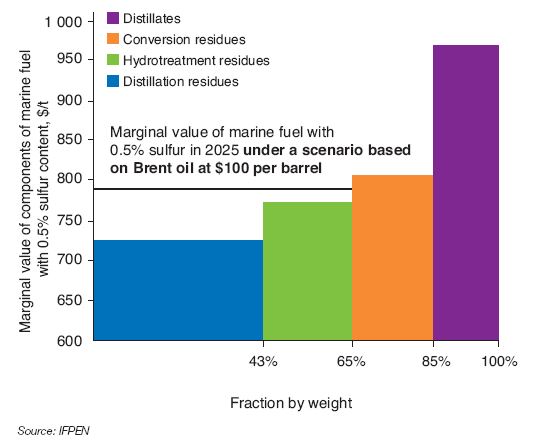

The appeal of the model for the various components of marine fuel with 0.5% sulfur content is presented in figure 6. It shows the interest in less costly residual base stocks (distillation residues first, then desulfurization residues followed by conversion ones6). Incorporation of distillates is more costly (20 to 35% depending on the applicable residual base stock), but necessary to comply with all VLS marine fuel specifications (density, viscosity, etc.).

sulfur content by 2025

In the studied scenario, in which the price of Brent oil was $100/barrel (i.e. $754/t), the cost price of marine fuels with 0.5% of sulfur and HSFO are $788 and $641/t respectively. This $147/t difference is consistent with the $120 to $160 range obtained from other exercises performed in an effort to maximize production marine fuels with 0.5% sulfur.

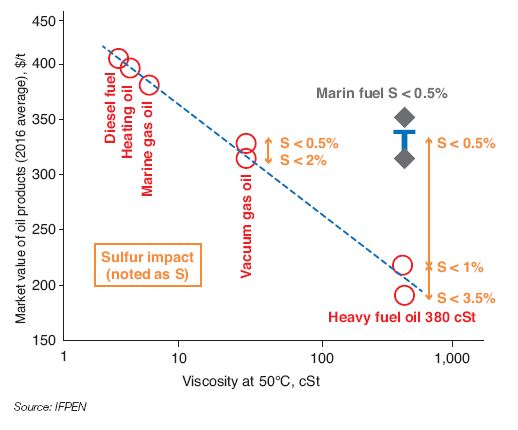

This difference in production cost between HSFO and marine fuel oil with 0.5% sulfur (ideally formulated) underscores the significant impact of future regulations on the price of marine fuels. Figure 7, prepared based on average market values for oil products during 2016 (while the price of Brent oil was $44/barrel) clearly shows this: the long-standing rule, whereby product price is correlated with viscosity (reflecting its residual base stocks content) and is relatively independent of sulfur content, is largely set aside in the case of marine fuel oil with 0.5% sulfur. Still, it is important to remember that such pricing games are plausible in a balanced market. In any case, high volatility in the price of certain oil products is expected, particularly for marine fuels, upon implementation of the coming IMO requirements unless steps are taken to avoid such an event.

content) of oil products in 2016

Marine fuels with 0.5% sulfur content: doubts prevailing

The shift to marine fuel with 0.5% sulfur content by 2020 is filled with uncertainty. Divergent positions concerning their formulations (residual base stocks versus distillates), disparate predictions for penetration of alternative solutions, potential temporary non-compliance of marine fuels and the possibility of flexible requirements have left stakeholders perplexed. However, there is consensus on the fact that the scrubber solution (with the complexity of ensuring their proper use) will be limited, and that the use of LNG is currently restrained by the lack of existing infrastructure. The use of refinery-produced marine fuels with 0.5% sulfur will be thus preferentially adopted, but the industry must make arrangements to minimize investments. Refiners that supply this market will first arrange for the processing of VLS oils, whose distillation residues can be directly incorporated into marine fuels with 0.5% sulfur, and operate their units to maximize their production. But bottlenecks exist and investments in refining processes must be scheduled to meet demand.

The risk of non-compliance with IMO regulations by 2020 is recognized, given the short timeframe between their adoption and the implementation date. Many proven professionals view total compliance with these requirements within this timeframe as a challenge, due to the inadequate deployment of suitable technological solutions. Accordingly, we will see a transition period during which the price of VLS oils and certain oil products (particularly marine fuels) will be disrupted, unless there is more flexibility in the law.

On the other hand, one thing is certain: The IMO has prepared a road map to develop a global strategy for reducing greenhouse gas emissions in shipping in spring 2018, and is aiming for a comprehensive depollution of this transport mode.

Contributors: Pierre Marion – pierre.marion@ifpen.fr ; Valérie Saint Antonin – valerie.saint-antonin@ifpen.fr ; Wilfried Weiss – wilfried.weiss@ifpen.fr

Final draft submitted in January 2018

(1) The use of scrubbers is permitted so long as the permanent reduction of sulfur emissions at least equals reductions achieved through the use of marine fuels that meet IMO requirements

(2) Estimates of the number of ships that can be equipped with scrubbers range from 1,200 to 3,000 per year

(3) 71st session of the Marine Environment Protection Committee or MEPC 71

(4) IFPEN estimates that production of VLS oils will reach slightly more than 10% of worldwide oil production by 2025

(5) Availability of LSFO atmospheric residue is estimated at between 200 and 250 Mt in 2025 (a quantity sufficient to manufacture all marine fuel oils with 0.5% sulfur if they are not reserved for other uses)

(6) Mainly catalytic cracking residue