09.02.2024

15 minutes of reading

Summary:

- Gasoline substitutes

- Diesel substitutes

- Biomethane for NGV powertrains

- Spotlight on biofuels in the aviation sector

- The emerging role of biofuels in maritime transport

- Focus on France

- Outlook for carbon neutrality

- Investment outlook

- A stronger position for biofuels in medium/long-term scenarios

Biofuels in the road transport sector

Biofuels in the road transport sector

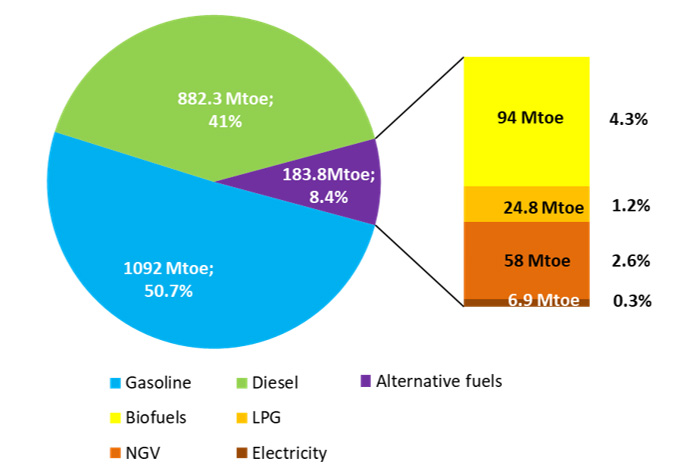

In 2022, global energy consumption in the road transport sector amounted to just over 2.16 Gtoe, representing an increase of 3.4% compared to the previous year. While the health crisis caused annual fuel consumption to fall by more than 10%, it is now back to pre-COVID levels (2.17 Gtoe in 2019).

The share of alternative energies to oil-based gasoline and diesel fuels (biofuels, LPG1, NGV2 and electricity) is up by more than 2.7%. In 2022, it represented 8.4% of the fuels consumed, i.e. nearly 180 Mtoe, the highest level ever reached. Among these alternatives, biofuels accounted for 94 Mtoe, i.e. a market share of almost 51% of these alternatives and 4.3% of all fuels consumed (Fig.1). After plummeting by more than 7% between 2019 and 2020, biofuel consumption bounced back by 3.2% between 2021 and 2022. These consumption levels and market shares are also very similar to the situation observed in 2019 (94.4 Mtoe in 2019).

in the road transport sector in 2022

Source: IFPEN, from Enerdata and S&P Global

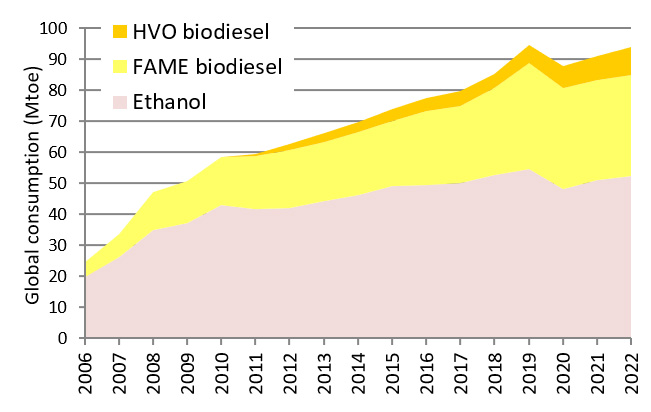

Out of the biofuels available for consumption in 2022, bioethanol, the main substitute for gasoline, continued its post-COVID recovery, with annual growth of 3%, but without returning to its pre-crisis level. The global consumption of ethanol thus reached 52.5 Mtoe in 2022, a level similar to that of 2018. This trend is similar to that of the gasoline market, which incorporates ethanol. As for biofuels that replace diesel, their overall consumption remained relatively unaffected by the crisis and continued to grow, reaching a record level of 41.5 Mtoe worldwide (Fig. 2). This growth was directly proportional to the increase in global demand for diesel engine fuels (around 3.5%). From a technological standpoint, the dynamics of the biodiesel market are mainly driven by the growth in demand for HVO (Hydrotreated Vegetable Oil), estimated at +15% between 2021 and 2022, compared with +0.7% for FAME (Fatty Acid Methyl Ester).

in the road transport sector in Mtoe

Source: IFPEN, from S&P Global

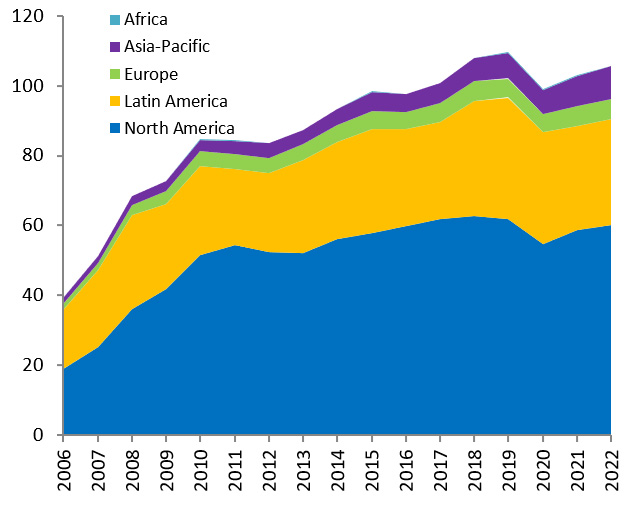

Across the entire continent, the incorporation rates of all biofuels into road fuels have remained stable since 2019. They vary depending on the region, but Latin America still has the highest rate (nearly 10% in energy terms), thanks to the Brazilian ethanol market, which alone reaches an incorporation rate in gasoline of close to 40%. North America and the European continent follow, with respective rates of 7% and 5.7% respectively. In Asia, this rate has been rising every year and reached 2.4% in 2022.

In the European Union, the health crisis has had little impact on biofuel consumption, which has remained virtually stable between 2019 and 2021, at around 17 Mtoe. Throughout 2022, consumption of liquid biofuels on the European continent rebounded by 13% to nearly 19 Mtoe, thanks primarily to growth in the HVO market.

While growth trends are struggling to pick up in South America (+0.4% vs. 2021), they are nonetheless effective in North America (+3.4%) and very marked in Asia (+7.6%).

Gasoline substitutes

Since the emergence of the biofuel market, ethanol has remained the primary substitute to gasoline fuels used around the world. Worldwide, the growth of its consumption has been estimated at +3% between 2021 and 2022. The United States continues to be the biggest producer, followed by Brazil. The two countries alone account for 82% of the global market. However, it was in Asia-Pacific that the rate of growth in production was the highest at over 10%. India, China and Thailand account for 94% vol. of the Asian market, with India showing particularly strong growth in 2022 (+24%).

Source: IFPEN, from S&P Global

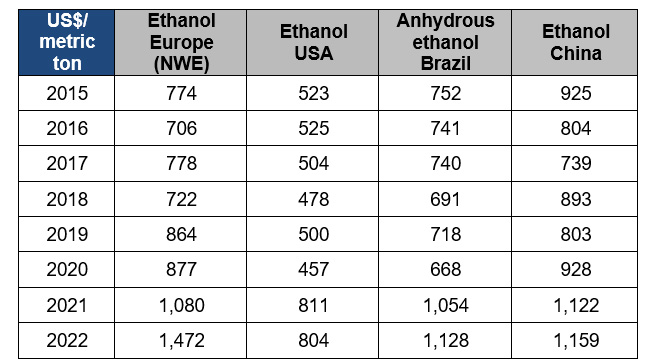

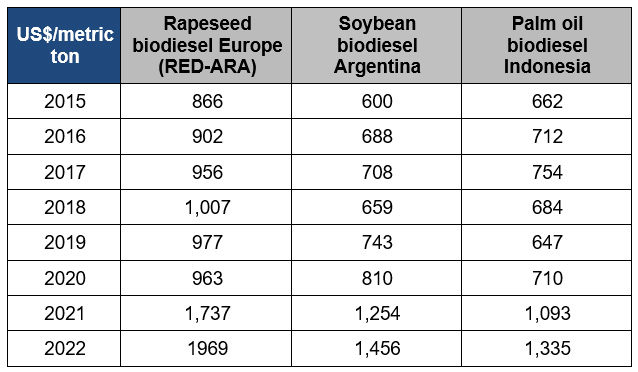

In Europe, demand for fuel ethanol continues to grow, driven primarily by the take-up of SP95-E10 and super-ethanol E85, particularly in France. Despite this, local European production has remained relatively stable since 2019. The uptake of European cereals has not changed (around 10 Mt). The disruption in the raw materials supply chain caused by the war in Ukraine continued into 2022. At the same time, soaring prices for natural gas - the main energy resource for European plants - squeezed production margins in the second half of the year, forcing producers to raise selling prices. Therefore, on the international market, Europe recorded the highest market price for fuel ethanol in 2022 (Table 1). In fact, ethanol imports reached a record level in 2022 in the European Union (+75%), including in the United Kingdom.

Source: IFPEN, from Argus

This has made Brazil the world’s leading exporter of ethanol, in response to rising European demand. Locally, the market is continuing to grow following the health crisis, but has not yet returned to its 2019 level, still suffering from the effects of poor weather in 2021 on sugarcane productivity. However, we can already expect that the 2023-2024 campaign will result in a market situation higher than historical levels.

Diesel substitutes

Two main biofuels are currently incorporated into the road diesel fuel pool: FAME and HVO. They use biomass resources that contain fatty acids mainly derived from oilseed crops (rapeseed, palm, soybean, etc.) or used cooking oils or animal fats. Unlike FAME, the incorporation of which is limited to a maximum of 10% vol. in diesel distributed at the pump in the European Union, there is no limit to the amount of HVO that can be incorporated in the mix. The youngest industry, but one that is enjoying strong growth, HVO represented 22% of biodiesels consumed globally in 2022 (compared with 16% in 2021) (Fig. 2).

Historically, the biodiesel market has dominated in the European Union, where the majority of vehicles run on diesel, unlike in other parts of the world. While the EU remained the world’s biggest biodiesel consumer in 2022, Asia became the world’s biggest biodiesel producer for the first time, producing more than 20 billion liters of biodiesel, over 60% of which is located in Indonesia. Following the EU’s decision to end support for biofuels made from palm oil, and the relocation of the US biofuels market, Asian palm biodiesel producers have reoriented their market. Indonesia has launched an ambitious energy security program targeting 23% renewable energies by 2025, including locally rolling out B35, a diesel fuel made from 35% vol. biodiesel. In China, Asia’s 2nd-largest biodiesel producer, production rose by more than 40% between 2021 and 2022. This production, which is primarily composed of biodiesel derived from waste oils and fats, is almost entirely dedicated to export to the EU. However, suspicions of fraud are currently being investigated, with the EU suspecting that China is dumping volumes of Indonesian palm biodiesel in Chinese biodiesel shipments.

by zone (in billions of liters)

Source: IFPEN, from S&P Global

In the EU, local production remained stable in 2022, while imports of biodiesel and waste oils and fats rose by 14% in 2022. Of the 5.8 Mt of imported products, the vast majority are UCO3 and PFAD4 (around 80%), but there are also volumes of UCO biodiesel and tall oil. When released for consumption in the EU, all of these products can be doubly counted towards the objectives of the REDII Renewable Energy Directive.

In the United States, the incorporation of biodiesel rose by nearly 10% in 2022, mainly due to the expansion of the HVO market, which accounts for nearly half of all incorporated biodiesel in 2022. While market growth in 2021 was mainly driven by imports, domestic HVO production capacity surged in 2022 and 2023, with some fifteen production units now operational. Four more units are currently under construction, and some fifteen additional projects have also been announced.

In Brazil, the biodiesel incorporation mandate was maintained at a lower level (B105) for 2022 in order to bring down the price of soybean oil, which has risen sharply following a poor harvest in 2021. The changeover from a B10 to a B12 mandate took place in 2023, while a B13 mandate is planned for early 2024. This year, the government’s Renovabio program includes a 15% (B15) mandate target for 2026.

In line with rising market demand and persistently high energy prices, biodiesel prices continued to rise throughout 2022.

Source: IFPEN, from Argus

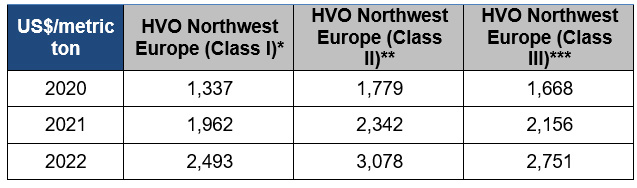

for different resource classes [US$/t]

Source: IFPEN, from Argus

* Class I: from food crops, enabling a reduction in greenhouse gases of 65% min.

**Class II: HVO from recycled vegetable oils (UCO, POME), enabling a reduction in greenhouse gases of 85% min.

***Class III: HVO from category 3 animal fats, enabling a reduction in greenhouse gases of 80% min.

For the FAME and HVO sectors, biodiesel prices followed the inflationary trend in 2022, reaching record levels, particularly for class II HVO in Europe, which benefits from double counting to reach incorporation mandates.

Biomethane for NGV powertrains

An as yet minority renewable fuel, biogas consumption is nevertheless increasing in some zones where natural gas has historically figured among road fuels. Currently primarily produced by the anaerobic digestion of organic waste (methanization), or via the recovery of landfill gas, biogas is a renewable fuel principally used for heat and electricity production. Only a fraction (less than 10%) is purified to obtain biomethane that is suitable for injection into the natural gas network and/or used as a fuel in dedicated vehicle engines (NGVs).

For transport, biomethane can be used in the form of Bio-CNG, a compressed form of biomethane, or Bio-LNG, which is a liquefied form of biomethane. Bio-CNG and bio-LNG can replace conventional CNG and LNG derivatives of natural gas without the need for any changes to infrastructure. Both fuels can be produced either directly in the biomethane production plant (on-site production), or by extracting biomethane from the grid using Guarantees of Origin (GO).

Today, Bio-LNG is mainly used for heavy-duty truck fleets. By the end of 2021, Europe had 15 Bio-GNL production plants in operation (around 1 TWh of capacity), fueling a fleet of around 15,000 trucks. This number should rise sharply in 2022 (+19 plants), 2023 (+43 plants) and 2024 (+21 plants). According to the EBA6, out of the hundred or so known Bio-LNG projects in Europe in 2022, 86% have a physical connection to a biogas purification unit, while 14% of projects purchase biomethane from the gas grid via GO. 10 European countries are currently active in the Bio-LNG market. The two largest bio-LNG plants in Europe are located in Germany (140 GWh/year) and Norway (120 GWh/year). The highest production capacities are expected in Germany, Italy, the Netherlands and Sweden, respectively, by 2025 (a total of almost 10.5 TWh),

Bio-CNG is used on fleets of heavy-duty and lighter vehicles. In 2022, there were 133 biogas plants in Europe producing compressed biomethane on site, including 69 in Sweden alone, 23 in Finland and 14 in Norway. Other producing countries have fewer than 10 production sites.

In the United States, NGV fleets made up of heavy trucks, buses and waste collection vehicles, have grown significantly in recent years. In 2022, Bio-NGV consumption rose by nearly 18%, to reach nearly 2.3 Mtoe. 86% of this Bio-NGV is consumed in the form of Bio-CNG and 13% is consumed as Bio-LNG.

Spotlight on biofuels in the aviation sector

With the growing awareness of the existing environmental impacts of international air travel (which accounts for 13% of CO2 emissions in the transport sector) and given the sector’s growth outlook, member states of the international civil aviation organization (ICAO) adopted a twofold global goal: (i) an immediate goal of stabilizing CO2 emissions from international aviation at 85% of the level observed in 2019, by incorporating sustainable aviation fuels (SAF) or purchasing certified offset credits; (ii) a long-term aspirational goal (LTAG) to reduce emissions to zero by 2050, without using offsets. To date, this target is not binding, but member state governments are responsible for drawing up incentive action plans. To achieve these goals, using SAFs is regarded as one of the principal levers for reducing emissions. There are currently 8 alternative biokerosenes certified to ASTM International standard D7566, including some that are already mature or close to industrial maturity, such as HEFA-SPK7, produced by HVO units, FT-SPK8, products of Fischer-Tropsch-type BtL and e-fuel processes, and ATJ-SPK , produced by converting ethanol or isobutanol into synthetic kerosene. These alternative kerosenes are currently approved for incorporation in conventional kerosene, with a maximum limit of 50% vol. in the blend.

In 2022, 240 kt of SAFs were produced worldwide, and production is expected to double by 2023. This production is primarily located in Singapore, Finland and the United States. Today, this production consists exclusively of HEFA-SPK. In 2022, the USA incorporated 48 kt of SAF, including 15 kt from imports. Through its Sustainable Aviation Fuel Grand Challenge, the US government has set itself the challenge of producing 9 Mt of SAF by 2030, corresponding to 10% of all the kerosene supplied by the country’s airports. Over the same timeframe, in the European Union, the ReFuel EU Aviation initiative requires the incorporation of 6% SAF in the kerosene distributed at European airports, i.e. around 3.5 Mt. By 2050, the European Union should be aiming for a 70% SAF incorporation rate. In Brazil, a SAF incorporation mandate is due to come into force in 2027, with the aim of reducing the sector’s CO2 emissions by 1%, a goal that will progress towards a 10% reduction by 2037. In the Asia-Pacific region, Japan proposed legislation in 2022 requiring SAF to account for 10% of aviation fuel by 2030. Over the same period, the Chinese civil aviation administration has also set itself the goal of increasing the use of SAFs and reducing the intensity of greenhouse gas emissions.

The announcement of these various goals has encouraged producers and airlines to sign a large number of partnership and supply agreements, accounted for around forty in 2022, as well as a major partnership in 2023 between Shell and Rotterdam airport for the production of 820 kt of biokerosene and the incorporation of SAF for all aircraft refueling at the airport from 2024.

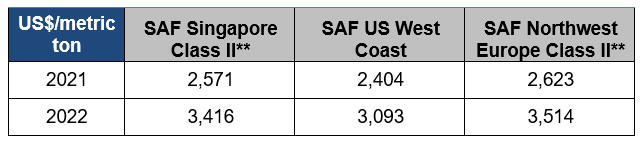

With the emergence of the SAF market, the first HEFA-SPK quotations have been recorded in Singapore, the United States and Europe, around $2500/t in 2021 and above $3000/t in 2022. The annual average should nevertheless fall back below $3,000/t in 2023.

per major production zone [US$/t]

Source: IFPEN, from Argus

**Class II: HEFA-SPK from recycled vegetable oils (UCO, POME), enabling a reduction in greenhouse gases of 85% min.

The world’s leading HEFA producer is Finland’s NESTE, which operates plants in Singapore and Porvoo, Finland. In Europe, it is mainly the oil companies Repsol (in Spain), TotalEnergies (in France), ENI (in Italy), BP (in Spain and Germany) and soon Shell (in Rotterdam) that have the largest HVO production capacities capable of meeting potential HEFA demand. Asia also has a plant in China, and the United States has two operational plants.

Furthermore, there are some forty new SAF production projects on the American continent (Canada, USA and Brazil), including thirty or so in the USA, thirty or so on the Asian continent and nearly fifty on the European continent. These projects include HEFA-SPK technology, as well as projects for FT-SPK production using the biomass-to-liquid process, Alcohol-to-Jet, and numerous FT-SPK projects using the Power-to-Liquid (or e-fuel) process.

In France, an incentive tax (TIRUERT10) and a 1% incorporation target have been specifically defined in the 2022 finance law for renewable jet fuels. This rate should rise to 2% in 2025, then 6% in 2030. In order to contribute to the national supply of SAF, several new FT-SPK industrial projects are currently being studied by the French environment and energy management agency (ADEME) for the award of investment grants, including 2 lignocellulosic biokerosene projects and 2 synthetic kerosene (efuel) projects based on biogenic and industrial CO2. It should be noted that the Air-France-KLM group was the airline that used the largest volume of SAF in 2023 (80 kt), and has set itself the goal of incorporating 10% SAF by 2030.

The emerging role of biofuels in maritime transport

In maritime transport, most ships in service across the world today use heavy fuel-oil, consuming around 280 Mtoe of oil-based fuel per year. The International Maritime Organization (IMO) has established regulations to limit the sulfur content of ship fuels. This limit was tightened in 2020, resulting in a 70% reduction in total sulfur oxide emissions from shipping. In addition, for several years now, players in the maritime sector have been calling on the industry to align itself with the 1.5°C trajectory of the Paris Agreement. Other highlights for 2021 include the gradual evolution of on-board technologies, enabling ships to run on a variety of alternative fuels. More recently, in July 2023, the European Union adopted a new law stemming from the Maritime FuelEU initiative, aimed at reducing GHG emissions from the maritime sector (to -2% by 2025 and -80% by 2050), notably through using renewable and low-carbon fuels11.

Worldwide, the main renewable alternative fuels under consideration today are biodiesels (FAME and HVO), biomethane (Bio-LNG), biomethanol, ammonia and their e-fuel synthetic versions (e-diesel, e-methane, e-methanol, e-ammonia). Preference is given to electrification and hydrogenation for dockside power requirements and river transport.

Today, the main alternative fuel to marine fuel-oil is fossil LNG. In 2023, 355 LNG-powered vessels were in service and some 400 were on order worldwide. The pace has picked up sharply in recent years. The majority of LNG bunkering infrastructures are located in Europe, but all continents are now equipped (with a single port in operation on the African continent and in South America). Bio-LNG is still not widely used, but by mid-2023, would be available in nearly seventy ports around the world, including Singapore, Rotterdam and the East Coast of the United States, according to SEA-LNG.

In addition, the first marine biodiesel bunkering operations were carried out in 2022 in the ports of Rotterdam and Singapore, involving around 280 ktoe of blended biodiesel (FAME and/or HVO). Other types of marine biofuels are currently at the pilot and demonstration stage.

Focus on France

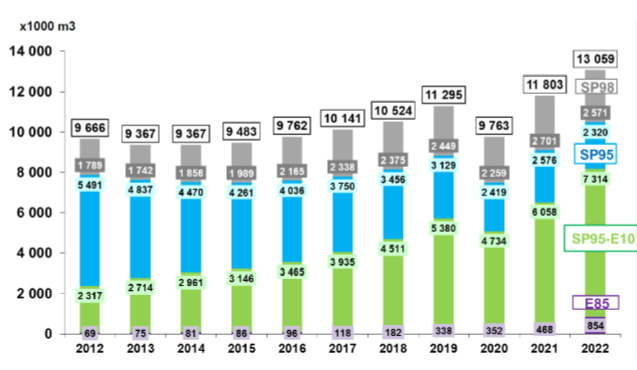

In 2022, France incorporated a total of 5.2 million m3 (or 3.7 Mtoe) of liquid biofuels in the fuels distributed throughout the country, up 18% from 2021 and the highest level ever recorded. Most of these biofuels are diesel substitutes (2.7 Mtoe), followed by gasoline substitutes (0.95 Mtoe) and for the second year, a share of jet fuel substitutes (0.028 Mtoe).

Since 2017, SP95-E1012, which contains up to 10% by volume of ethanol, has been the most consumed fuel by French gasoline vehicle owners, with a market share of more than 58% by the end of 2022. Super ethanol E85 (gasoline containing up to 85% ethanol by volume), dedicated to Flex-fuel vehicles and gasoline vehicles fitted with conversion boxes, continued its growth, with a market share of 6.5% of gasoline and a total consumption up +83% compared to 2021. The number of service stations distributing E85 also continued to grow. This fuel is now readily available in 36% of national service stations.

consumed in France in thousands of m3.

Source: SNPAA 2022 from CPDP (French Professional Oil Committee)

The years 2021 and 2022 were also marked by a two-fold increase in the number of approved E85 conversion boxes fitted, i.e. a total of 226,000 gasoline vehicles kitted out by the end of 2022. Sales of production Flex-E85 vehicles also rose by 33% in 2022, for a total of 83,300 vehicles and 2.1% of registrations in January 2023. Alternatives to gasoline also include a share of HVH-E13, which remains a minority (3.3% of substitutes). With no mixing limits, this biofuel is not currently restricted by any specific indication at the pump.

In terms of fossil diesel substitution options, FAME, and in particular VOME14, continue to make up the majority (90% of the biodiesel mix), followed by HVH-G15 (or HVO biodiesel). After a period of stagnation, the biodiesel market is on the up again, with a diversification of waste oil resources (flotation fats, oil mill effluent and other industrial waste) that can be double-counted to meet regulatory incorporation targets.

Lastly, for biofuels, there is also a growing share of biomethane incorporated into NGV. In France, the share of bio-CNG in total CNG consumption has risen from 19% in 2021 to almost 36% in 2022, representing a consumption of 92 ktoe of biomethane.

The segment with the largest share of NGV vehicles is light commercial vehicles (nearly 9730 vehicles by the end of 2022), followed by heavy-duty vehicles, with France’s NGV heavy-duty truck fleet being the largest in Europe (8,856 vehicles). Next come buses and coaches (+30% growth by 2022) and finally refuse collection vehicles (nearly 15% of the vehicles on the road).

Outlook for carbon neutrality

Investment outlook

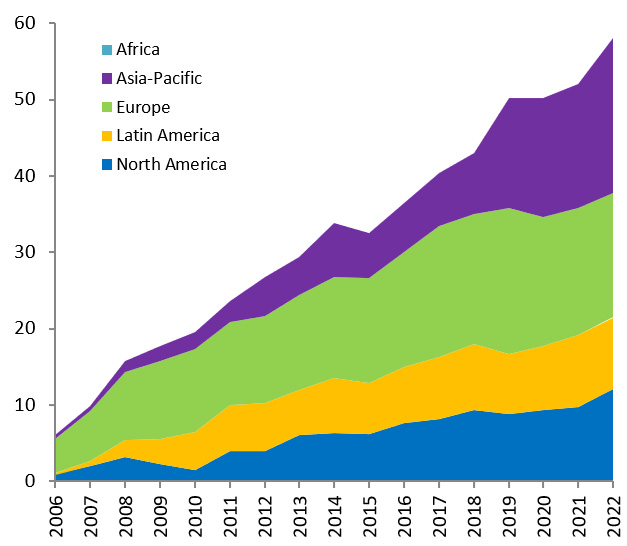

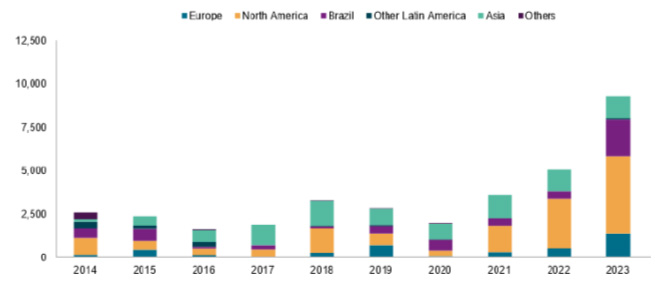

After a period of relative stagnation, global investment in liquid biofuels is seeing a clear upturn, reaching nearly 5 billion dollars in 2022 and an estimate of nearly 10 billion dollars for 2023 according to S&P Global. This investment could represent an increase in global biofuel production capacity of + 7 Mt, bringing total production capacity to 230 Mt.

per geographic region (in millions of dollars).

Source: S&P Global 2023

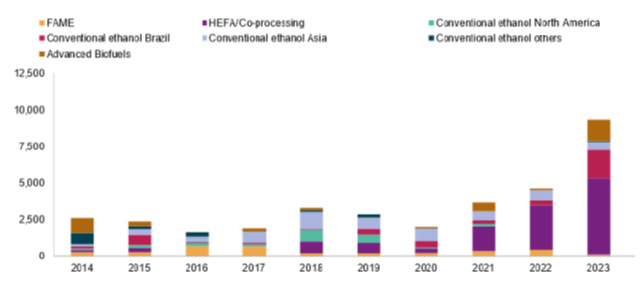

per product (in millions of dollars).

Source: S&P Global 2023

The vast majority of this growth is in the production of HEFA biokerosene coupled with HVO biodiesel production, mainly in the United States (for 50% of all investments), but also in Europe (Repsol plant in Spain in particular) and a shift towards biodiesel in Indonesia. By 2024, the new capacities of TotalEnergies’ Grandpuits plant in France and NESTE’s Rotterdam plant are scheduled to come on stream. HEFA/HVO production capacity could reach 16 Mt by the end of 2023, half of which would be in the United States. Conventional ethanol also accounts for a significant share of new investments in 2022 and 2023, particularly in Brazil and India, which has set ambitious goals for the widespread deployment of E20 by 2025-2026 (i.e. the incorporation of around 9 Mt of ethanol).

Investments in lignocellulosic processes are still relatively modest. In addition to American and Indian projects, Raizen is developing cellulosic ethanol production capacities in Brazil. Shell has agreed to deliver 2.5 Mt by 2037 from 5 new plants deployed within existing sugar mills that will come on stream between 2025 and 2027. Shell also has 4 plants potentially operational by 2023, representing an expected capacity of 550 kt of 2G ethanol.

Lastly, as for the BtL process, out of the 6 plant projects in the United States, the first plant, owned by a company called Fulcrum in Nevada, is now in the start-up phase. France is not lagging behind in this technology, with two new investment projects announced this year for the construction of the first two BtL plants, the BioTJet16 and Hynovera17 projects. These projects for the production of biokerosene and synthetic biodiesel, mainly from wood residues, will get their investment decision confirmed in 2024 for a production start-up by 2027.

So, based on existing announcements, the global biofuels market could increase by 23% over the next 5 years, reaching 160 Mt by 2028. HVO and ethanol account for two-thirds of this growth, with FAME and biokerosene accounting for the remaining third.

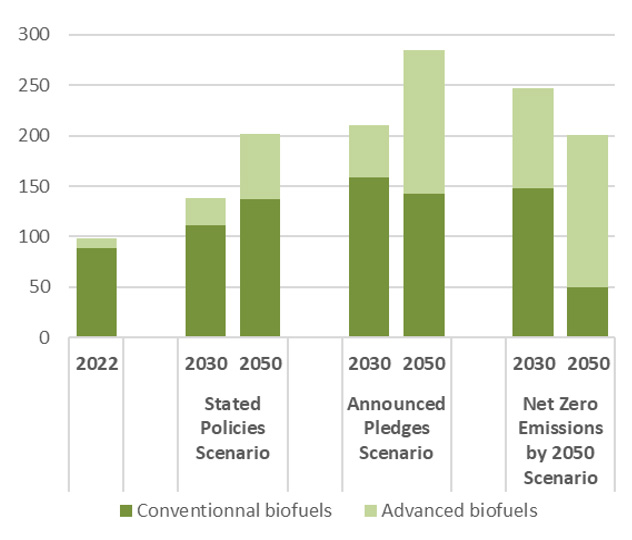

A stronger position for biofuels in medium/long-term scenarios

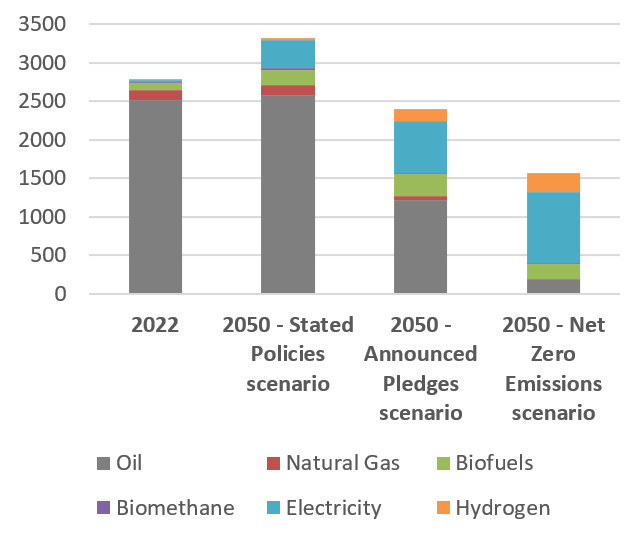

With the adoption of carbon neutrality goals being rolled out across all states, decarbonization solutions for emitting sectors are set to grow and diversify. For the transport sector, the main technological solutions are electrification, natural gas, hydrogen and biofuels. As each solution has its limits, most energy scenarios for 2050+ envisage rolling out all of these solutions, and especially biofuels, at different levels. The scenarios in the International Energy Agency’s World Energy Outlook (IEA, WEO 2023) all envisage growth in the biofuels market, with a minimum of 200 Mtoe (i.e. double the size of the current market) and a maximum of 285 Mtoe in 2050.

for the 3 IEA-WEO scenarios (in Mtoe).

Source: IFPEN from AIE, WEO 2023

for the 3 IEA-WEO scenarios (in Mtoe).

Source: IFPEN from AIE, WEO 2023

Even if there is still room for growth with conventional biofuels (up to a total of around 150 Mtoe), advanced biofuels will take over from 2030 onwards, and will become the mainstay by 2050.

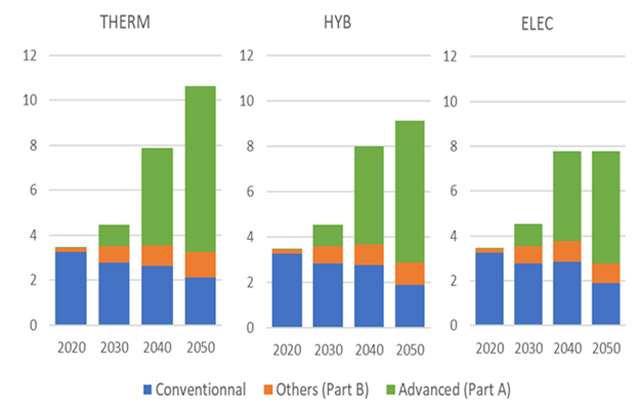

The same holds true for France, with ADEME’s “Transitions 2050” scenarios forecasting an increase in consumption of between 5.6 and 11 Mtoe by 2050, depending on the scenario (compared with 3.7 Mtoe today). Furthermore, in a report published in November 2023, the French energy research alliance ANCRE presents an analysis of 3 decarbonization scenarios for the French transport sector in 2050, by factoring in the law to phase out the sale of internal combustion vehicles by 2035.

for the transport (in Mtoe) sector.

Published by ANCRE, 2023

For the entire French transport sector, biofuels are expected to increase from 7.7 to 10.5 Mtoe by 2050, with an analysis of biomass requirements based on availability trajectories defined at the national level. While the transport sector alone does not appear to pose a risk of pressure on national biomass resource potential, meeting the biomass needs of all energy sectors will require the implementation of specific supply chain deployment measures, particularly when it comes to mobilizing lignocellulosic resources (wood residues, harvest residues, or even fast-growing dedicated crops).

Daphné Lorne - daphne.lorne@ifpen.fr

![]() [1] LPG: Liquefied Petroleum Gas

[1] LPG: Liquefied Petroleum Gas

[2] NGV: Natural Gas for Vehicles

[3] UCO: Used Cooking Oil

[4] PFAD: Palm Fatty Acid Distillate

[5] B10: Diesel containing up to 10% volume of FAME biodiesel

[6] EBA: European Biogas Association

[7] HEFA-SPK: Hydroprocessed Esters and Fatty Acids – Synthetic Paraffinic Kerosene

[8] FT-SPK: Fischer-Tropsch – Synthetic Paraffinic Kerosene

[9] ATJ-SPK: Alcohol-to-jet - Synthetic Paraffinic Kerosene

[10] TIRUERT: Taxe Incitative Relative à l’Utilisation d’Energie Renouvelable dans le Transport (a tax to encourage the use of renewable energy in transport)

[11] https://data.consilium.europa.eu/doc/document/PE-26-2023-INIT/fr/pdf

[12] SP95-E10: Lead-free 95 gasoline containing up to 10% by volume bioethanol

[13] HVH-E: Huiles Végétales Hydrogénées de type Essence (synthetic gasoline from hydrogenated vegetable oils)

[14] VOME: Vegetable Oil Methyl Ester

[15] HVH-G: Huiles Végétales Hydrogénées de type Gazole (synthetic diesel from hydrogenated vegetable oils)

[16] BioTJet: https://www.ifpenergiesnouvelles.fr/article/decarbonation-laviation-elyse-energy-et-ses-partenaires-lancent-projet-biotjet

[17] Hynovera: https://concertation.hynovera.fr/le-projet-hynovera/

You may also be interested in