01.09.2018

2 minutes of reading

Sub-Saharan Africa has many advantages to face a dynamic of sustainable economic development. According to the United Nations (UN), the region is endowed with significant energy and mineral resources and its population is expected to double by 2050. However, unlike emerging Asian countries, African countries have benefited little from the rapid growth of globalization in the 1990s, hampered by their lack of industry and weak energy system. Under these circumstances, could a massive, organized deployment of renewable energies be the key to African development in the years to come?

Sub-Saharan Africa (SSA) is one of the richest regions in terms of natural resources1. Naturally, it has been subject to increased attention in recent years. With a young and growing population, it appears to have all the elements necessary for a significant development of its economy. However, the continent’s lack of infrastructure and/or obsolete equipment in key sectors such as water and electricity2, transport and industry have undoubtedly hampered inclusive economic growth in African countries. After explaining its potential in terms of natural resources and the delays in electrification of the region, we will examine the role that renewable energies could play in the coming decades. Renewable energies could become a significant factor for growth in SSA, due to its considerable untapped potential3, its rapid technological development and the drop in prices4 observed over the past 20 years. They would enable off-grid electrification for rural populations5 and support sector-based initiatives in the future.

A sub-continent with under-exploited resources

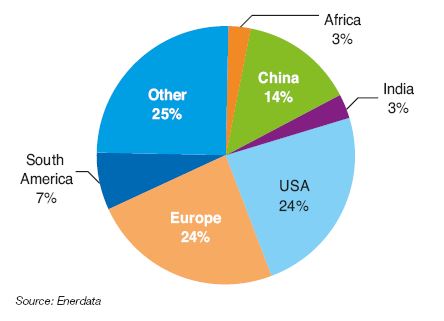

The SSA has the dual advantage of being extremely rich in natural resources and human capital. Proper management of these two elements could ensure its future economic development, though the region currently represents only 3% of global gross domestic product (GDP) and 2% of global trade in terms of value (Fig. 1)6.

A region rich in raw materials

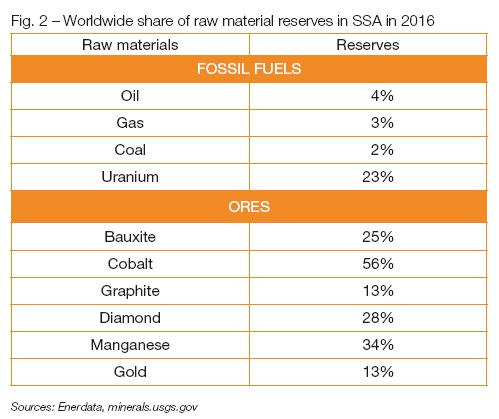

SSA has 3% of global gas reserves, 4% of oil reserves and 23% of uranium reserves, as well as significant mineral resources including 25% of bauxite (Guinea), 56% of cobalt (Democratic Republic of the Congo) and 28% of diamonds (Fig. 2).

Fig. 2 – Worldwide share of raw material reserves in SSA in 2016

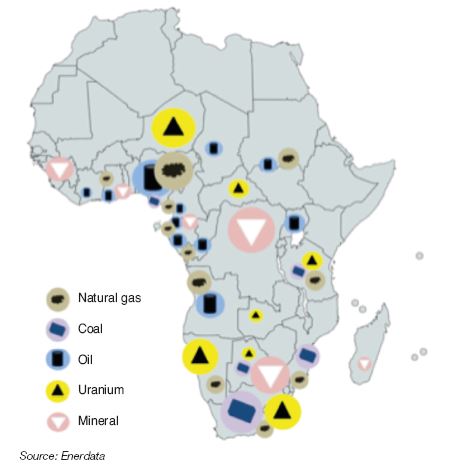

Some countries such as Nigeria and Angola hold the largest share (58% and 18% respectively of the sub-continent’s oil reserves), but overall, natural resources are relatively dispersed across the region (Fig. 3)7. There is oil in the Gulf of Guinea (55 billion barrels (Gb), 85% of SSA’s reserves)8, and uranium in the south, with 31% in Niger and 63% in the southern part of the continent, in Namibia, South Africa and other countries (Enerdata 2016)9. But like many countries around the world with a wealth of natural resources, the growth of African producers suffers from weak economic diversification and a form of deindustrialization that has taken place since the 1970s, mainly due to heavy dependence on the cyclical raw materials markets. In addition, weak infrastructure, traditional specialization in low value-added production (energy and mining extraction without processing) and problems with oversight of natural resource management have historically hindered the development process.

There are many paradoxes, such as Nigeria, SSA’s leading economy in terms of GDP, but where 60% of the population (112 million people) currently live below the international poverty threshold10.

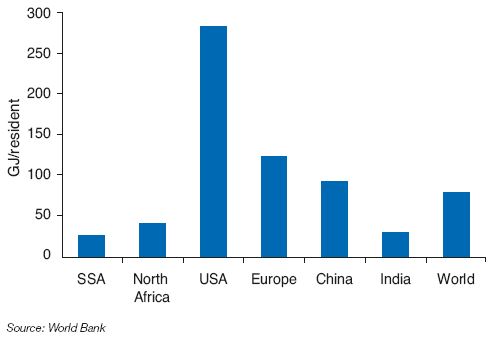

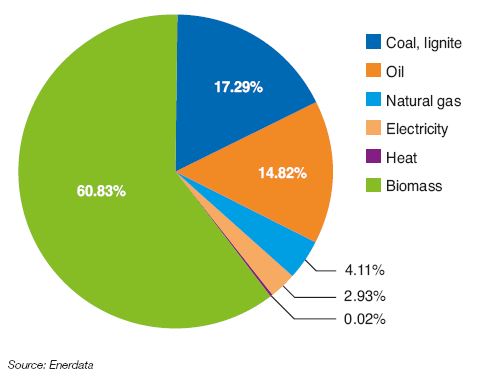

Primary energy consumption in SSA remains significantly below the worldwide average (0.7 toe11 per capita compared with 1.9 toe per capita in 2014) (Fig. 4). The primary energy mix relies largely on the use of biomass (61%) and fossil fuels (34%), including nearly 17% coal (Fig. 5)12. CO2 emissions are among the lowest in the world’s inhabited regions, currently representing around 4% of the world’s total, with about 17% of the population13. However, demographic projections to 2050 and the expected growth in development have prompted fears of a significant rise in emissions during the coming years14.

Fig. 3 – Location of resources in SSA in 2016

Fig. 4 – Primary energy consumption per capita in 2016

Fig. 5 – Primary energy mix in SSA in 2016

An up-and-coming demographic force

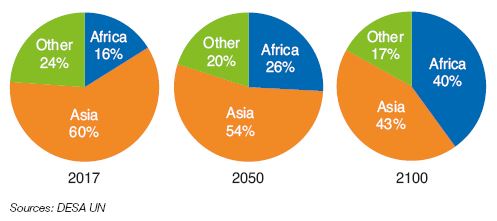

According to the UN, Africa’s population currently represents 17% of the world’s total (1.26 billion people) and is expected to double by 2050 to reach approximately 40% of the global population in 210015 (Fig. 6). SSA represents 85% of the continent’s population, with a 2.8% growth rate, 0.1% higher than the average in Africa16.

Fig. 6 – Change in global population distribution

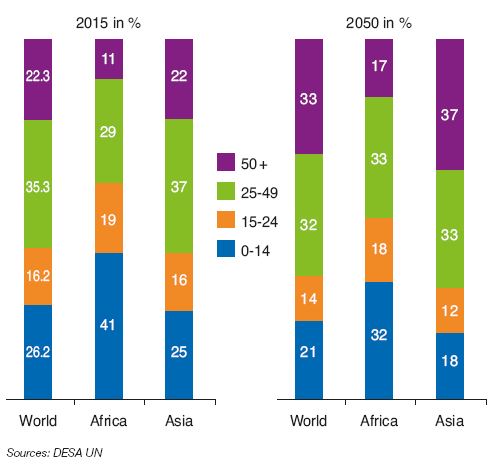

The labor force is young and abundant, with 60% under age 25 (Fig. 7), but the unemployment rate, though somewhat varied across the region, is close to those seen in the Occident (9% unemployment in Africa in 2016, 4% in China and 8.2% in the European Union17). Each year, demographic dynamism brings 12 million additional workers into the labor market.

Fig. 7 – Worldwide distribution of population by age group

However, low productivity in the agricultural and industrial sectors makes African workers less competitive than their counterparts in emerging countries in Asia18. This is even morethe case since access to basic education is not guaranteed throughout the region, and elites leave the continent for better job opportunities in Europe and the United States. According to UNESCO, in 2015, African students represented one-tenth of worldwide student mobility (74% of whom came from sub-Saharan Africa). Nearly 50% of these sub-Saharan African students lived in an OECD19 country20.

Industry: weak infrastructure and a lack of economic diversity

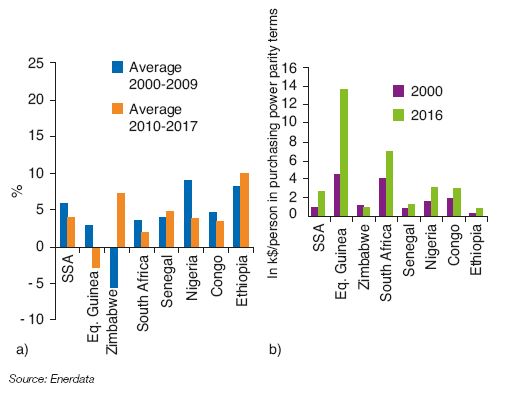

Over the past ten years, certain African economies have experienced growth rates among the highest in the world. This resulted in a €300 increase in GDP per capita in SSA between 2010 and 2017, a figure which remains low in comparison to emerging Asian countries (for example, +€10,000 per capita over the same period in South Korea). Oil producing countries (Nigeria, Democratic Republic of the Congo) recorded very strong growth from 2000 to 2009, but experienced a subsequent economic slowdown, related to changing oil prices (Fig. 8). Countries in the east and in the west, with fewer resources but more diversified economies, are currently more dynamic. But growth in Africa is far from inclusive. It offers little structural change, job creation or poverty reduction.

Fig. 8 – Growth rate of GDP (%) (a) and per capita GDP (in k$/cap in purchasing power parity terms) (b)

In its 2018 report, addressing the economic situation in Africa, the African Development Bank (AfDB) noted that industrial expansion is essential to economic and social development in SSA. 31 out of 35 countries drafted an Emerging Plan by 2025 or 2030, giving priority to industrial development. However, at the present time, the latter mainly relies on the extraction and export of raw materials, a sector with few local jobs and largely dependent on relationships with companies (national or foreign) operating in the region. African industry still creates few jobs (11% of industrial jobs in Nigeria, 8% in Angola, the two largest oil exporters in SSA), compared with 27% in China and 25% in South Korea21. Political tensions related to resource appropriation create a tense business climate and constant insecurity.

A considerable delay for electrification

In 2015, SSA accounted more than one-half of the world’s poor compared with one quarter in 200222.

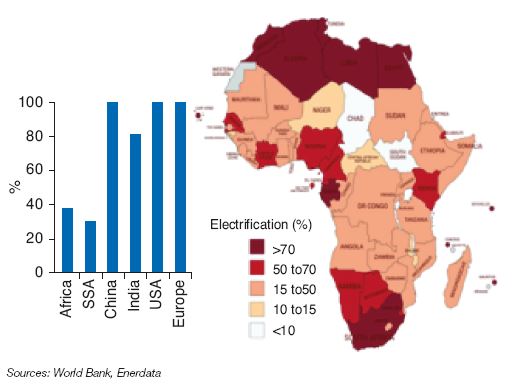

In general, there is a significant lack of infrastructure in SSA. According to the AfDB23, between $130 to 170 billion is needed annually for infrastructure development. The electricity sector is a top priority. In 2016, 57.2% of the population in SSA (591 million people) (World Bank) did not have access to electricity24. Most Africans connected to the grid suffer from frequent power outages that impede any significant economic activity25 Consumption is very low: 430 kWh/person on average in the region, one-tenth of that of China, and one-thirtieth of that of the United States of America26.

The geographic disparities are notable: countries such as the Seychelles have an electrification rate of nearly 100% while Chad and Burundi fell below 10% in 2016, according to the WEO 2017 (Fig. 9). It remains significant disparity between rural and urban areas, with average electrification of 22% for the former, compared with 71% for the latter in 201627. Looking at the continent as a whole, electrification is gradually increasing (+9% between 2000 and 2017) thanks to policies and actions put into place. In 2018, for the first time, the rate of electrification in the region exceeded its population growth rate28. Nevertheless, significant regional disparities remain, and some countries such as Mali have in fact lost power capacity (–2.6% between 2010 and 2016), with infrastructure being destroyed by war or terrorism29.

Fig. 9 – Electrification rate in 2016

There are many consequences for the population and the economy. In areas without electricity, young people cannot study at night, farmers cannot track changes in the price of their products on local markets, and women, who spend an average of 1 to 5 hours a day harvesting wood30, have difficulty accessing employment and independence.

From an economic perspective, transmission and distribution losses (23% on average, up to 48% in Rwanda) and low production (1.8% of worldwide electricity production for 17% of the population) lead to frequent power cuts. Between 2010 and 2017, there was an average of 8.9 power outages per month in SSA which could last for 5.8 hours31. Companies must use emergency diesel generators to overcome weaknesses in the grid, which burdens their finances and does nothing to improve the business climate (Liberia and Chad produce more than 50% of their electricity through individual diesel generators)32. Most African countries are ranked at the bottom of the Doing Business 2017 list prepared by the World Bank.

Thus, it is urgent to prepare a structured, realistic plan, which can be quickly deployed with a lasting impact on society as a whole, in order to develop the electricity sector in SSA.

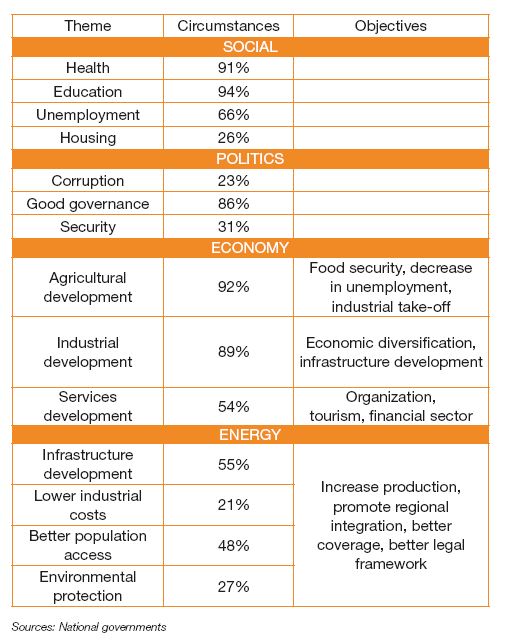

From the end of the 1990s, African governments, upon the advice of the World Bank and the AfDB, focused on the need for long-term planning for their countries’ economic and social development. As mentioned previously, 35 countries established an Emerging Plan by 2025 or 2030. In these plans, the 35 signatory countries list the main objectives to transform their countries, and the means to achieve them. Many themes are recurrent, others more specific to resources, the economic situation and governance (Tab. 1).

Table 1

Emerging Plans in SSA

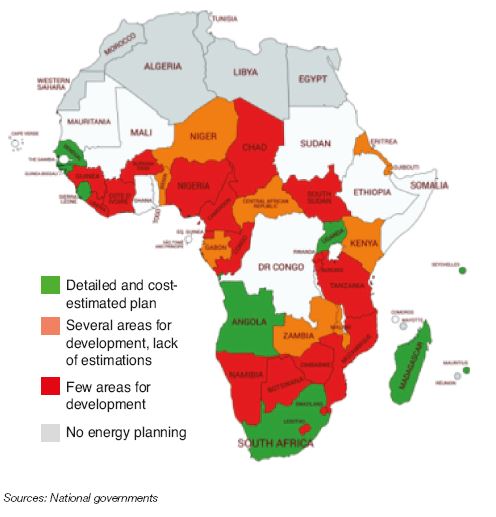

But these plans are often too vague to be implemented as they stand or are not sufficiently realistic to lead to sustainable development. They do not yet constitute medium-term planning for the country’s economy and energy infrastructure needs. Budget figures for these development plans are only provided in ten reports. As for the energy sector, the budget allocated for this purpose has only been mentioned by four countries33. In terms of energy development, only seven plans provide figures underlying their new production capacity and grid coverage objectives; most of them only provided a few action items for deployment (Fig. 10).

Fig. 10 – Quality of energy planning

Renewable energies, a vector for Africa’s economic and social take-off?

According to the World Bank, demand for electricity in Africa is expected to double current production by 2030.

It estimates that, to meet the goals of the Sustainable Energy for All (SE4ALL) initiative, substantial investment would be required. For access to electricity alone, the World Bank had estimated the needs in 2014 at around 34 billion dollars per year worldwide, and 20 billion dollars per year – nearly 60% of the total –for sub-Saharan Africa alone34. These figures are well below the values of the African Development Bank.

However, between 1990 and 2012, excluding Chinese investments made since 2010, investments in the electricity sector in sub-Saharan Africa never exceeded $600 million per year35. And only 0.3% of the continent’s renewable energy potential is currently being used, while technological progress makes renewable solutions more and more financially attractive, given the lack of network infrastructure in place.

Solar off-grid: unprecedented natural and economic potential

According to the IEA36, 60% of new electrification by 2030 will be carried out via off-grid and mini-grid, benefitting from increasingly low costs. SSA suffers, on the one hand, from a double problem of lack of grid coverage and its obsolescence, leading to high maintenance and expansion costs, particularly in the most remote areas. On the other hand, African electricity production remains very carbon-intensive (70%), with renewable energies accounting for only 27% (of which 24% hydropower) and nuclear energy for 3% with a power plant located in South Africa, and dependent on foreign refined oil imports which weakens the economies’ finances (Fig. 11).

%20in%20SSA%20in%202016.JPG)

Fig. 11 – Electric power mix (production) in SSA in 2016

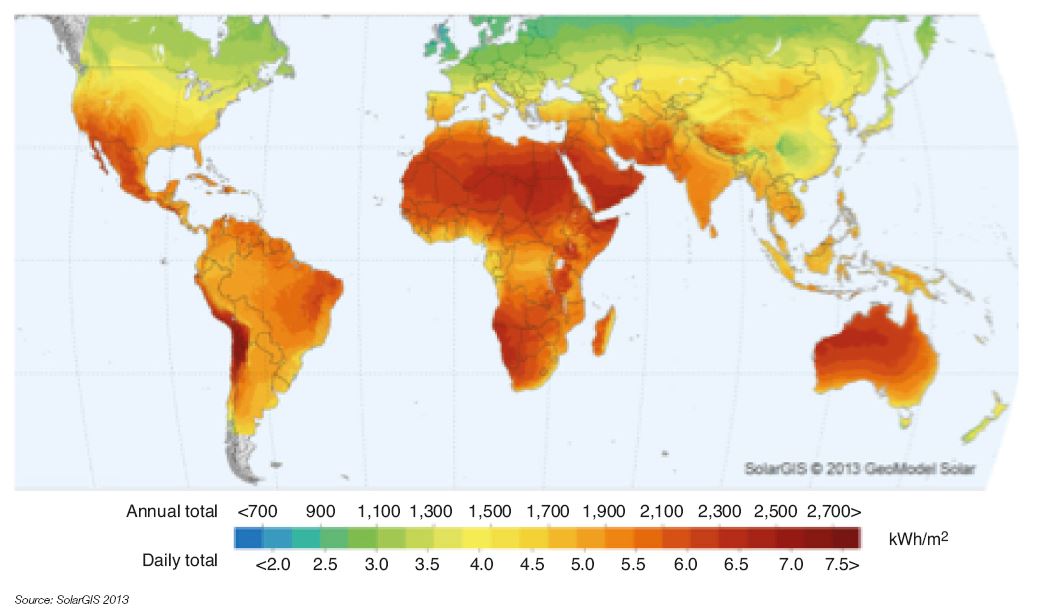

Nevertheless, the African sub-continent has unequalled potential for renewable energy, especially solar (10 TW) and hydroelectric (350 GW, 10% of worldwide potential)37, which, combined with off-grid technologies, could quickly and cost-effectively reduce the problem of access to electricity in rural areas.

Off-grid technologies are composed of a small power generation system (often photovoltaic solar power, sometimes small hydro) coupled with a short-range distribution system and storage batteries. The smallest, Solar Home Systems (SHS), supply one to five households, while the largest can supply a village of up to one thousand households (capacity from 5 kW to 1 MW depending on the system)38. Their installation requires a favorable natural environment, the ability to make initial investments and pay for consumption on site.

The significant amount of sunshine in the region (Fig. 12) coupled with relatively low population density (43.8 inhabitants/km² on average, compared with 144 in China and 403 in India) facilitates the deployment of solar panels. More and more local entrepreneurs are partnering with foreign companies (EDF in Senegal and Ivory Coast for example) to transfer technologies, install systems and train the local population.

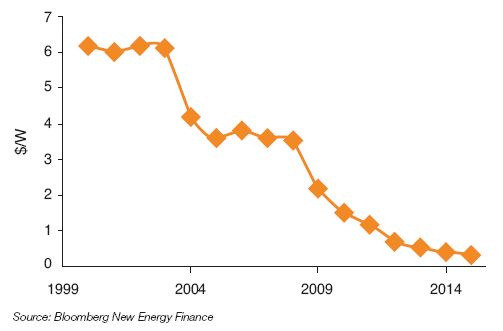

The initial investment needed to build a photovoltaic system has decreased considerably in recent years (Fig. 13). According to Irena, photovoltaic solar power (PV) is the energy source with the lowest production costs in most African countries. Lighting for a household costs between $4 and $15 per month with a diesel generator, compared with $2 per month with solar PV39. However, this estimate does not take into account the additional cost incurred to purchase a storage system (battery) for the household, even if its value should decrease in the coming years. The initial investment remains greater for a solar power system, but allocation of costs over the lifecycle makes the solar power system more attractive over the long term.

Fig. 12 – Average annual sunshine worldwide

Fig. 13 – Change in price of photovoltaic cells

In addition, the boom in the telephony market in Africa over the past five years, with 420 million subscribers in sub-Saharan Africa (a penetration rate of 43% in 2016) and according to Deloitte, 660 million Africans will have a smartphone by 2020, almost doubling. This dynamism should make it possible to resolve, in part, the issue of financing. The “Pay-As-You-Go” principle consists for the consumer in making an initial payment for the installation, based on their means, and then to buy the electricity s/he needs. Another model, promoted by the worldwide leader of off-grid solar power, the Kenyan company M-Kopa, consists of installing SHS in individual dwellings, then offers regular payment terms, according to their means, until the customer becomes the owner of the system. If the buyer misses a payment, the supplier can cut off the power supply remotely. M-Kopa has distributed thousands of systems throughout East Africa and claims that it provides electricity to around 500 new households each day.

Expected externalities for the economy

In the agricultural sector, the off-grid system could supply a refrigeration system to conserve perishable goods or low-powered agricultural machine to assist manual labor. Using a mobile phone, agricultural producers could access the price of their products on local markets. In addition, solar-powered pumping systems could irrigate crops and more effectively supply water to livestock. Productivity gains in the agricultural sector could enhance the wealth in rural areas, reducing the need for the latter, with a shift of manual laborers to the industrial sector.

Specifically in industry, off-grid solar power can hardly meet the electricity needed to operate a factory. According to ADEME40, operation of a motor-driven weaving loom requires electrical power of 0.1 to 10 MW. But the largest off-grid solar power systems have a maximum capacity of 1 MW, and it requires far more than one motor to operate a textile factory.

Large hydroelectric or solar power plants could meet industrial demand, but according to IRENA41, the cost of hydroelectric power is expected to remain higher than the cost of fossil fuels until 2020, without mentioning the need to invest in storage capacity due to intermittent production of some types of renewable energy systems, particularly solar. Thermal power stations currently being developed, which are more economically attractive with proven technologies, seem to be the logical choice for wide-scale industrialization. However, they can and must be deployed responsibly. Energy efficiency must be a priority, with consistent effort within the grid infrastructure to limit losses and improve production processes in the industrial sector.

If household consumption turns off-grid, there will be less pressure on the grid, hopefully resulting in improved performance. But renovations must be carried out to reduce the amount of energy lost from transmission and distribution networks. Production cycles can also be optimized to improve energy efficiency, through better management of heat transfers and improved waste-to-energy schemes. Finally, the impact of greenhouse gas (GHG) emissions, though unavoidable, can be minimized by reducing households’ emissions using off-grid renewable energy sources.

In the services sector, off-grid power sources provide a significant contribution. Shops, financial services and public institutions have consumption slightly greater than a household’s consumption. Therefore, an off-grid solar power installation could supply a butcher shop or a bank branch, thus promoting growth within the services sector.

Renewable energy power plants: a distinguishing feature of African industry; versatile and powerful potential

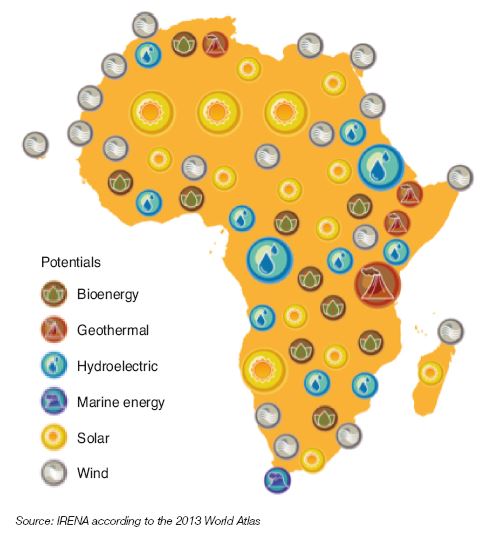

Apart from sunshine, the region offers tremendous potential for several types of renewable energies (Fig. 14) including hydroelectric power (with the Nile, Zambezi and Congo rivers), with only 8% used despite its already significant share in the electricity mix. Next is biomass, with the primary forest in Central Africa and bagasse from sugar cane plantations in the south, geothermal in the Rift Valley, and wind power along the coasts and the islands.

Since the 1990s, international investors and governments have been taking advantage of this potential, developing power plants that use these renewable resources. China has already installed 5 GW of hydroelectric production in Africa, with engineers who have become global experts in the field. Independent Power Projects (IPP) and projects, which are jointly financed by governments and development assistance organizations, are expanding rapidly42. In 2014, Kenya opened Olkaria IV with capacity of 140 MW, making this the largest geothermal power station in Africa43. In addition, since early 2018, Senegal has had four solar power stations with a total capacity of 102 MW. The AfDB also encouraged the development of hydroelectric infrastructure in its report Economic Outlook in Africa 2017, as the sector offers strong positive externalities for economic development and job creation.

Fig. 14 – Potential for renewables in Africa

Hydroelectric infrastructure specifically stands out from other investments in renewable energies due to the ability to made cross-border interconnections and create strong, positive externalities for regional development and cooperation44. In addition to the environmental and social impacts of these major projects, they help to improve energy security on a regional scale. For example, the Democratic Republic of the Congo in the center with its Inga dam (whose potential is estimated by the World Bank to be about 110 GW) and countries in the Rift valley with their significant geothermal potential (more than 20 GW according to Irena) would like to distribute their electricity outside their borders45. The World Bank estimates that the creation of an energy exchange market among West African countries would lead to savings of $5 to 8 billion per year, and ensure access to more affordable, more reliable and cleaner energy for all46. The region established a regulated electricity market in June 201847, an initiative that could expand across the entire sub-continent. But such development requires significant investment, a favorable legal framework and a skilled workforce in the field.

Conditions for success

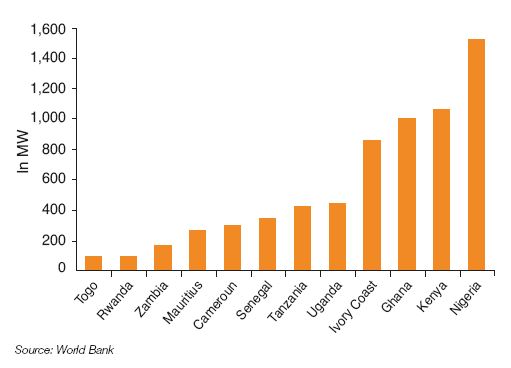

Currently there are three types of investments in SSA for energy deployment: the most significant are IPPs, bringing together private international investors and governments, with a focus on thermal production although the share of solar and wind power is increasing (Fig. 15).

Fig. 15 – Installed capacity by Independent Power Projects

in Sub-Saharan Africa in 2015

Chinese investors are closely behind, specialized in hydroelectric dams, followed by funding from development aid institutions, focused on countries that attract fewer traditional investors48.

China is a favored partner for African development, the source of 40% of direct foreign investment in SSA during 2016 ($36 billion), which helped to create 38,000 jobs. Chinese investment mainly takes place in the real estate and transport sectors49. This is not an innocuous strategy, as 13% of China’s oil imports come from SSA (8% from Angola alone); as such, these investments are in part based on its interest in energy security. In terms of exports, China floods the African markets with manufactured products, specially technological goods. It is strengthening the internationalization of the yuan by promoting the rapid expansion of trade denominated in its currency. China also lends in yuan to African countries, that have issue sovereign bonds. Rates are higher than those offered by international development aid institutions, but without the socio-economic and governance requirements concerning the use of such loans (World Bank and IMF loans at preferential rates are conditioned on taking action to promote the country’s development).

Foreign investment, while significantly growing since the early 2000s, remains insufficient to meet the growing demand of the population and economic stakeholders. Certain countries such as Uganda are more attractive due to its specific legal framework and efforts to improve the business climate (fight corruption, formalize services, energy planning, etc.).

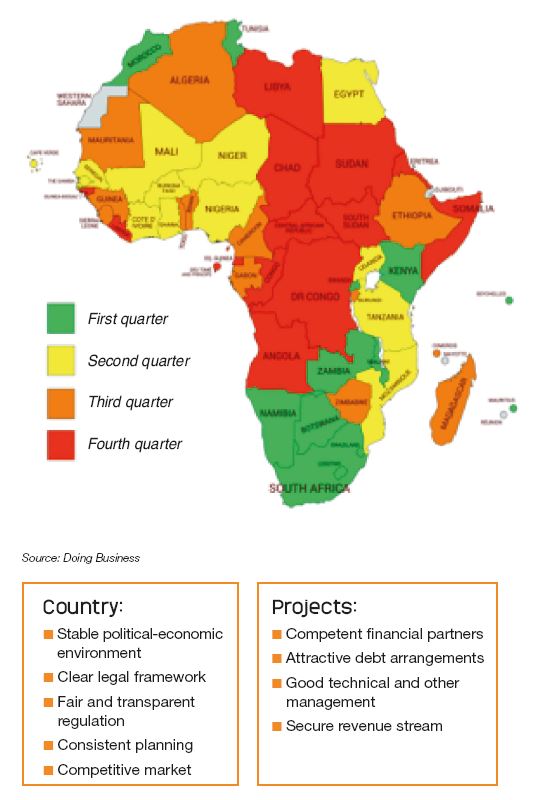

Because foreign direct investment is a major issue for electrification of SSA, the World Bank attempted to identify key factors in a report published in 201650. It also ranked SSA countries based on the ease of doing business51 (Fig. 16).

Existence of an independent energy oversight agency appears to be essential, though insufficient. 29 SSA countries currently have such agencies, with uneven performance.

Fig. 16 – Business climate in Africa during 2017

Prerequisites were also identified at host country and project level, such as low level of corruption, good planning and a consistent legal framework.

However, weak local currencies, coupled with external debt and a growing lack of liquidity among African countries, is a major practical limitation. Most African currencies have weak exchange rates and remain highly volatile, dependent on raw materials. A sudden devaluation could jeopardize the economic viability of ongoing renewable energy products or the ability to repay loans taken out. However, declining export earnings due to falling raw material prices on global markets in recent years has led to higher indebtedness for several SSA nations52 (Chad, Eritrea, Mozambique, Congo, South Sudan and Zimbabwe). Of course, this debt ratio is far below that53 seen in developed countries, particularly due to debt relief programs54 (67% of GDP on average for SSA in 2016, 95% of GDP for France in the same year), but the increase is troubling (+20% for example in SSA between 2012 and 2016)55 and the ability to repay, given their economic productivity, concerns investors and international institutions56.

Involvement of the population is key to the success of renewable energy development in SSA

Education of the African population is essential. It starts with basic education for all (current inequalities related to both location and gender), followed by specialized training and professional development (specialized courses in renewable energies at university, dedicated schools), which offers genuine job prospects. Investment in education currently remains low (Fig. 17) and many young graduates are unemployed due to a lack of connection between the university and the professional world. For example, in 2016 the employment rate for graduates in Ivory Coast was below 15%57.

Training institutes are being established, often supported by international institutions that support economic or energy development. This is the case for the Ecowas Renewable Energy Entrepreneurship Support Facility, founded in 2015 by West African governments in partnership with Irena. The institute provides training and support to local entrepreneurs who wish to engage in the renewable energies field. Chinese influence in Africa can also be seen in the educational field, with the country dedicating a significant share of its investments to develop skills in sub-Saharan Africa58.

From national development to regional cooperation

Encouraged by a better knowledge and control of new renewable energy technologies, and more generally by the desire to take part in economic development and profit from its returns, the population can be involved in electrification of the continent, particularly through crowdfunding.

The Great Dam of the Renaissance in Ethiopia is one of the first promising examples of this movement. With capacity of 6 GW, the dam is expected to enter service in 2018. Its construction was made possible through the involvement of the Ethiopian people. Following the refusal by international backers to take part in the project and disassociation by neighboring countries, the government turned to the Ethiopian population, issuing bonds that were purchased by Ethiopians and the diaspora, which enabled this $6 billion project to reach completion. Local financing initiatives such as this alleviates the challenge of attracting foreign capital and limits the geopolitical conflicts that can slow the development of international projects.

Solving inequities in the deployment of the electrical grid could open a pathway toward regional cooperation, focused on better management of energy and economic trade. The creation of organizations for regional cooperation such as ECOWAS (Economic Community of West African States) and COMESA (Common Market for Eastern and Southern Africa) reflects the desire for improved regional integration, even if results have been uneven. The creation in 2018 by 44 african countries of a continental free-trade area strengthens and expands this cooperation59.

Cross-border electrical lines are starting to appear, such as Zizabona which connects Zimbabwe, Zambia, Botswana and Namibia. Senegal even plans to extend its grid to southern Europe in its Plan for an Emerging Senegal.

Because areas with high energy potential are sometimes located along borders, structured cooperation within a precise legal framework, offering benefits for all parties, could prevent many conflicts. On the other hand, shared investment, followed by a sharing of production and profits, could be beneficial for major projects that are costly to develop, but which are essential to the development of a regional electrical grid. The Senegal River Basin Development Authority (Organisation pour la mise en valeur du fleuve Sénégal – OMVS) is already taking this step: the four member states (Senegal, Guinea, Mauritania and Mali) are jointly investing and sharing profits from dams built along the Senegal River, following to the 2015 creation of a common energy market.

The Democratic Republic of the Congo also hopes to expand its Inga dam network through the Grand Inga Project. The new dam would benefit from nearly all the capacity of the Congo River and have capacity of 39 GW. This could be redistributed to Zambia and Zimbabwe, establishing regional cooperation beyond the traditional south-central border. But the cost of this project is equal to the infrastructure, and political instability in the Democratic Republic of the Congo, combined with ongoing fears of corruption, is hindering investment and development.

Conclusion

With 70% of the population lacking access to electricity, and economic and industrial activity limited by an inefficient electrical grid, the issue of infrastructure in SSA is critical, and will require massive investment by 2025. Addressing this lack of infrastructure in the energy sector must now be considered through an approach inclusive of all populations, and in relation to the long-term economic development of each individual African country. With its significant potential in natural resources, along with clear possibility for renewable energies, many solutions are available to the various stakeholders: from off-grid options for local populations to renewable energy power plants, there is assurance of economic development, along with national – followed by regional – inclusion.

Along with the population of India, the African population is the youngest in the world. All sub-Saharan economies must take advantage of this demographic dynamism and the entrepreneurial drive of these young people, eager to invest in economic and technologically sustainable solutions adapted to their circumstances. Establishing effective institutional frameworks, and taking into account intangible aspects such as capacity-buildingt60 (education of human capital) in the planning, regulation, design and implementation of projects, could maximize the potential for development.

Consolidation of electricity production and transport infrastructure would address the continent’s industrial lag. This is consistent with the strong statement delivered by the African Development Bank in 2018 at its Abidjan summit, there is “no development without industrialization”. This inclusive approach must predominate with regard to investment in the energy sector, which remains too dependent on foreign financing.

In the end, renewable energies could be a true driver for economic development. Solutions are already in place on the continent, so the issues surrounding Africa’s economic take-off is not a question of technology. Above all, a number of different elements must be set in motion: entrepreneurial dynamics, innovative financing systems and national reforms in the various SSA countries.

Emmanuel Hache

Rebecca Martin

Gondia Seck

Final draft submitted in September 2018

(1) 4% of the world’s oil, 23% of uranium and 56% of cobalt, etc.

(2) Average losses are estimated at 15% during transmission and distribution of electricity (World Bank)

(3) 10% of global hydroelectric resources, 10 TW of solar

(4) For example, solar panels divided by 10

(5) Advantages: no dependence on foreign fuels, compatible with the customer’s income and consumption, unnecessary to connect to the grid

(6) World Bank

(7) BP Statistical Review of World Energy

(8) U.S. Energy Information Administration (EIA)

(9) World Nuclear Association

(10) https://www.brookings.edu/blog/future-development/2018/06/19/the-start-of-a-new-poverty-narrative/

(11) Tonne of oil equivalent

(12) International Energy Agency (IEA) Key World Energy Statistics 2017

(13) International Energy Agency (IEA) Africa Energy Outlook 2014

(14) International Energy Agency (IEA) Key World Energy Statistics 2017

(15) World Population Prospects: The 2017 Revision, DESA UN

(16) World Bank

(17) World Bank, 2016 Human Development Indicators; Eurostat

(18) World Bank, http://www.banquemondiale.org/fr/news/press-release/2015/06/04/boosting-agriculture-services-and-value-chains-is-key-to-africas-competitiveness

(19) The Organization for Economic Co-operation and Development (OECD) is a forum where 30 countries committed to democracy and free markets work together to address the economic, social and governance challenges posed by an increasingly globalized economy. No African countries are members of the OECD

(21) World Bank

(22) World Bank, http://blogs.worldbank.org/opendata/fr/l-extreme-pauvrete-continue-de-progresser-en-afrique-subsaharienne

(23) African Development Bank (AfDB) Economic outlook in Africa, 2017

(24) The International Energy Agency (IEA) defines electrification as follows: 250 kWh/year for a rural household, 500 kWh/year for an urban household

(25) World Energy Outlook, 2017

(26) International Energy Agency (IEA) Key World Energy Statistics 2017

(27) World Bank, 2016

(28) World Energy Outlook, 2018

(29) World Bank, 2016

(30) International Energy Agency (IEA), https://www.iea.org/newsroom/energysnapshots/average-number-of-hours-spent-collecting-fuel-per-day-per-household.html

(31) World Bank, http://www.enterprisesurveys.org/Data/ExploreTopics/infrastructure#sub-saharan-africa

(32) World Bank 2016

(33) Central African Republic, Guinea-Bissau, Senegal and Zimbabwe

(34) World Bank, Global Tracking Framework sustainable energy for all, 2014

(35) Anton Eberhard, Powering Africa: facing the financing and reform challenges, 2015

(36) World Energy Outlook 2018

(37) Enerdata, 2016

(38) IRENA Off-grid renewable energy systems; status and methodological issues, 2015

(39) IRENA, L’Afrique et les énergies renouvelables: la voie vers la croissance durable, 2013

(40) Industry: How to control your electricity consumption? Ademe 2001

(41) Rethinking Energy, Irena 2017

(42) Independent Power Projects in sub-Saharan Africa, Lessons from five key countries, World Bank Group, 2016

(43) TOTAL installed capacity of the site 593 MW in 2015 according to US Aid

(44) IEA, World Energy Outlook, 2014

(45) Cabinet of the President of the Republic, Agency for the development and promotion of the Grand Inga project

(47) West African Power Pool (WAPP).

(48) Independent Power Projects in sub-Saharan Africa, Lessons from five key countries, World Bank Group, 2016

(49) La Tribune Afrique, La Chine, premier investisseur sur le continent en 2016, https://afrique.latribune.fr/entreprises/les-nouveaux-champions-du-sud/2017-08-25/la-chine-premier-investisseur-en-afrique-747985.html

(50) Power projects in Sub-Saharan Africa, Lessons from five key countries

(51) Doing Business, 2017

(52) Debt sustainability framework jointly defined by the IMF and the World Bank for low-income countries, over-indebtedness means that a threshold value, reassessed regularly by the institutions and dependent on economic, political and social variables, has been exceeded

(53) HIPCs (Heavily Indebted Poor Countries, 33/40 of SSA countries) have benefitted multiple times from debt relief programs at the initiative of the IMF and the World Bank

(54) Initiative to support Heavily Indebted Poor Countries (HIPC) in 1996, Multilateral Debt Relief Initiative (MDRI) in 2005, etc.

(55) World bank, 2018, Africa’s pulse: an analysis of issues shaping Africa’s economic future

(56) This issue could be debated whether most of the debt results from investment in electricity production methods, or if it results from running costs without long-term externalities for the population

(57) The Conversation, les origines du problème de surqualification en Côte d’Ivoire, https://theconversation.com/les-origines-du-probleme-de-surqualification-en-cote-divoire-99004

(58) World Bank, Investir dans la jeunesse: la clé d’un meilleur avenir pour l’Afrique, https://www.banquemondiale.org/fr/news/opinion/2018/09/06/youth-key-to-strengthening-africas-future

(59) RFI Afrique, UA: 44 pays signent un accord pour une zone de libre-échange continental, https://www.rfi.fr/afrique/20180321-ua-44-pays-signent-accord-une-zone-libre-echange-continental

(60) Commonly known as “capacity building”