10.02.2021

10 minutes of reading

Like cobalt, lithium is a key component in Li-ion batteries. In recent years, the demand for lithium has grown at a steady rate of approximately 20% per year. This trend looks set to continue in the future as electrical mobility becomes increasingly popular as part of the ecological transition. However, it is not so much the geological risk that is worrying for this metal as the high concentration of reserves, production and the market, as well as China's hold on the entire value chain.

- Lithium, a key component in batteries

- Where is lithium found? Who produces it?

- Should we be concerned about lithium resources?

- What risks can be expected for lithium?

- Video: lithium in a nutshell

.jpg)

Podcast (French version)

Lithium, a key component in batteries

Lithium is in relatively abundant supply in the earth's crust, being the 32nd most represented element among the 83 significantly represented elements. In 2008, most of the known lithium resources were contained in two types of deposits: so-called "conventional" deposits, i.e. salar brines (62%) and lithiniferous rocks (27%, with a significant proportion of spodumene) and so-called "non-conventional" deposits, i.e. hectorite (clay) (7%), geothermal brines (1%) and oil fields (3%) (Evans, 2008; Bradley, 2017).

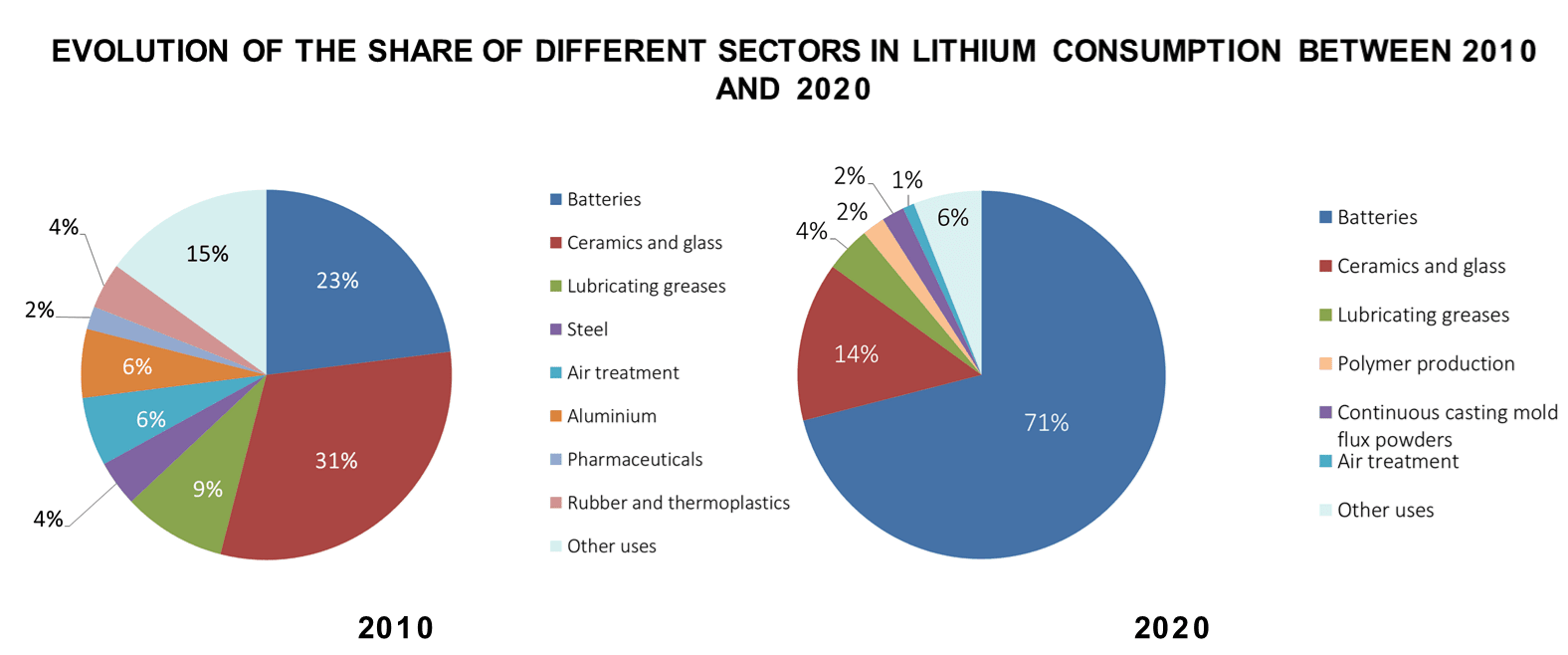

In the early days, lithium was mainly used for glass and ceramic manufacturing, for lubricating greases, or for the production of aluminum. Now, it is mainly because of its widespread use in lithium-ion batteries for electronic devices or electrified vehicles (EVs)1 that this chemical element is drawing attention. The share of batteries in total lithium consumption has increased considerably, representing 23% in 2010 against 65% in 2019 (Graph1).

Source: USGS, 2010, 2021

Where is lithium found? Who produces it?

Among the low carbon transition metals, lithium is found to be highly concentrated in terms of resources, reserves and production.

A concentration of resources and reserves in the "Lithium Triangle"

Source: USGS, 2021

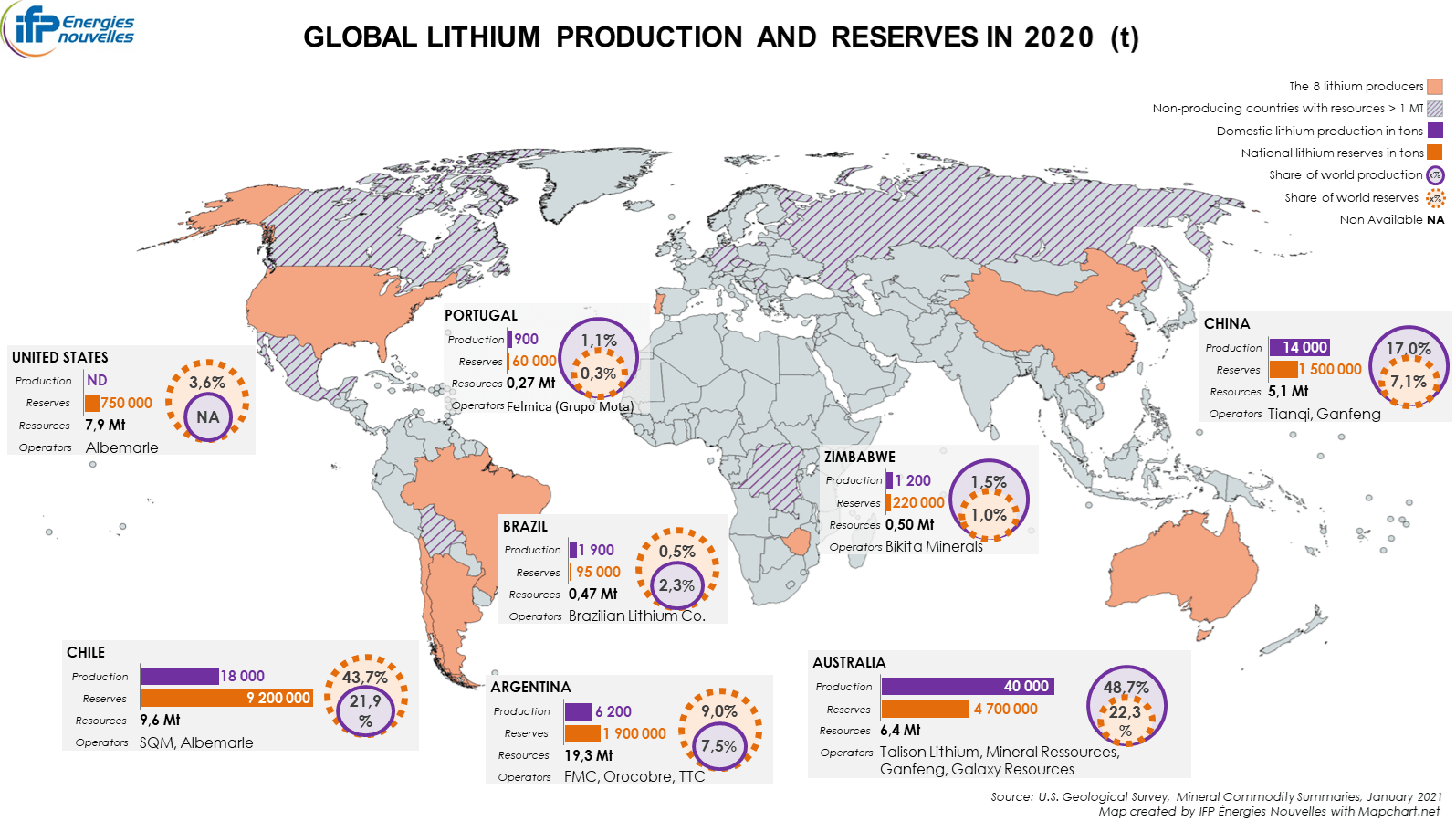

Of the 86 million tonnes of lithium resources identified in 2020, nearly 60% are held by the three Andean countries forming the "Lithium Triangle": Bolivia (21 Mt), Argentina (19,3 Mt) and Chile (9,6 Mt) (Map 1). Significant resources have also been identified in the United States, Australia, China, the Democratic Republic of Congo, Germany, Canada and Mexico.

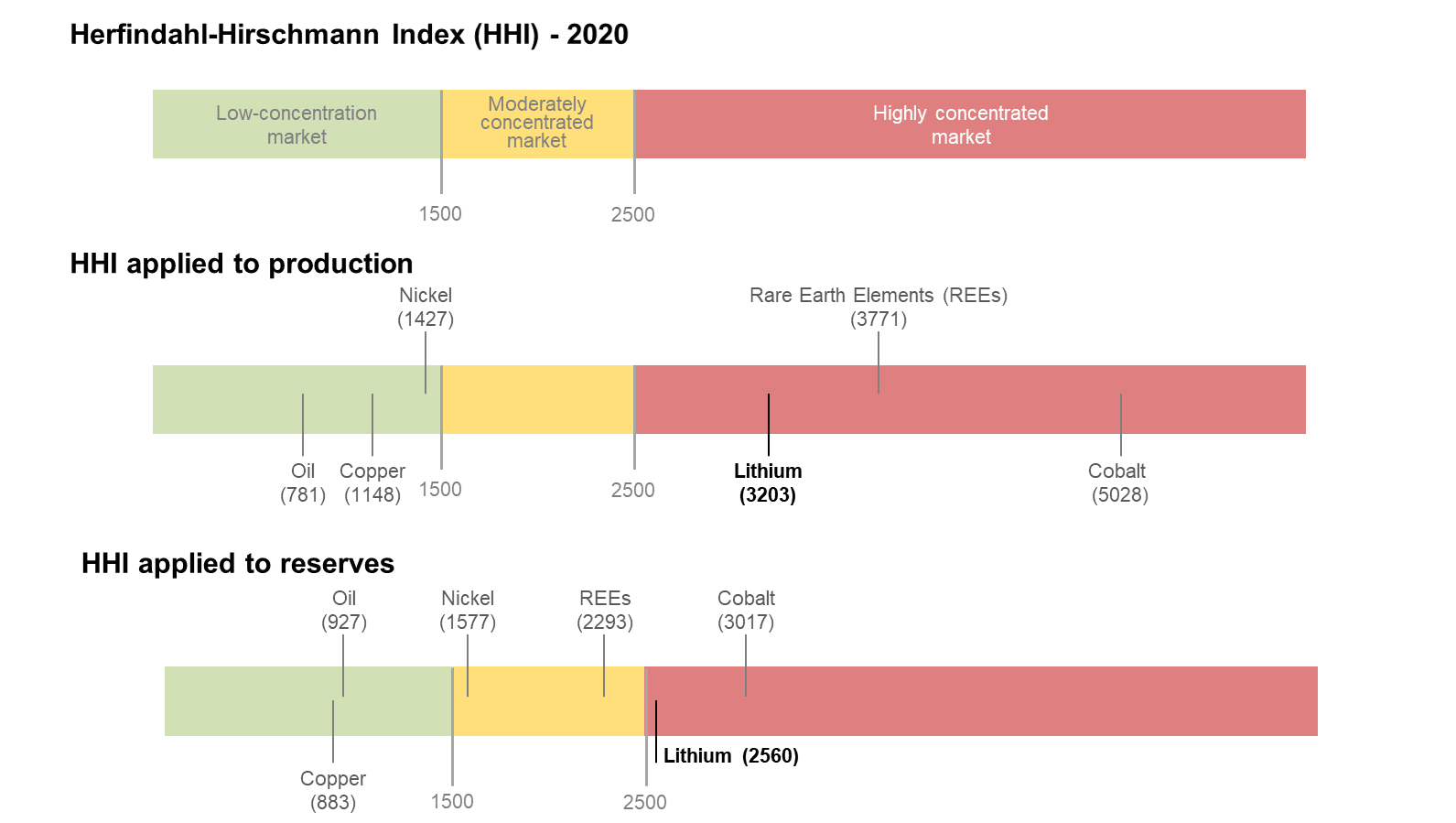

Lithium reserves are estimated at 21 million tonnes (Mt) in 2020, compared to 13 Mt in 2010, of which half are held by Chile and Argentina alone (HHI of2560) (Map 1).

Mining production is becoming more concentrated

Global lithium production has more than tripled in the space of a decade, from 25,000 tons in 2010 to over 82,000 tons in 2020. The geographical concentration of the latter has increased over the last ten years and is now greater than that of reserves (HHI of 3203 in 2019 compared to 2779 in 2010) (USGS, 2011 & 2020) (Figure 2).

Currently, two regions – Australia and Latin America – account for 80% of mining production, even if the concentration of production is not limited to these two geographic areas due to industrial holdings. Australia became the world's leading producer in 2018 (48.7% of global production), followed by Chile (21.9%), China (17%) and Argentina (7.5%) (Map 1). It is surprising that Bolivia is not part of the mining scene, given that the Uyuni Saltworks are the world's largest lithium resource.

Source: USGS, 2021

“Top 5” control the market

The lithium market is controlled by a very small number of large multinational companies - the top 5 - that have integrated the entire lithium value chain, from mining production to the production of chemical compounds (products with high added value).

Among these five players are the three long-standing producers: Chilean company SQM (Sociedad Química y Minera de Chile), American companies Livent (ex-FMC Corp) and Albemarle Corp. The other two members of this "top 5" are the two Chinese companies Tianqi Lithium and Jiangxi Ganfeng Lithium. They have entered the market much more recently and have invested heavily in overseas mining before developing expertise in the lower end of the value chain (Grant et al., 2020). Approximately two-thirds of production is said to have been controlled by Albermarle, SQM and Tianqi in 2019, suggesting a possible cartelization of the production of this strategic ore (Escande, 2018).

Tianqi's unique positioning and partnerships with two of its competitors are also attracting attention: Tianqi operates the Greenbushes deposit in Australia, one of the largest mines currently in operation, together with Albermarle and holds a 24% interest in the SQM Group.

Prices soon to be more transparent?

Global lithium production and the pace of development of mining or exploration projects are closely correlated to the selling price of lithium. However, information on the price of this metal is not readily available, especially when it comes to its unprocessed and refined forms. A lithium futures contract is expected to be launched in the first half of 2021, which would help to improve the degree of transparency in this market.

Should we be concerned about lithium resources?

The IFPEN research team used the TIAM-IFPEN model to evaluate the cumulative demand for lithium for the period to 2050 on the basis of two climate scenarios: a 4°C scenario corresponding to a temperature increase of 4°C above pre-industrial levels (4D scenario) and a more ambitious climate scenario limiting the temperature rise to 2°C (2D scenario).

It then applied two mobility scenarios to each of these climate scenarios: the first, in connection with "Business As Usual" (BAU) mobility, corresponds to a continuous increase in the vehicle ownership rate and a greater reliance on cars. The second is a sustainable mobility scenario, which favors the use of public and non-motorized transport and an integrated approach to land-use and urban transport planning and investment.

Paris Agreement: towards widespread electrification of the vehicle fleet

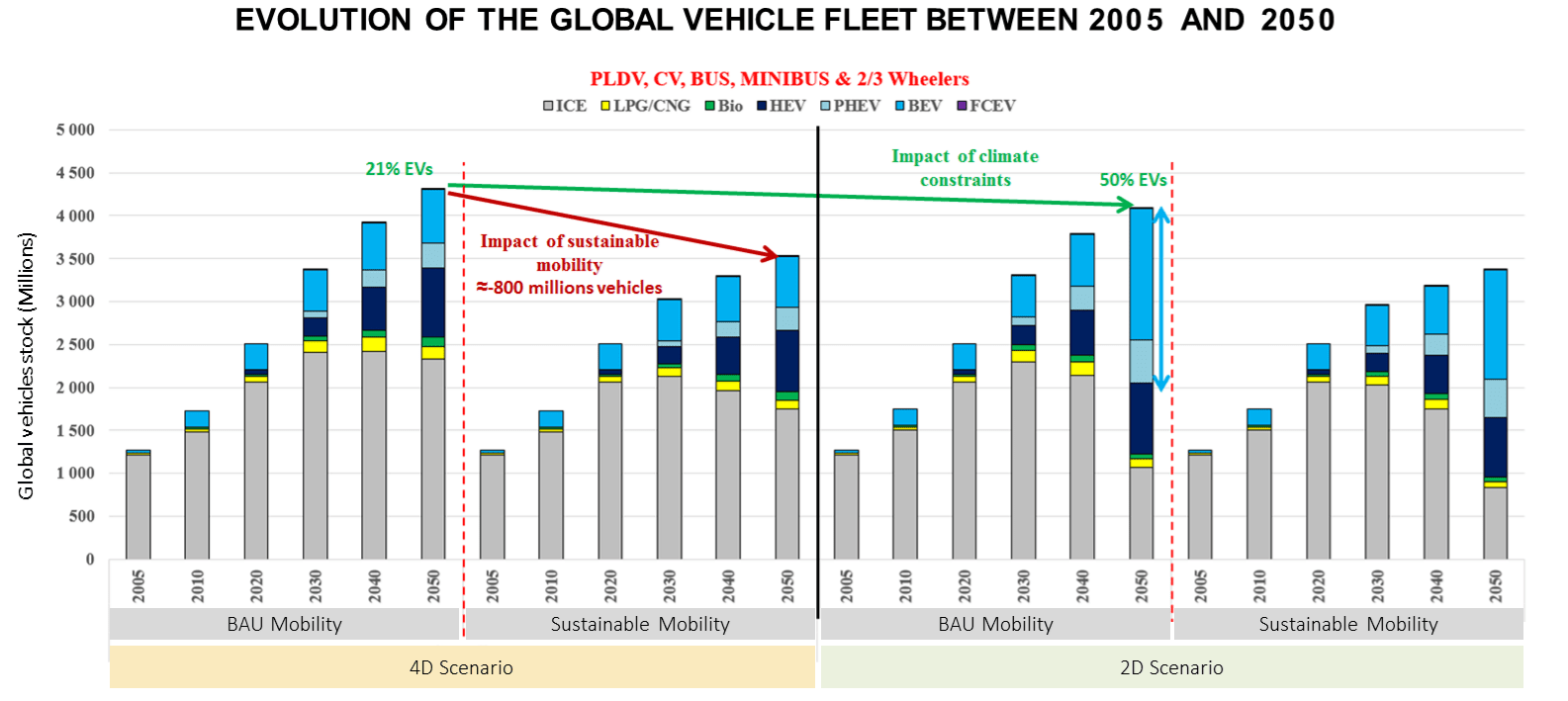

Using the TIAM-IFPEN model (Hache et al., 2019), the team assessed the evolution of the global vehicle fleet up to 2050. In the case of climate targets in line with the goals of the Paris Climate Agreement and with BAU mobility, it anticipates widespread electrification of the vehicle fleet (50% of EVs).

In the other combinations of scenarios, the internal combustion vehicle remains dominant. Projections show that the implementation of a sustainable mobility policy would make it possible to reduce the global fleet: in scenario 4D for example, there would be 800 million fewer vehicles (graph 3).

Graph 3

Source: IFPEN

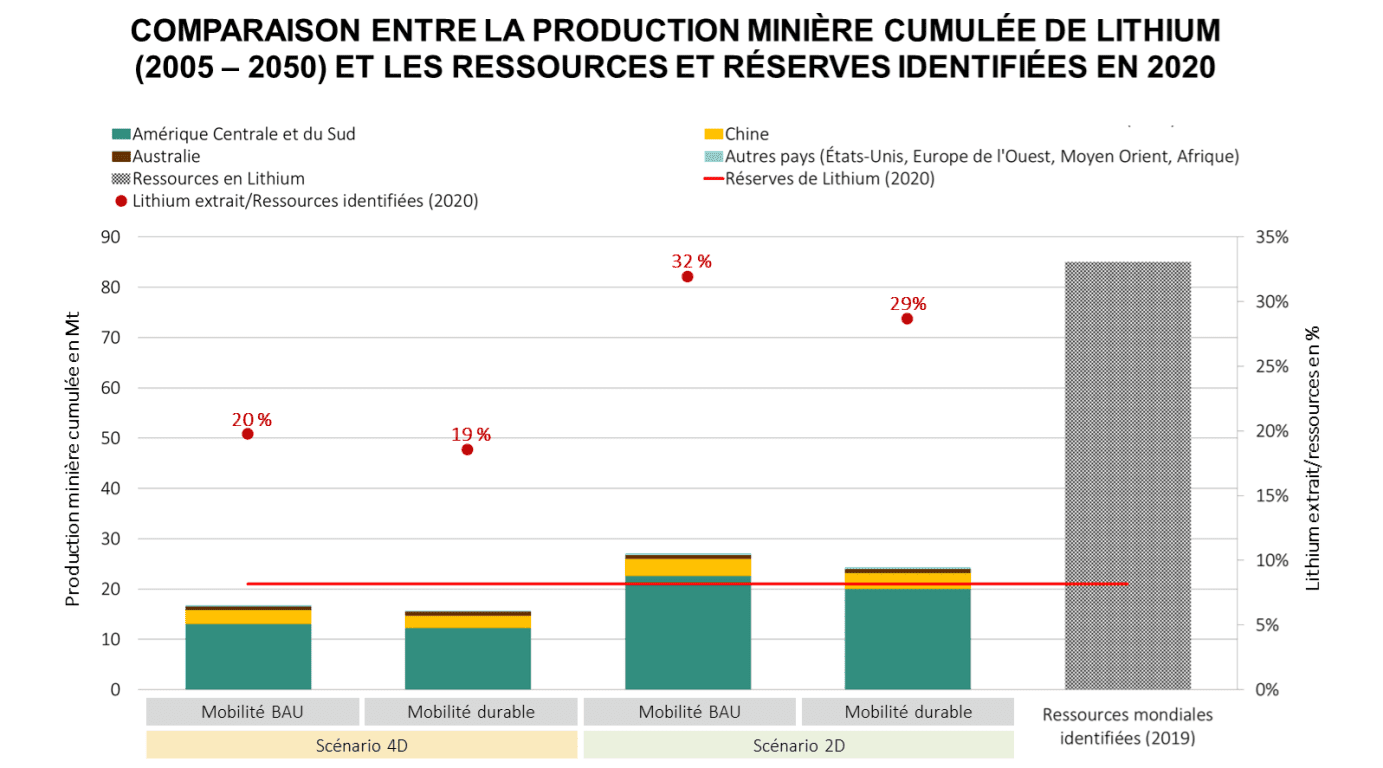

Limited geological criticality despite the increase in demand

Reflecting the development of the world EV fleet and thus the demand for lithium, lithium mine production appears to be higher under ambitious climate scenarios (Graph 4). In a 4D scenario, cumulative mine production between 2005 and 2050 is estimated at 15.7 Mt for the sustainable mobility scenario and 16.8 Mt for BAU mobility, while in a 2°C scenario these same demands reach respectively 24,3 Mt and 27.1 Mt, i.e. a multiplication by about 1.5 of the required lithium quantities!

Did you know?

What is the difference between primary and secondary production?

Primary production: production from resources contained in the subsoil.

Secondary production: production from recycled end-of-life products and waste recovery.

Source: Minéral Info

Despite the significance of these figures, only the 2D scenarios show cumulative lithium mine production above the current reserve level (21 Mt in 2020). Another indicator of criticality, the ratio of cumulative primary production to resources, also shows no high level of pressure on resources. This ratio thus fluctuates between 19% and 20% in a 4D scenario, while it is between 29% and 32% in a 2D scenario.

Source: IFPEN

The results therefore tend to indicate that there is no significant geological risk in the lithium market. As with the reserves, the resources are significant and are likely to be technologically accessible by 2050, at least in part.

What risks can be expected for lithium?

Lithium, a market with little flexibility

The rapidly increasing demand for lithium will require the development of new mines in the coming years. However, it can take up to ten years to bring a deposit into production. Moreover, part of the current production is not very flexible in the short term: while mines operating from spodumene (Australia) can adapt their production fairly quickly, the mining of Andean salt flats involves an evaporation process that can take up to 18 months. Finally, junior or mid-sized companies are struggling to find the necessary financing to develop these capital-intensive projects, a problem accentuated by the low transparency of the lithium market (Lefebvre and Tavignot, 2020).

A metal produced at the expense of environmental considerations

The lithium industry generates environmental impacts, the intensity of which depends on the mode of extraction. These impacts mainly concern (Early, 2020):

- CO2 emissions: 15 tons of CO2 are needed on average to produce one ton of lithium in the case of hard rock mining and 5 tons for the mining of underground reservoirs.

- Water use: 469 m3 of water is required to produce one ton of lithium. In Chile, indigenous communities and environmental groups are increasingly opposed to lithium mining activities in the Atacama Salt Flat because of the pressure it exerts on fresh water resources (Sherwood, 2019).

- Land use: Lithium production through the mining of underground reservoirs monopolizes 3,124 m2 of land per ton produced. Huge evaporation basins thus disfigure entire landscapes in the Andean salt flats.

The environmental impacts related to lithium extractions and the growing media pressure around the carbon footprint of ecological transition technologies have generated a strong interest in green lithium, i.e. lithium from geothermal waters. For the same volume of lithium extracted, this method would thus make it possible to consume 150 times less water and 3,000 times less land than the mining of underground reservoirs (Early, 2020). Geothermal lithium reserves have been located in the United States, but also in Europe (Germany, France, United Kingdom).

The idea of a lithium that is "made in Europe" is also particularly appealing to the European Union, whose industrial ambition is to reduce its dependence on China, and Asia in general, in the battery segment for electrified vehicles. This ambition has led to the launch in 2017 of the European Alliance for Batteries, a project supported by the European Commission and bringing together more than 500 public and private players in the sector.

A Chinese hold on the market?

China has only 7% of lithium reserves but has a much higher level of control over the value chain. China's apparent weakness in the mining sector should be qualified: 17% of extractions come from Chinese soil in 2020, but Beijing actually has more control over mining thanks to Ganfeng and Tianqi hold shares in numerous mining projects and competing companies around the world (Lefebvre and Tavignot, 2020).

Furthermore, Australia also sends 80% of its mining production to China for processing, refining and consumption. Chile does carry out some processing, but leaves the refining to Japan, South Korea and China. In this way, Beijing would control between 50% and 89% of the world's refined lithium production (LaRocca, 2020).

China has finally moved down the value chain by investing in energy storage technologies. By 2018, it accounted for 61% of global lithium-ion battery production capacity (Desjardins, 2018). The results of the model also confirm that the ambitions of the Made In China 2025 plan in the field of electrified vehicles (Hache, 2019) should maintain China's position as the world's leading consumer of lithium by 2050.

This strong reliance of the global market on Chinese processing and refining activities, coupled with a growing Chinese interest in lithium, may call into question the security of future supply.

Lithium triangle: national strategies with uncertain consequences

The lithium triangle contains 58% of global resources, 53% of global reserves and 29% of global ore production (USGS, 2021) and, according to the IFPEN team's findings, the region is expected to become the world's leading lithium exporter by 2050 with 90% of global supply (Graph 4). The position of individual countries in the region in international trade is also closely linked to their national policies.

In Argentina, for example, the favorable climate for foreign investment has enabled exploration projects and the development of new mining sites to take off. Chile, on the other hand, undermined by internal opposition and, hampered by the opacity of its legal and regulatory framework, has not been able to maintain its position in global lithium production. Finally, Bolivia, despite the willingness of the government of Evo Morales to create a national lithium industry - a goal materialized by the creation of the national company Yacimientos de Litio Bolivianos (YLB) in 2017 - has still not entered the world market because of its lack of technological know-how in the field.

In short, the supply’s margin decreases because of the massive penetration of EVs worldwide (Scenarios 2D), but the results of the model do not indicate any real geological criticality for lithium. However, the long-term equilibrium dynamics of commodity markets teach us that the absence of geological criticality of resources does not exclude other risks (economic, industrial, geopolitical or environmental). In particular, the competition between actors appears quite relative on the lithium market, despite the entry of new companies. Thus, the small number of actors and their oligopolistic positioning question the economic criticality of the sector.

In addition, the economic, industrial and commercial policies of China and its companies, on the lithium sector but also on the battery market, remains a key element for understanding the lithium market in the future.

1 Electric vehicles(EVs) include Plug-in Hybrid Electric Vehicle (PHEVs), Battery Electric Vehicles (BEVs) and Fuel Cell Electric Vehicles (FCEVs)

Points to remember

Lithium is increasingly being used in lithium-ion batteries for electronic devices or electrified vehicles, but reserves and resources are expected to be sufficient to meet needs until 2050.

Thus, the risks to lithium are not so much geological as they are:

- geostrategic: Reserves and production are increasingly concentrated geographically, with the Lithium Triangle concentrating 58% of resources and 53% of reserves, and Australia and Latin America 80% of mining extraction;

- economic:

*Prices are not transparent, which impacts the production and development of mining projects.

*5 global players control the majority of mining production and have a strong influence on the value chain, with China in particular exerting a strong influence on processing and refining activities;

- environmental: lithium production is especially CO2-intensive and water-consuming. In addition, the exploitation of underground reservoirs monopolizes the land and evaporation basins disfigure the landscapes in the Andean salt flats.

To find out more :

Metals in the energy transition

Find all the points on this video:

>> BIBLIOGRAPHY

Scientific contacts : Emmanuel Hache, Charlène Barnet, Gondia Seck

To quote from this article: Hache, Emmanuel ; Barnet, Charlène ; Seck, Gondia-Sokhna «Lithium in the energy transition: more than a resource issue?», Metals in the energy transition, n° 4, IFPEN, February 2021.

You may also be interested in

Aluminium in the energy transition: what lies ahead for this indispensable metal of the modern world?

Nickel in the energy transition: why is it called the devil’s metal?

Rare earths in the energy transition: what threats are there for the “vitamins of modern society”?

Copper in the energy transition: an essential, structural and geopolitical metal!

Cobalt in the energy transition: a closer look at supply risks